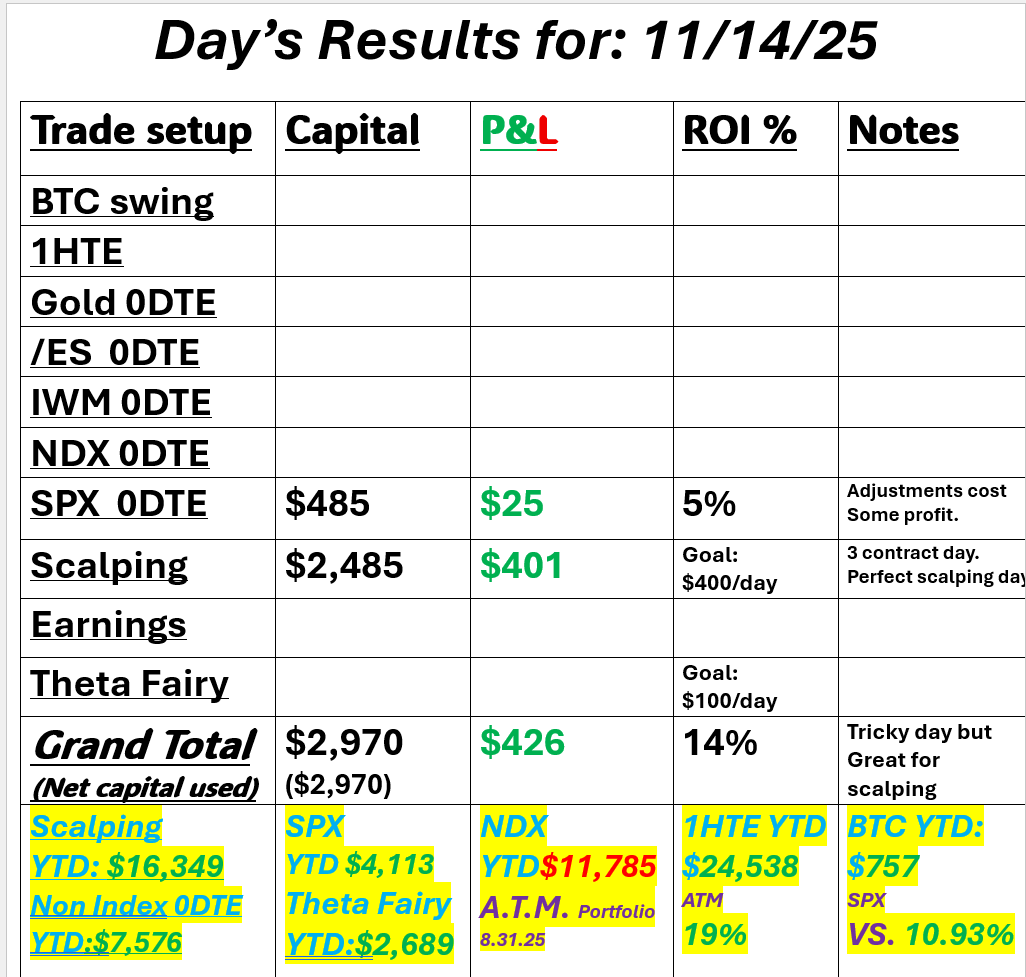

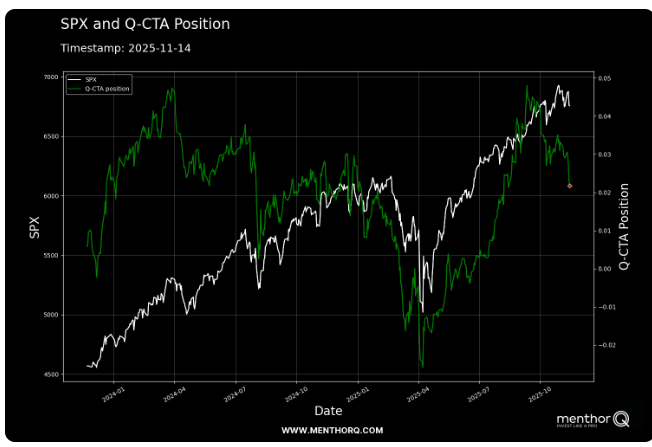

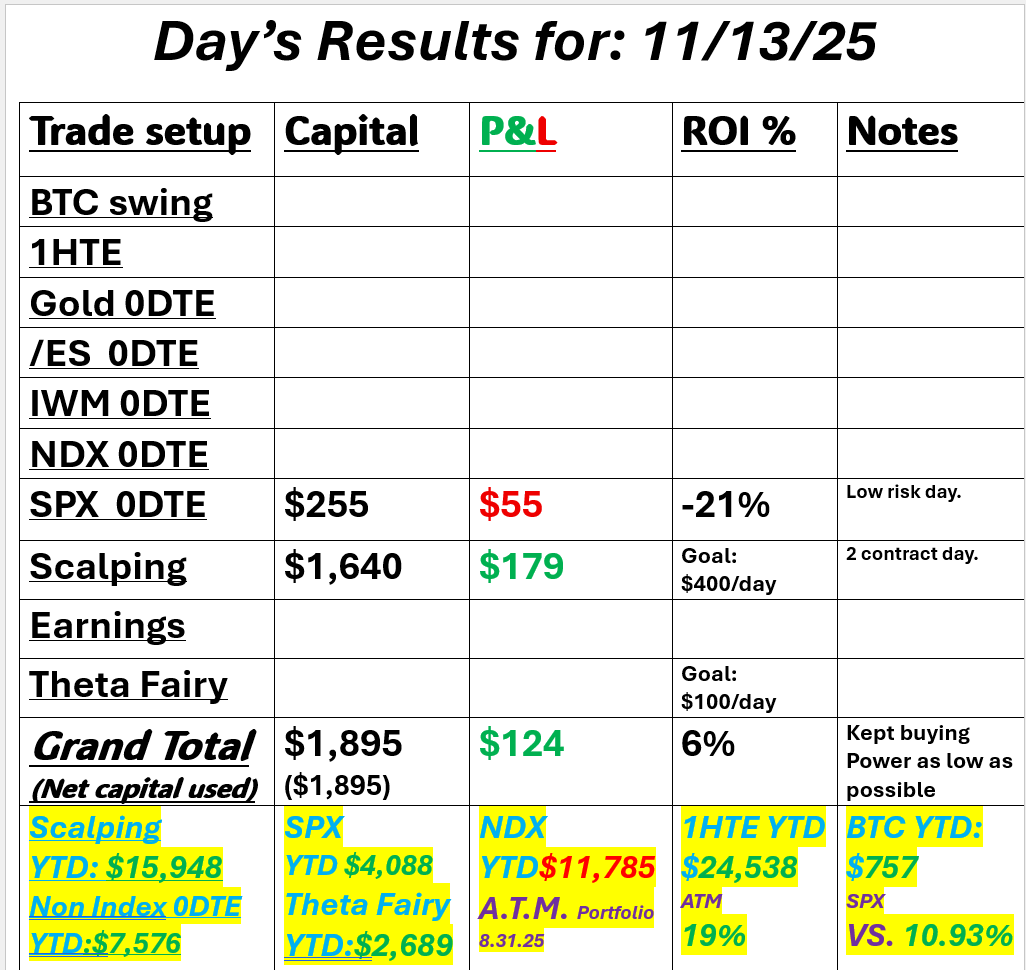

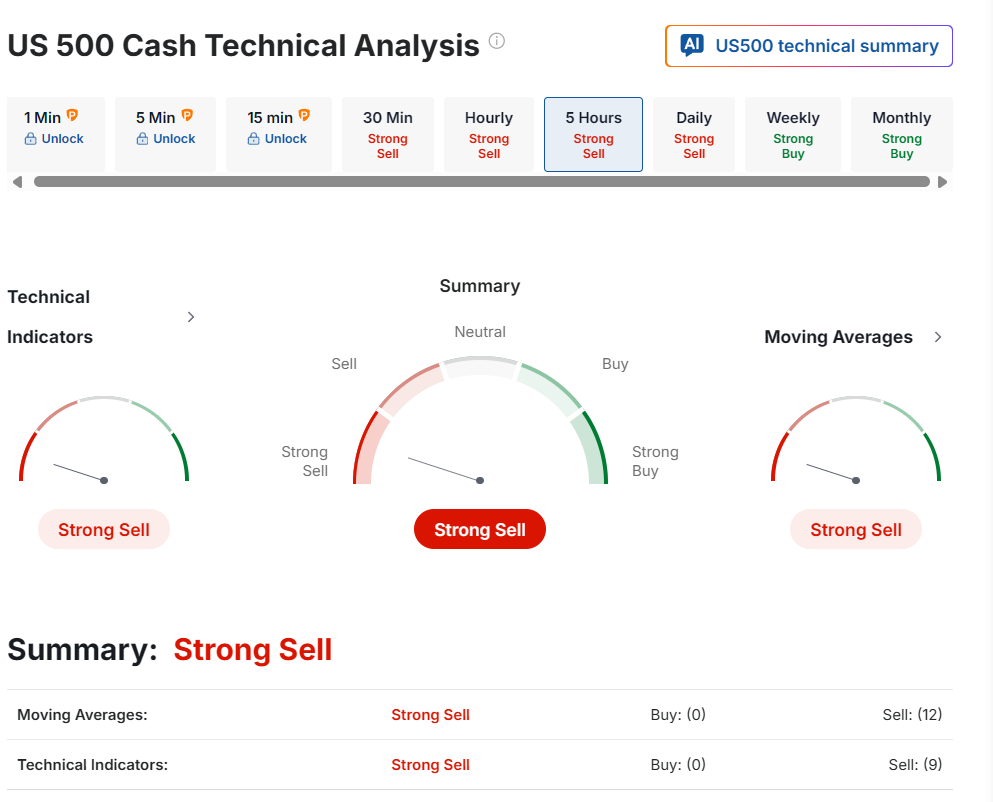

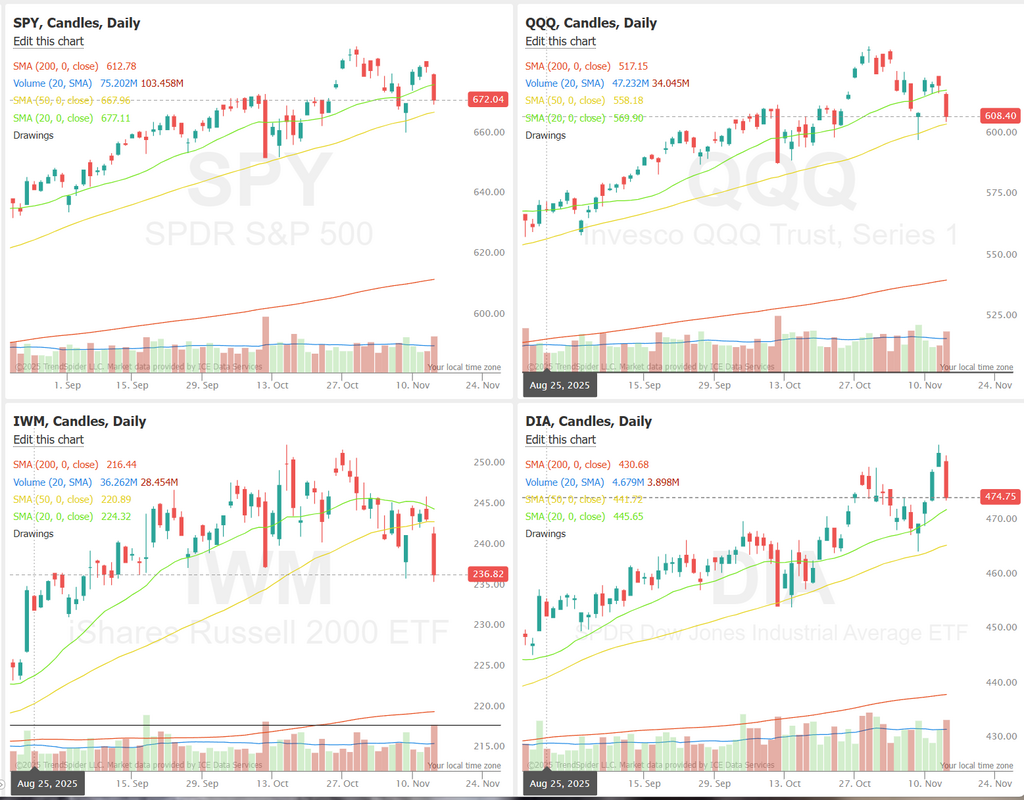

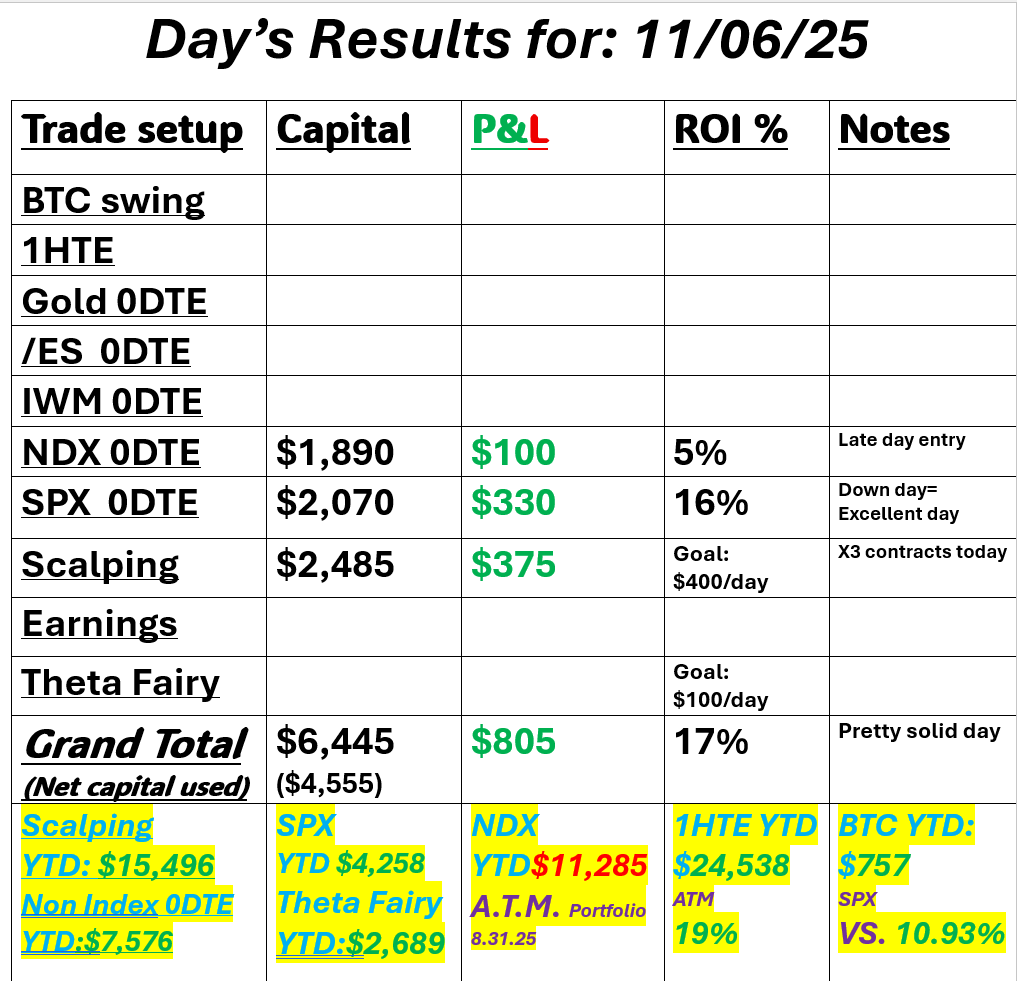

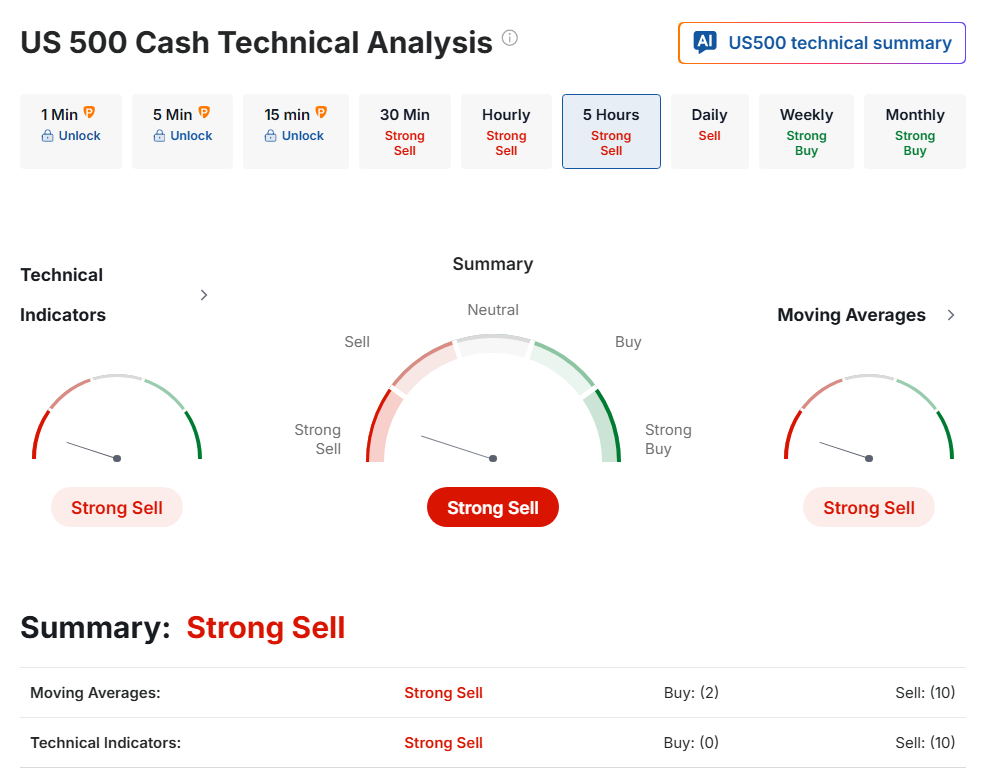

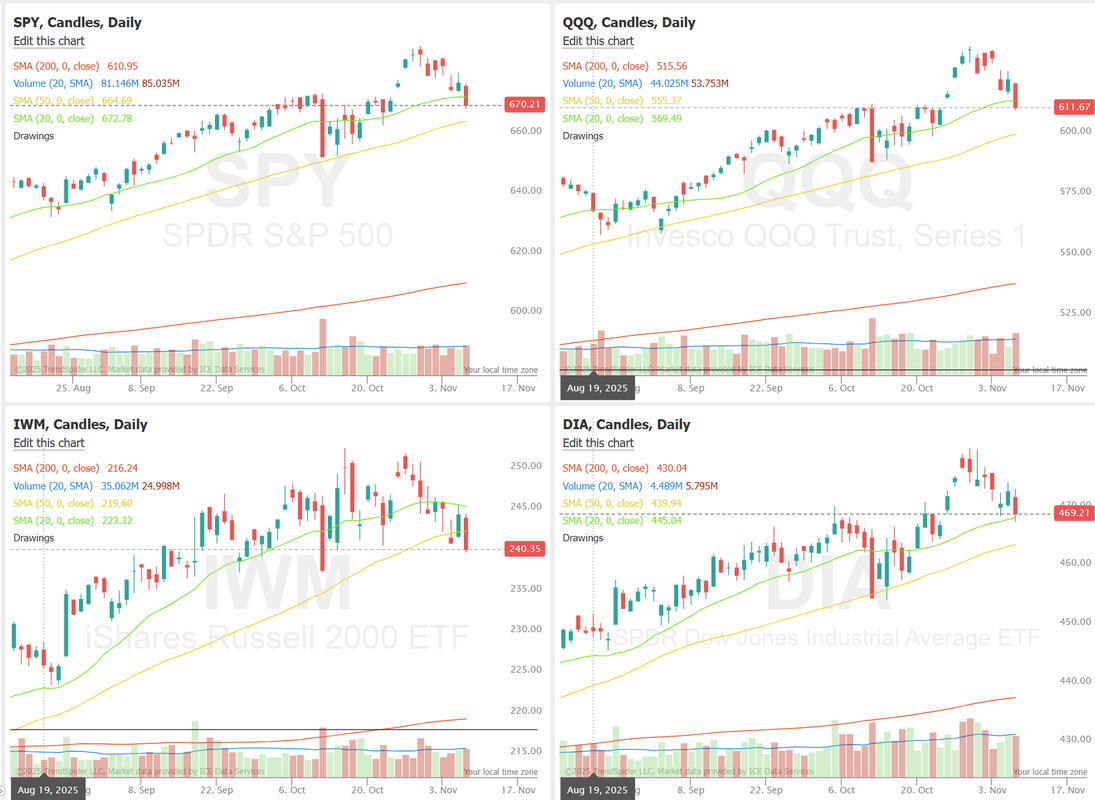

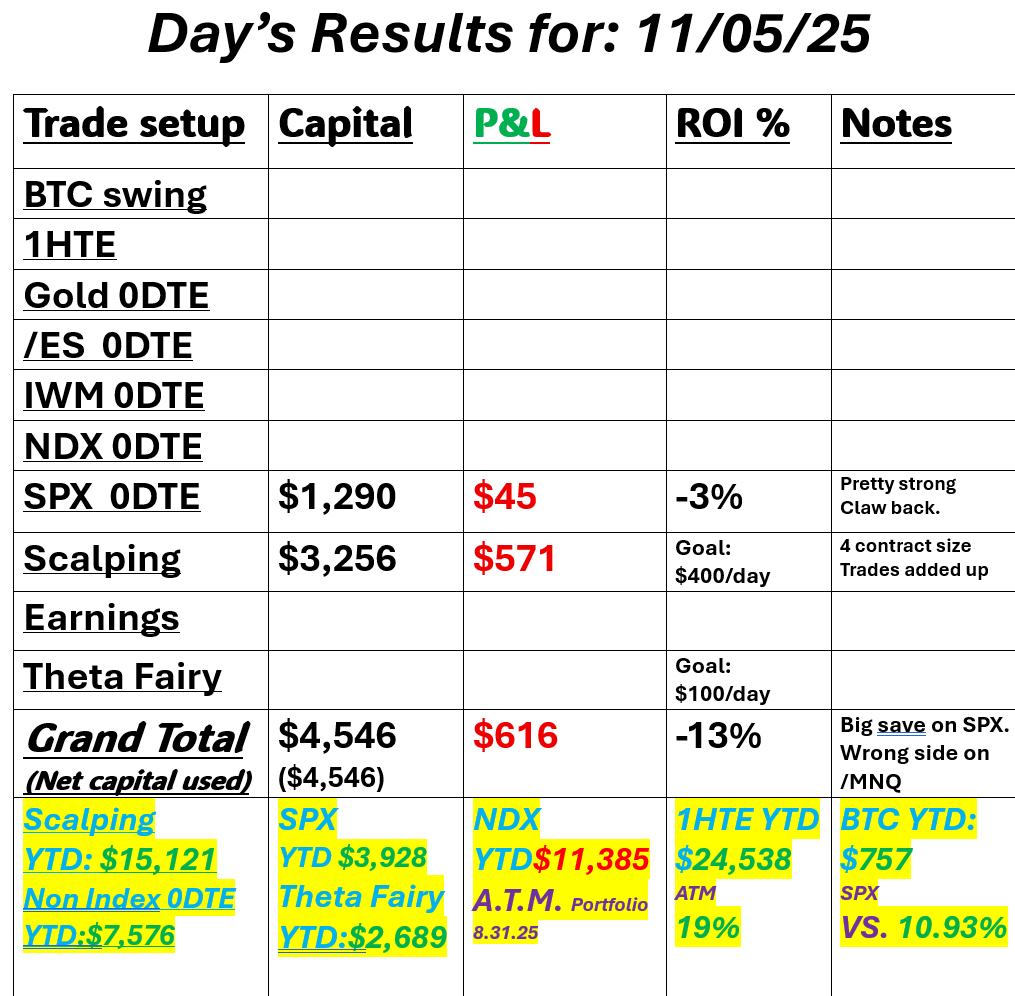

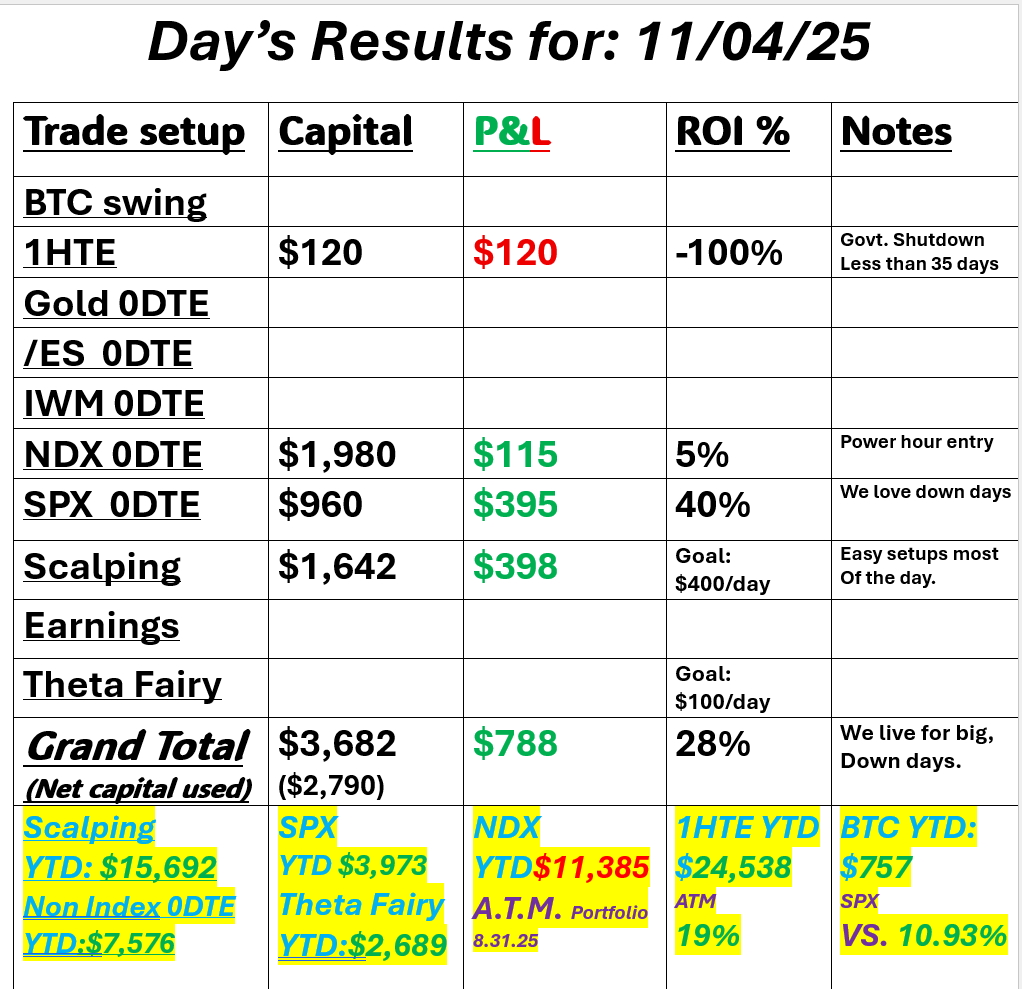

Nivida earnings incomingNVDA earnings are coming in after the close today. The numbers should be awesome. It's not like AI chip and GPU demand has waned. The real question is, how will the market react? Chances are high we get a selloff. Regardless, it will be a driver for futures after hours and likely into tomorrow morning. We'll be looking to add another Theta fairy tonight once we see the reaction. Yesterday was a loss for me but I'd still take the same approach. All our day trades worked out well, even though the SPX needed an adjustment to work. I went bigger than normal on scalping because the movement (or so I thought) was going to be great. It ended up chopping me up most of the day and the internet outage in the early hours hurt. Trading without our tick strike audible order flow was tough and put me in a hole right out of the gate. Here's a look at my day.  Let's take a look at the markets: Sell mode is still in place technically.  We are now FIRMLY below the 50DMA on all our indices  Theta fairy's seem to be back! Premium is rich now. They still need to be modified as a pure strangle is still too low of premium but they seem to be working. We've got another one on this morning that is already above our normal take profit level. We'll look to add another one this late afternoon after we see what NVDA earnings do to the futures.  Today is part II of our training on the next four books in our master list. Join in on our live zoom feed.  December Nasdaq 100 E-Mini futures (NQZ25) are trending up +0.44% this morning, signaling a modest rebound from a bruising stretch of losses, while investors look ahead to an earnings report from AI darling Nvidia. In yesterday’s trading session, Wall Street’s major indexes ended in the red. Home Depot (HD) slid over -6% and was the top percentage loser on the S&P 500 and Dow after the world’s largest home-improvement retailer reported weaker-than-expected Q3 comparable sales and cut its full-year earnings guidance. Also, chip stocks slumped, with Marvell Technology (MRVL) and Micron Technology (MU) falling more than -5%. In addition, Amazon.com (AMZN) sank more than -4% after Rothschild & Co. Redburn downgraded the stock to Neutral from Buy. On the bullish side, Medtronic Plc (MDT) climbed over +4% and was the top percentage gainer on the S&P 500 after the medical device maker posted upbeat FQ2 results and raised its full-year guidance. Economic data released on Tuesday showed that U.S. factory orders rose +1.4% m/m in August, in line with expectations. Also, data from ADP Research showed that U.S. companies shed an average of 2,500 jobs per week in the four weeks ending November 1st. Richmond Fed President Tom Barkin on Tuesday offered an upbeat outlook on inflation, while indicating the labor market may be softer than the available data suggest. Still, he did not indicate whether he will back another rate cut next month. Meanwhile, U.S. rate futures have priced in a 53.4% chance of no rate change and a 46.6% chance of a 25 basis point rate cut at the December FOMC meeting. Investors are eagerly awaiting Nvidia’s third-quarter earnings report, scheduled for release after the market close. The chipmaker’s earnings reports have been market-moving since May 2023, when it delivered the revenue growth forecast that reverberated globally. Skepticism toward the AI trade is now at its highest level since before Nvidia’s 2023 forecast, putting pressure on the company to deliver with its report. “We expect Nvidia to exceed estimates and provide future earnings and revenue guidance that is higher than investors expect. It’s unlikely that Nvidia has seen any slowdown in demand for its products, even with increased competition, given how early we are in the AI cycle,” said James Demmert at Main Street Research. Retailers such as TJX Companies (TJX), Lowe’s (LOW), and Target (TGT), along with cybersecurity firm Palo Alto Networks (PANW), are also set to report their quarterly figures today. Market watchers will also pay close attention to the publication of the Fed’s minutes from the October 28-29 meeting. The FOMC lowered its benchmark rate last month for the second time this year, though Chair Jerome Powell cautioned that a December reduction is far from a “foregone conclusion.” Since then, a faction of Fed officials has intensified warnings that progress on inflation could slow or stall, casting doubt on the prospects for another rate cut next month and underscoring a widening divide within the central bank. “We expect the minutes to show a deeply divided Fed with concerns over weaker employment picture but sticky inflation,” according to Mohit Kumar, chief economist and strategist for Europe at Jefferies. In addition, market participants will be anticipating speeches from Fed Governor Stephen Miran, Richmond Fed President Tom Barkin, and New York Fed President John Williams. On the economic data front, investors will focus on the August Trade Balance data, set to be released in a couple of hours. The data was originally scheduled for release on October 7th, but was delayed due to the government shutdown. Economists anticipate that the trade deficit will narrow to -$61.3 billion from -$78.3 billion in July. The EIA’s weekly crude oil inventories report will be released today as well. Economists expect this figure to be -1.9 million barrels, compared to last week’s value of 6.4 million barrels. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.126%, up +0.10%. The SPX has been sliding in recent sessions, and the Volatility Risk Premium has jumped back into elevated territory, sitting near the upper end of its 3-month range. With IV marked as overvalued and VRP pushing above 5%, the options market is pricing in more short-term uncertainty than recent realized volatility supports. In the near term, this kind of setup often coincides with choppier price action as traders recalibrate to the richer volatility environment. The key focus now is whether VRP continues to rise—signal of persistent hedging demand, or quickly mean-reverts, which would hint that the recent volatility spike may be settling.  The QQQ 5-day Swing Model is entering a more tactical zone, with price pulling back toward the model’s risk trigger near 575.96, a level that has historically acted as a short-term pivot. The lower band remains well below current pricing, but the recent drop toward mid-range suggests momentum has cooled. With the swing model showing a high historical success rate and the upper band sitting far above at 616.66, the next few sessions may hinge on whether QQQ stabilizes above the risk trigger or continues sliding toward the lower band that has captured most successful rebounds. Short-term traders often watch these inflection zones closely, as moves into or away from risk triggers tend to shape near-term directional bias.  Wednesday

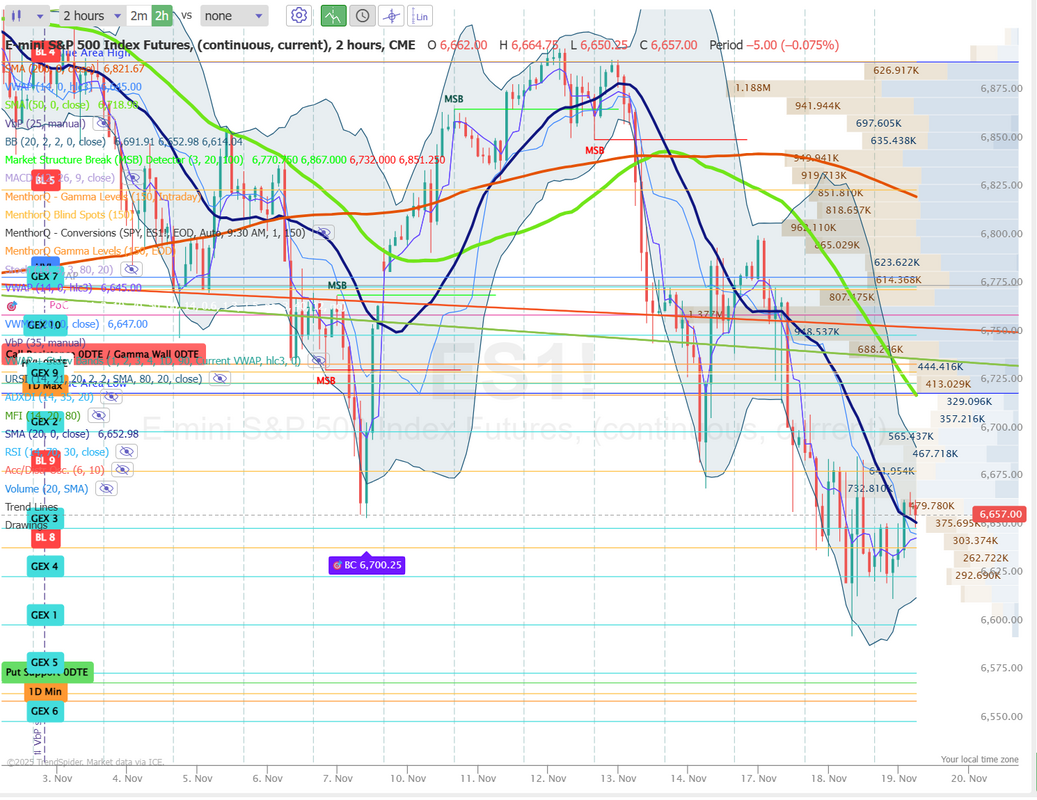

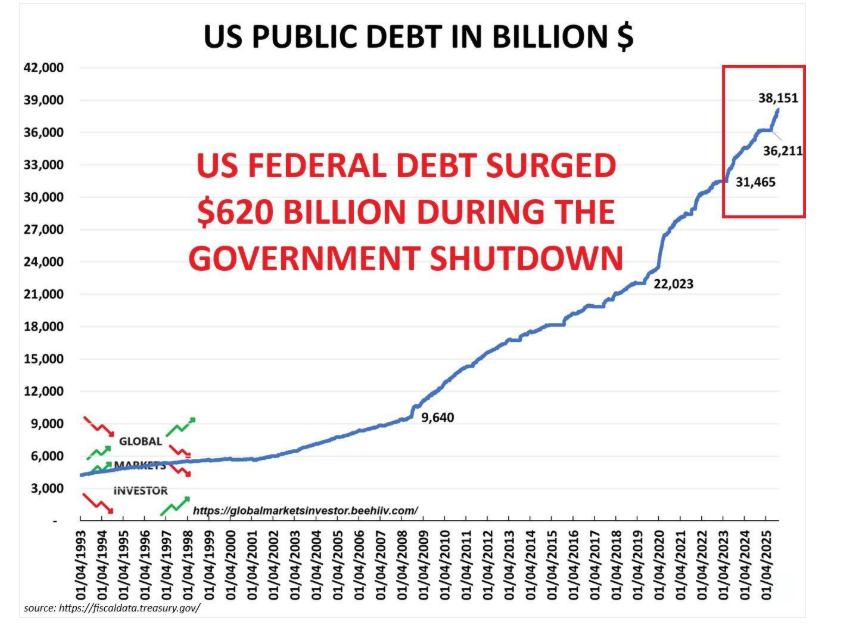

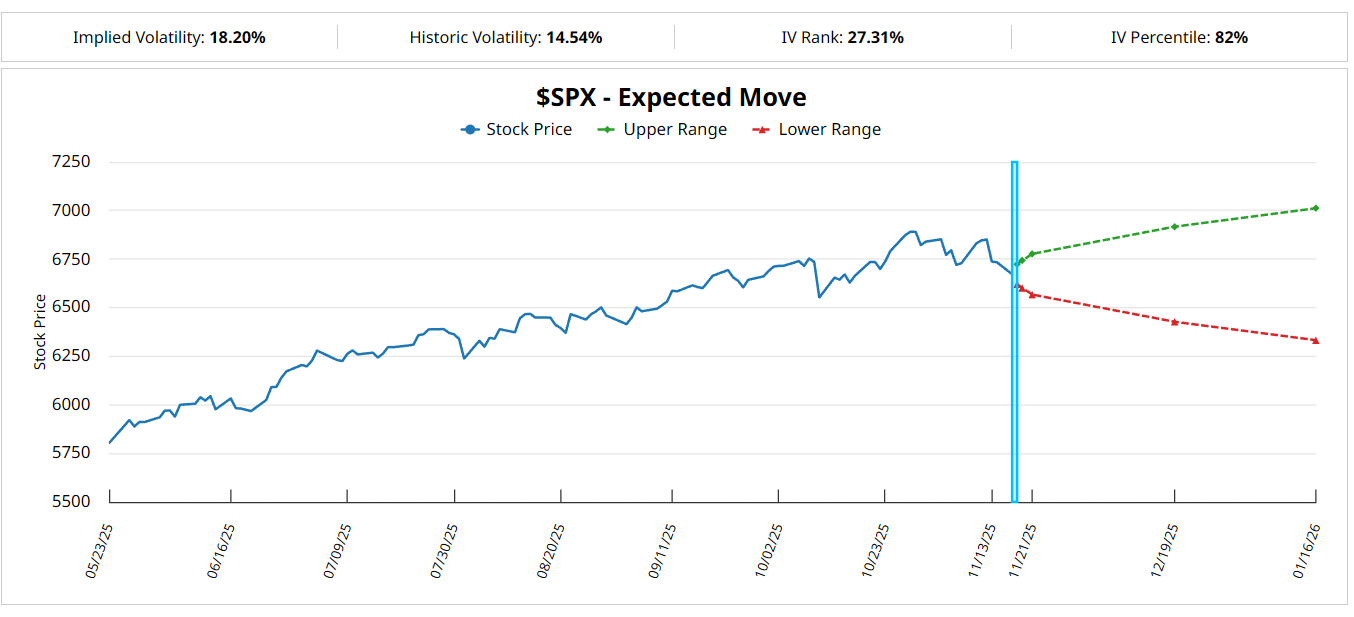

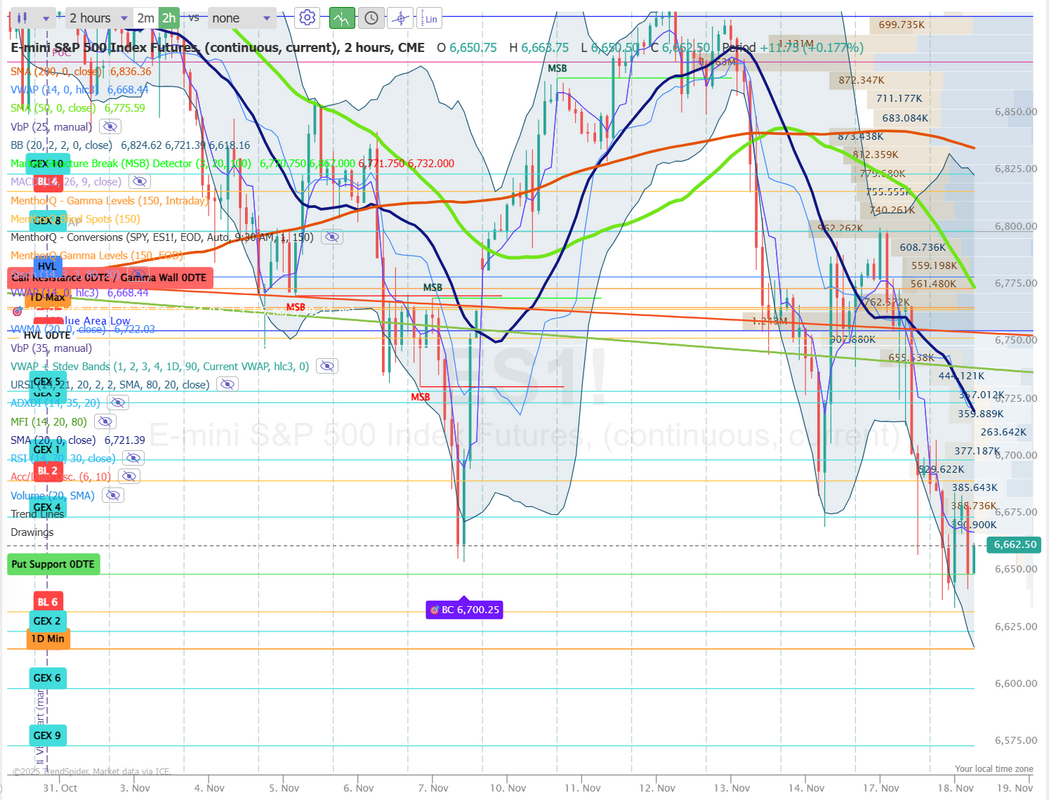

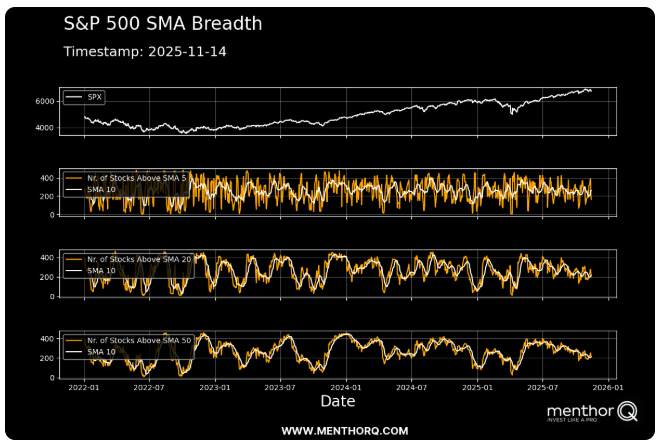

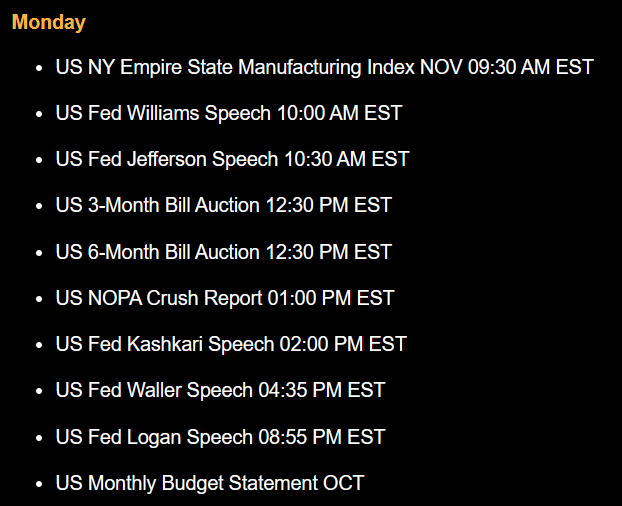

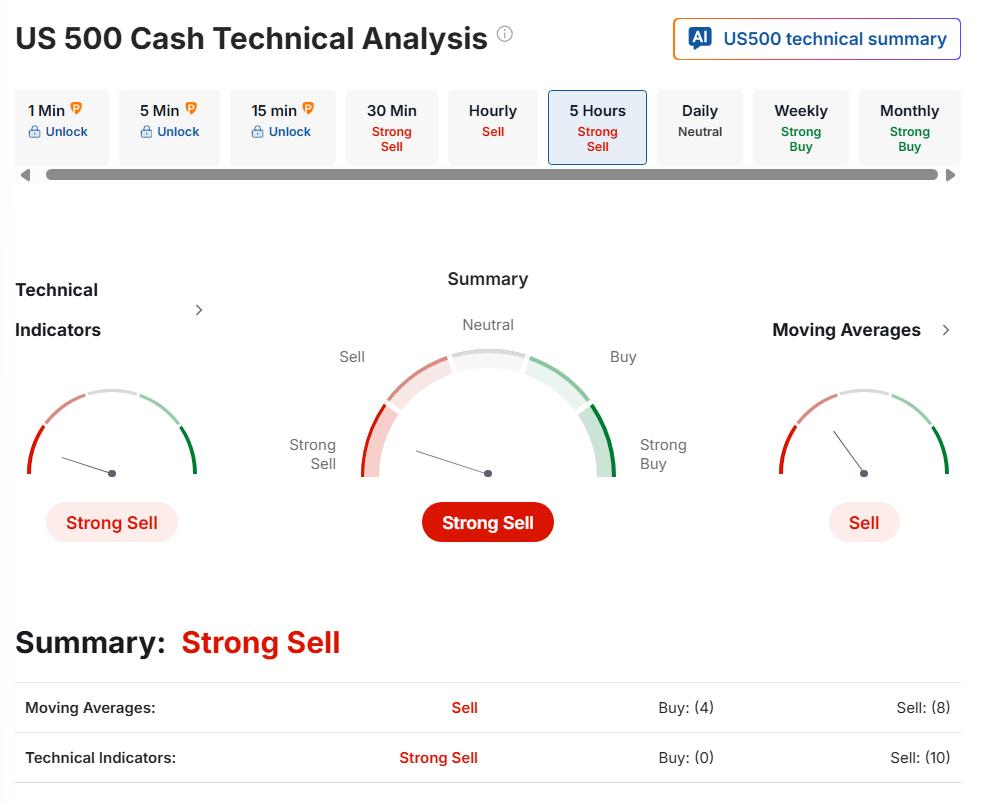

My lean or bias this morning is bearish once again. Much like yesterday, we may be a relief rally and futures are up as I type but technicals are bearish and being below the 50DMA you kind of have to go with the flow.  Let's take a look at the intraday /ES levels for 0DTE's today. 6679, 6700, 6719 6735* (big gamma wall) are all resistance levels. 6650, 6640* (key support level yesterday), 6625, 6599* (key buying level) are all support levels.  I look forward to seeing you all in the live trading room shortly. Our part II training should be another good one.

0 Comments

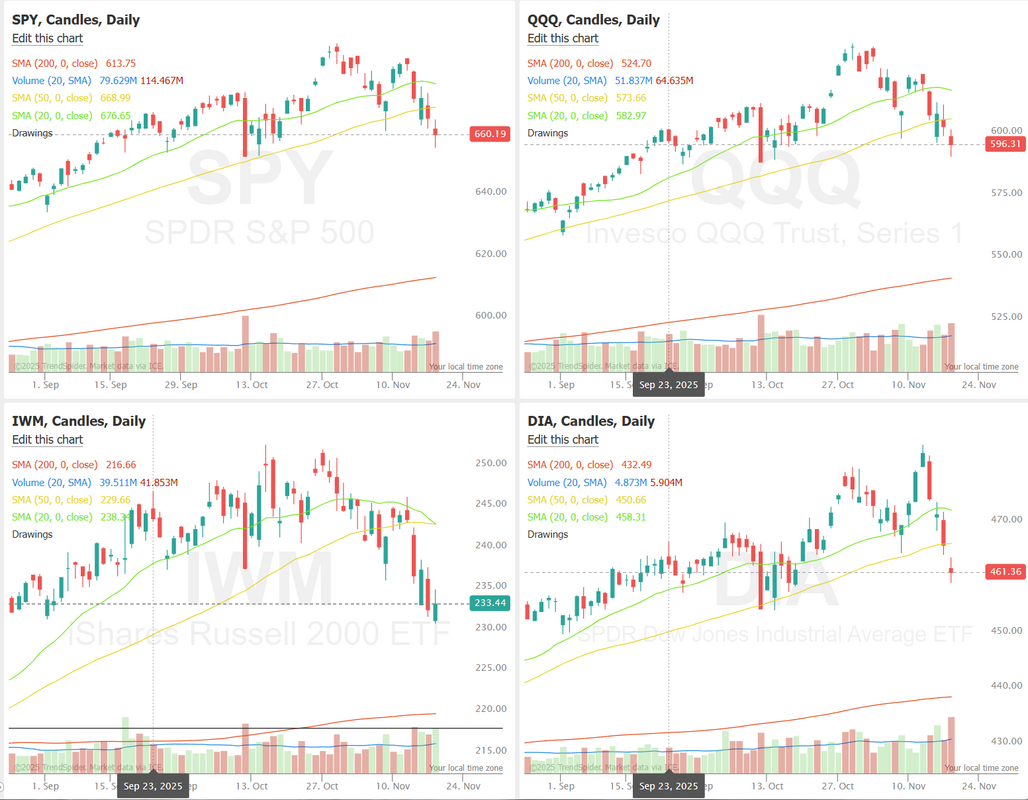

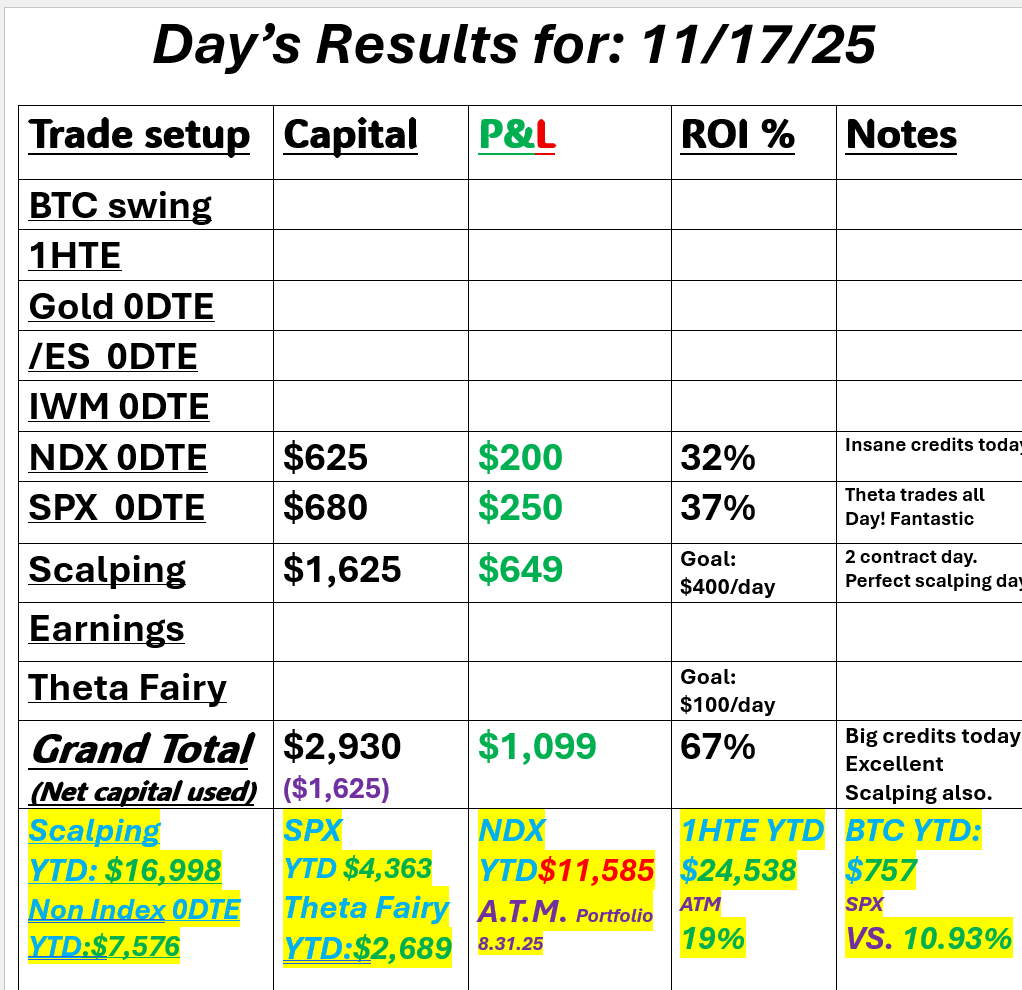

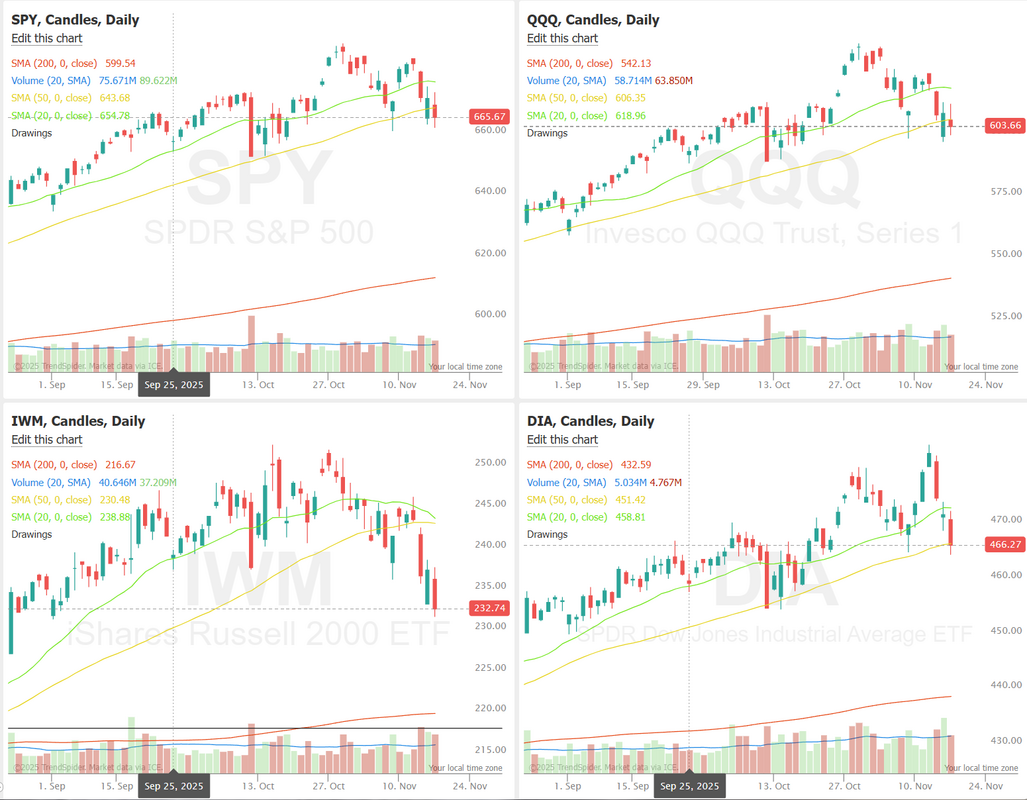

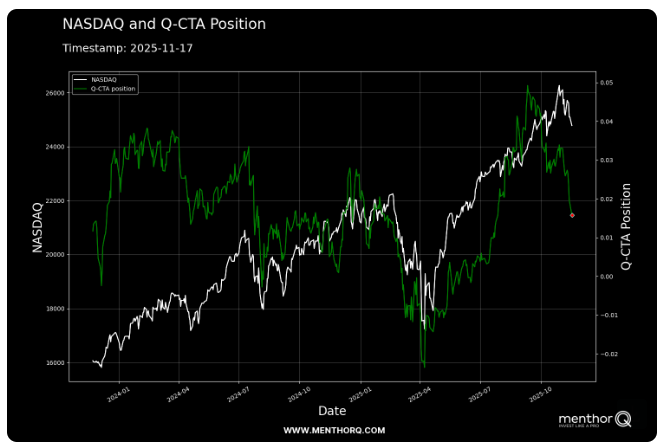

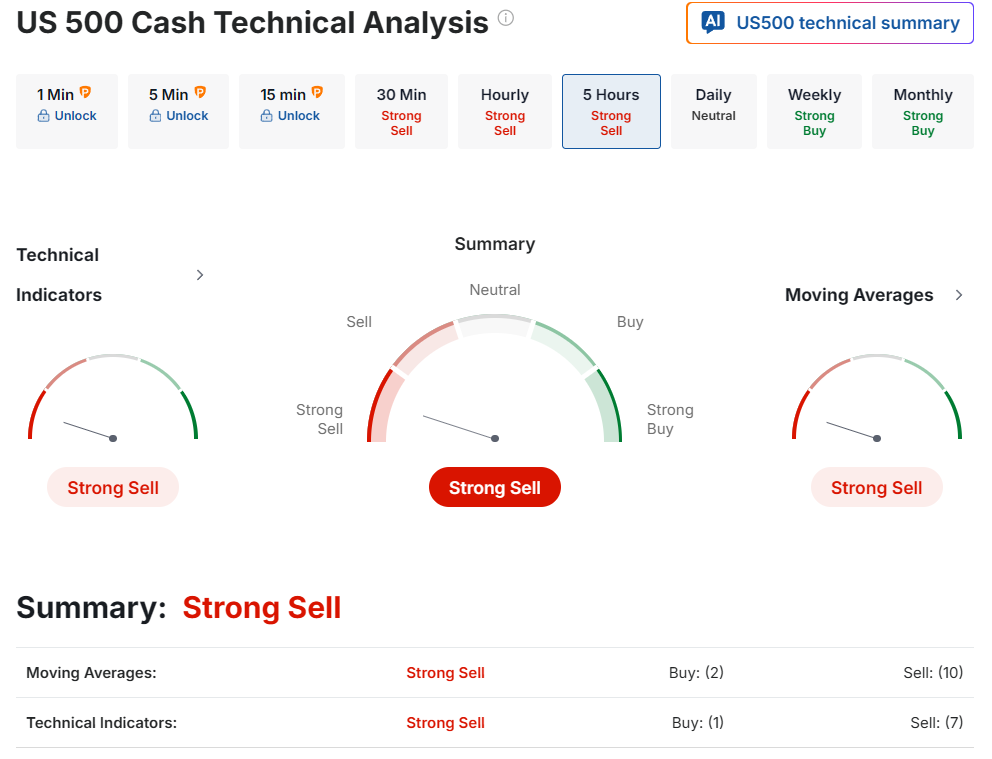

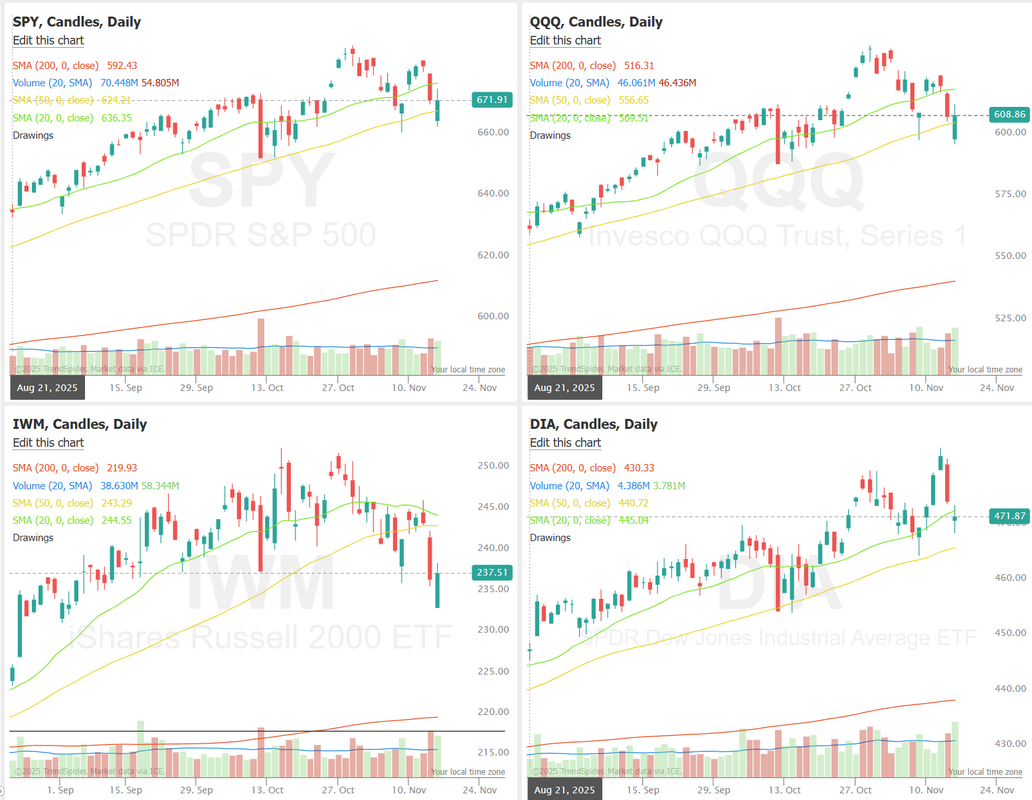

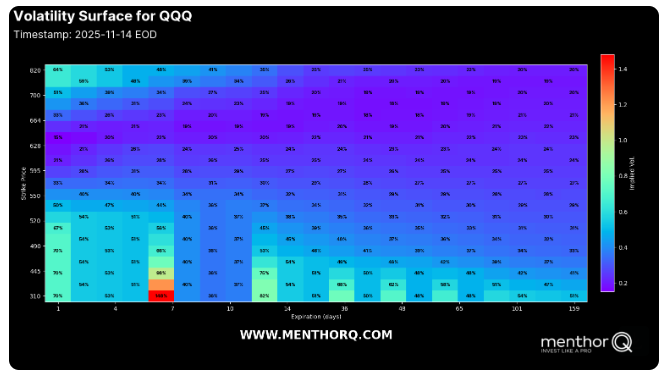

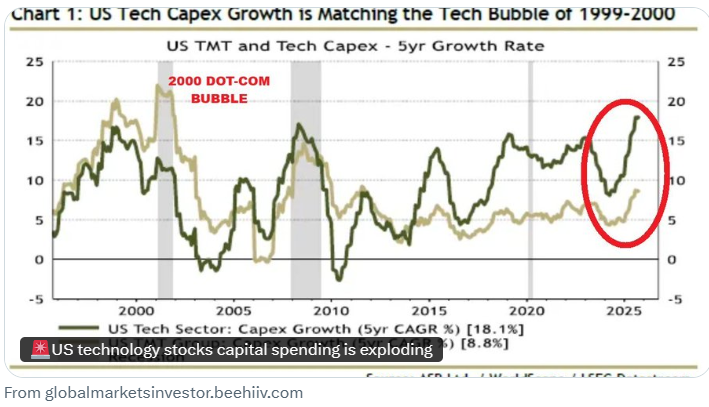

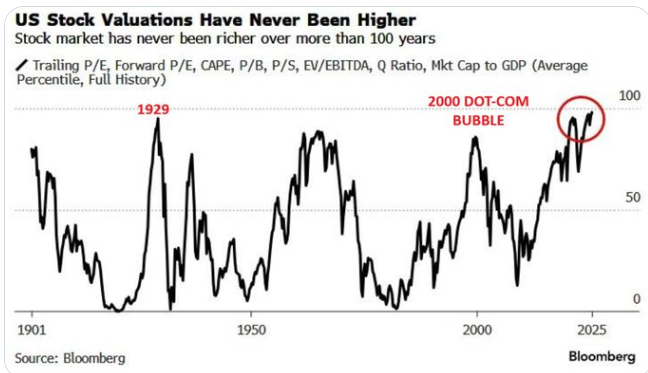

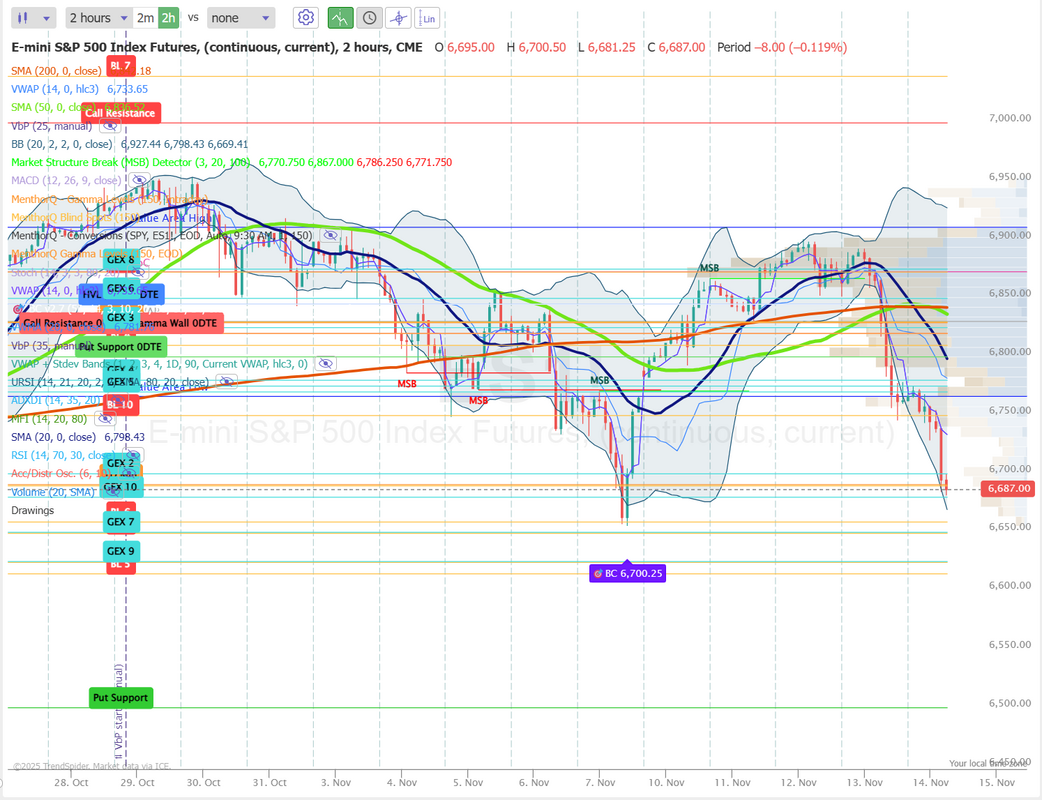

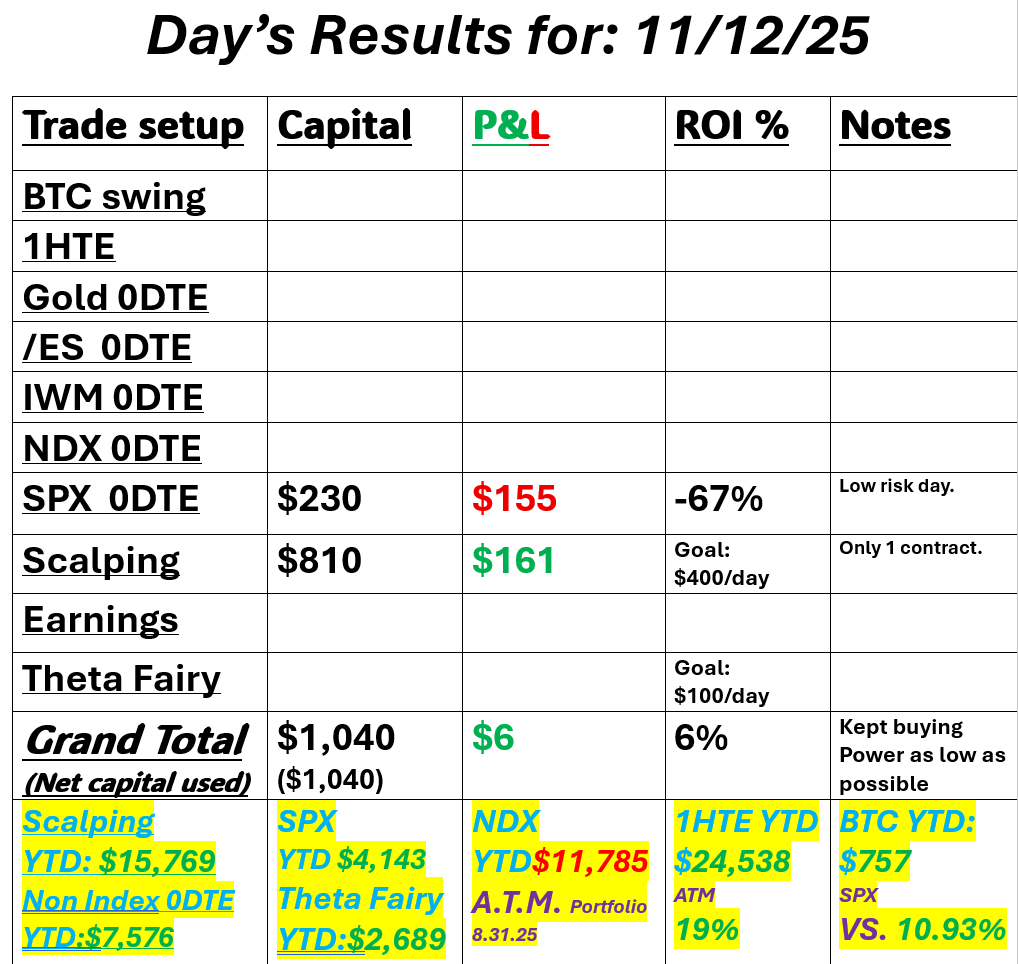

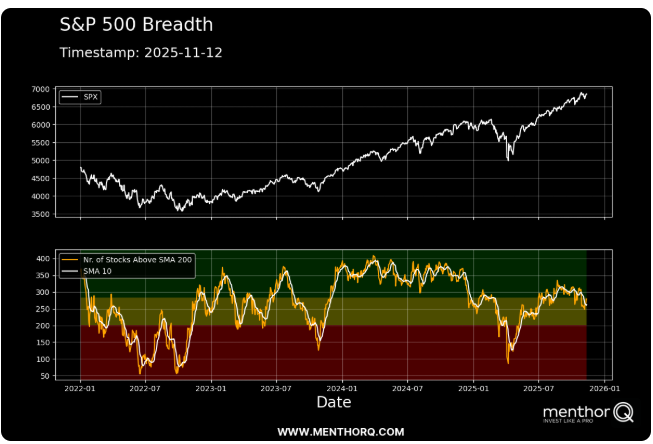

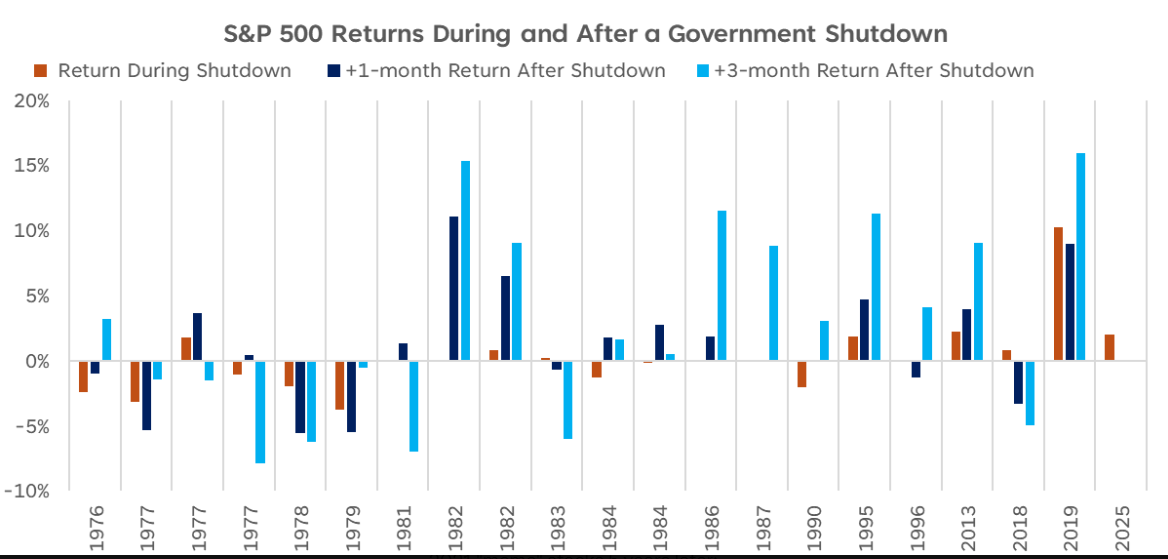

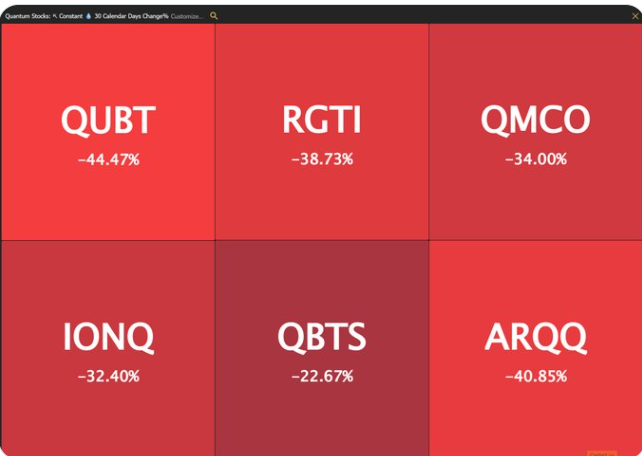

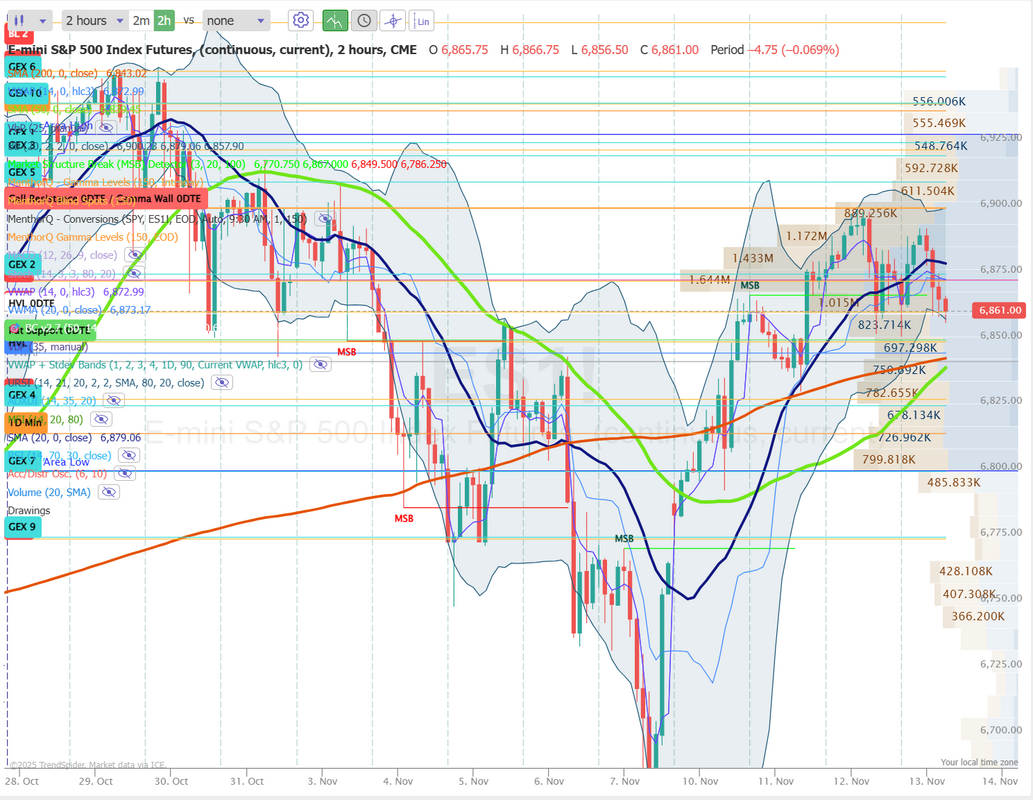

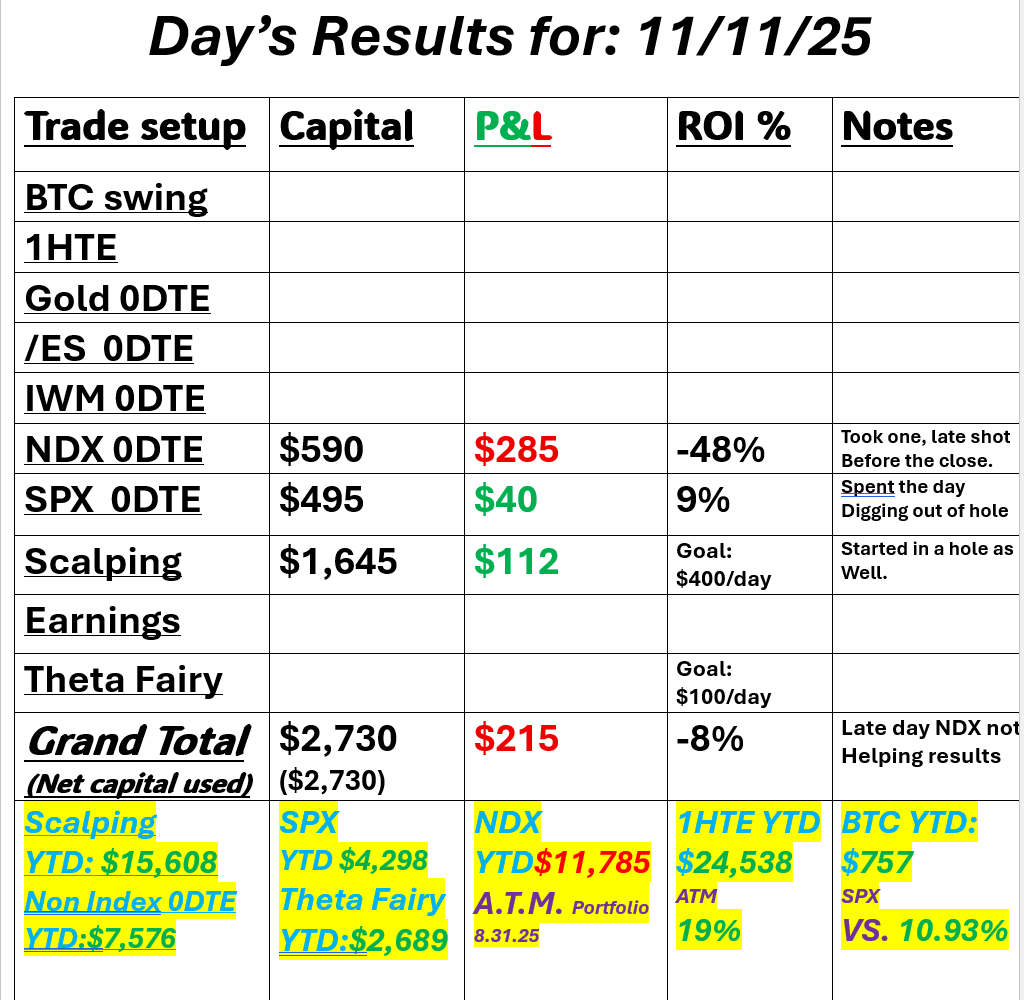

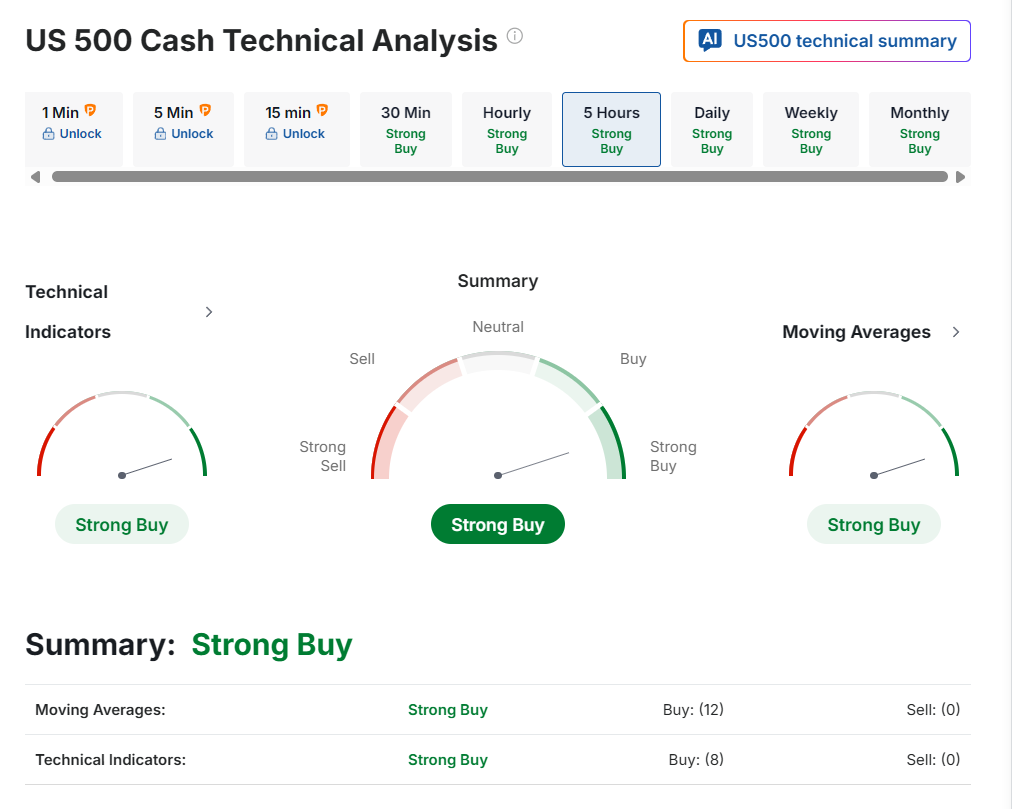

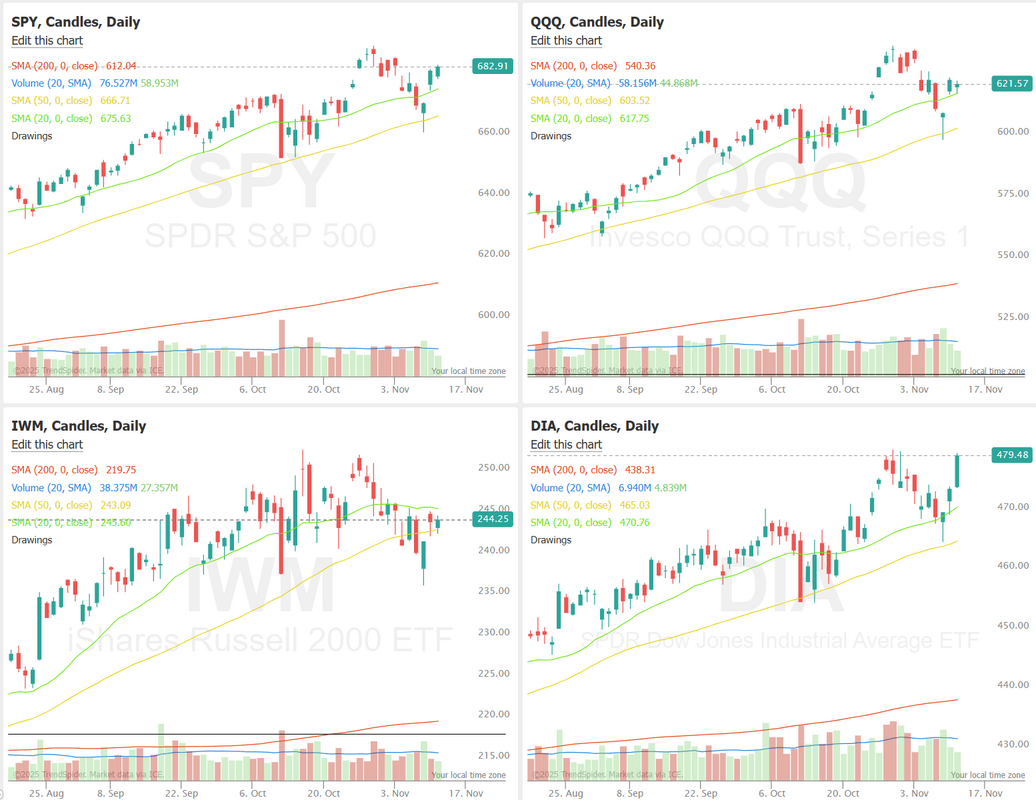

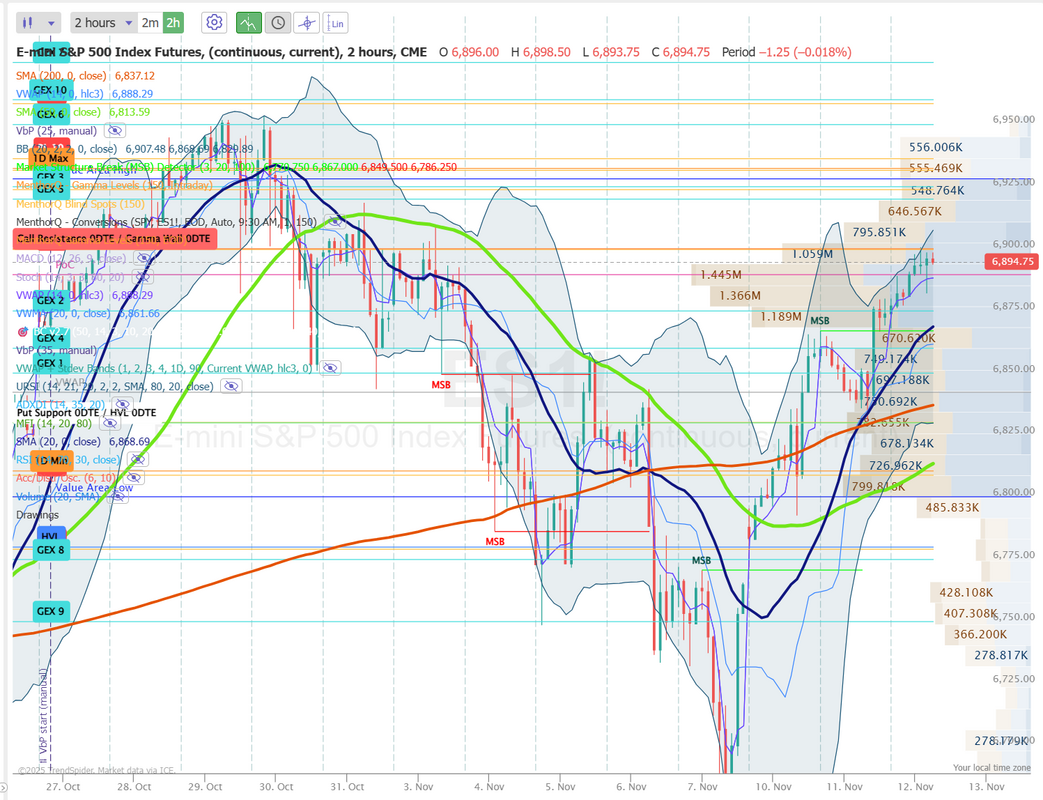

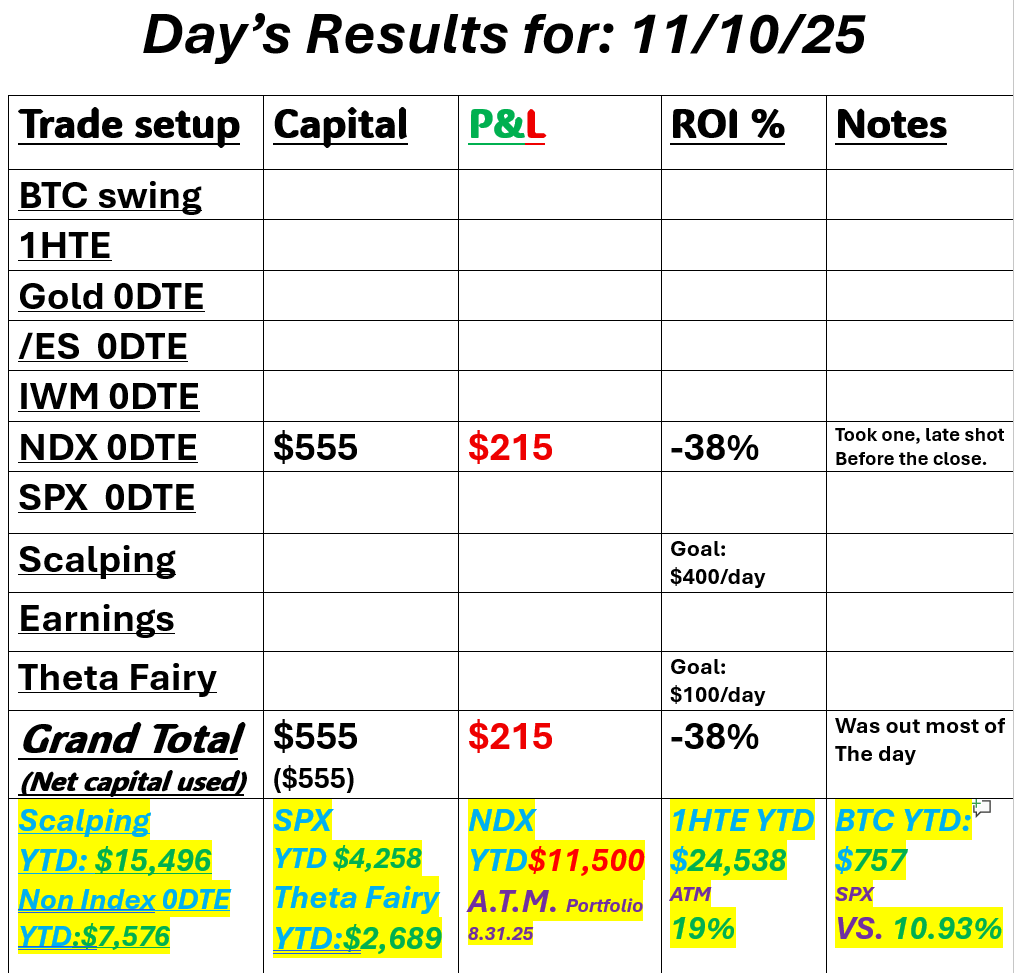

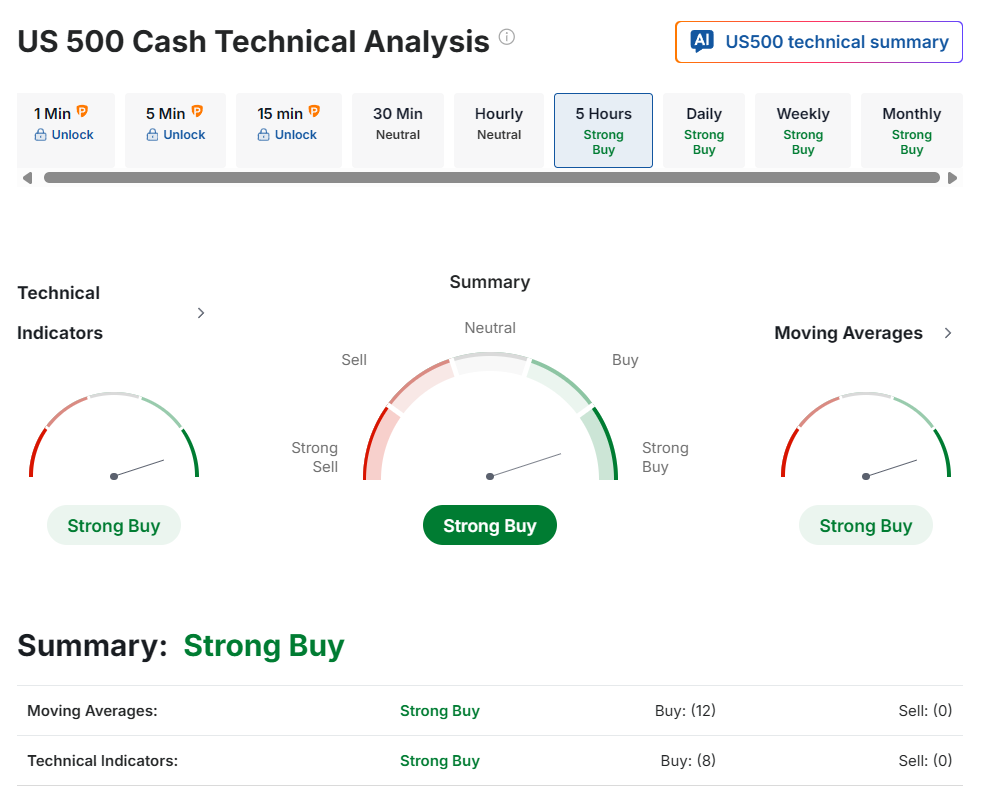

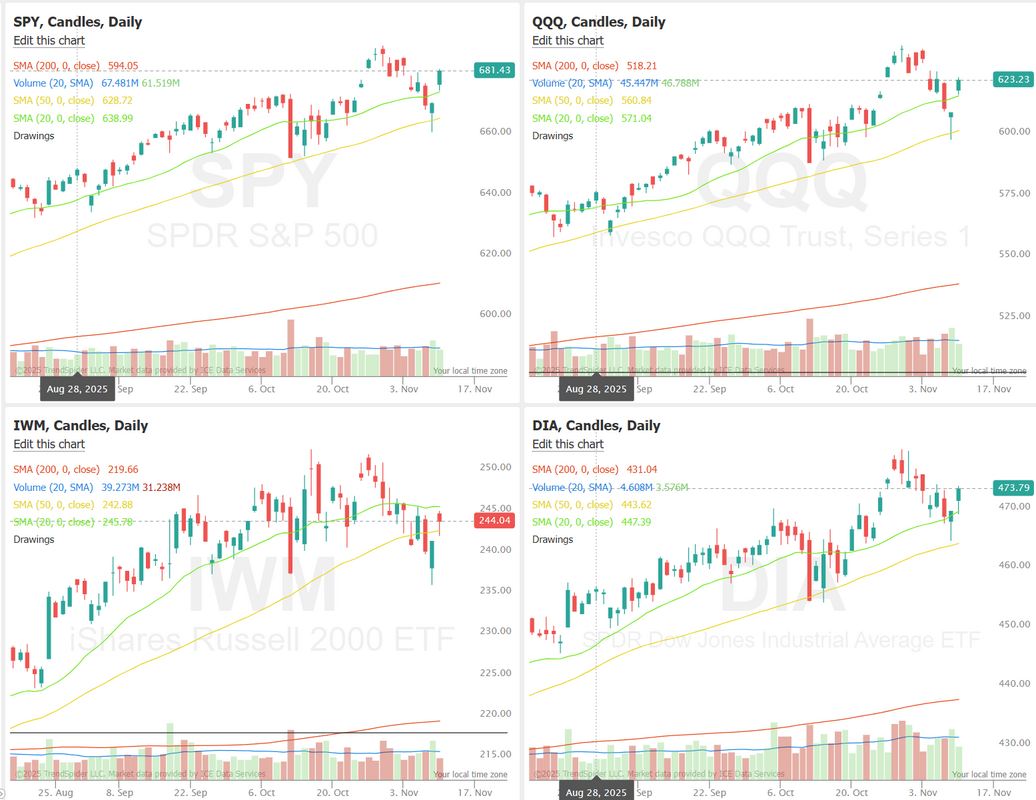

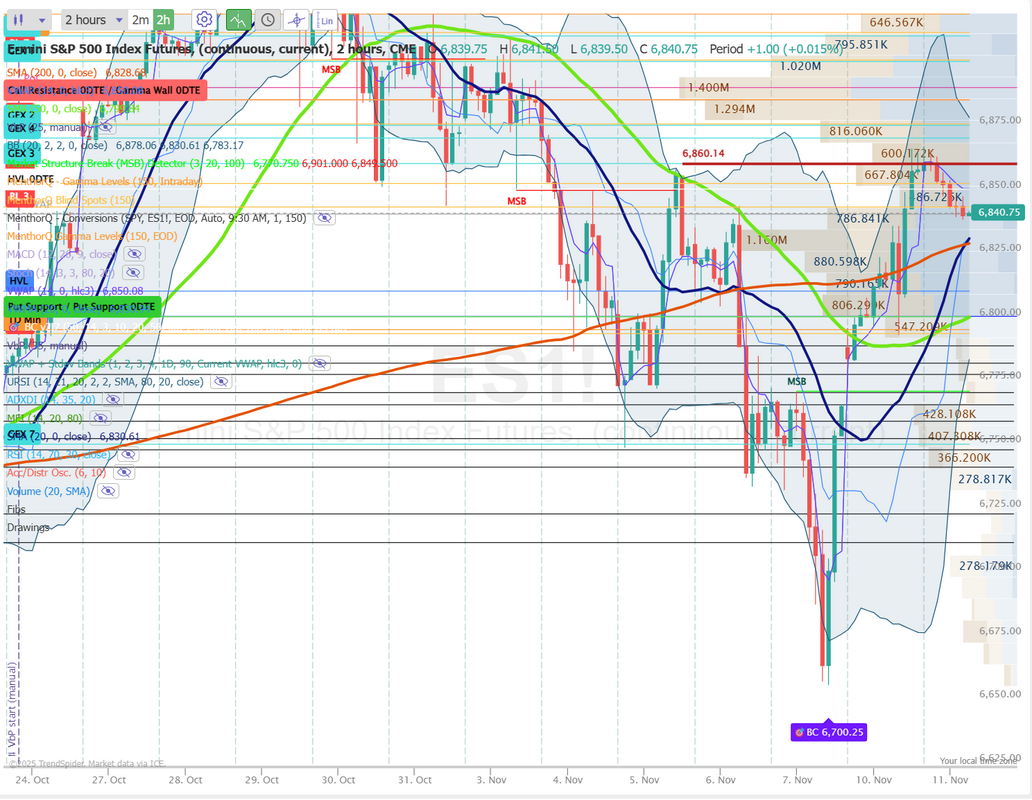

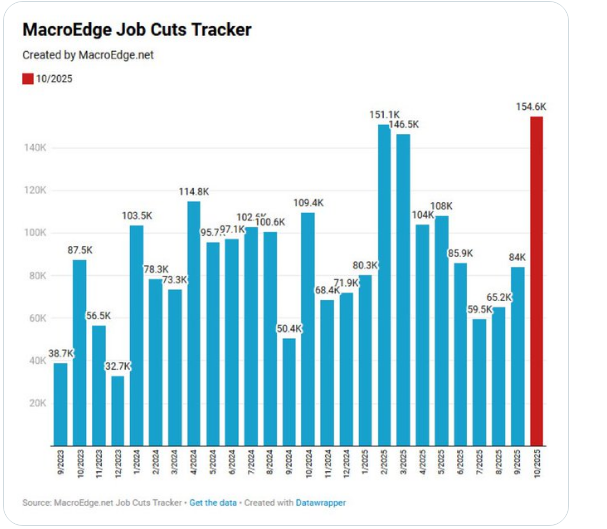

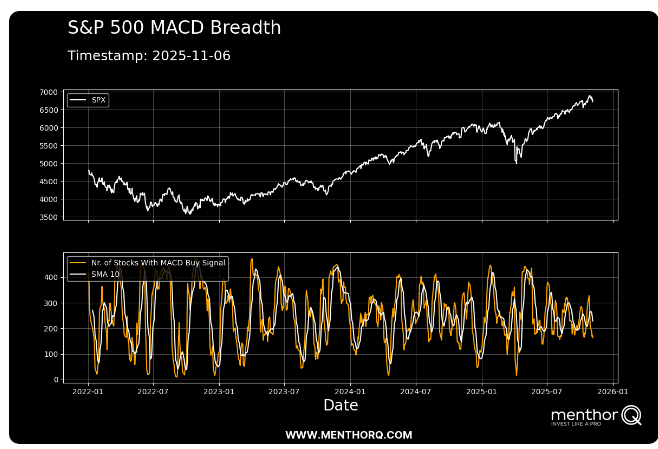

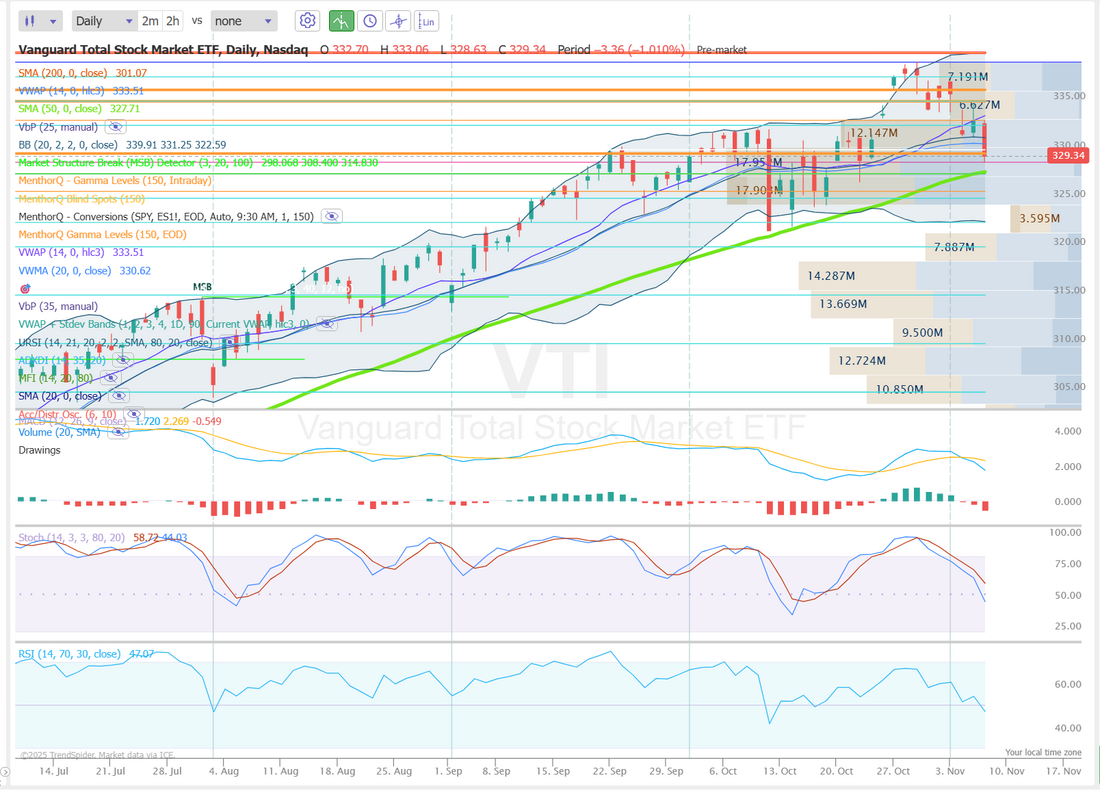

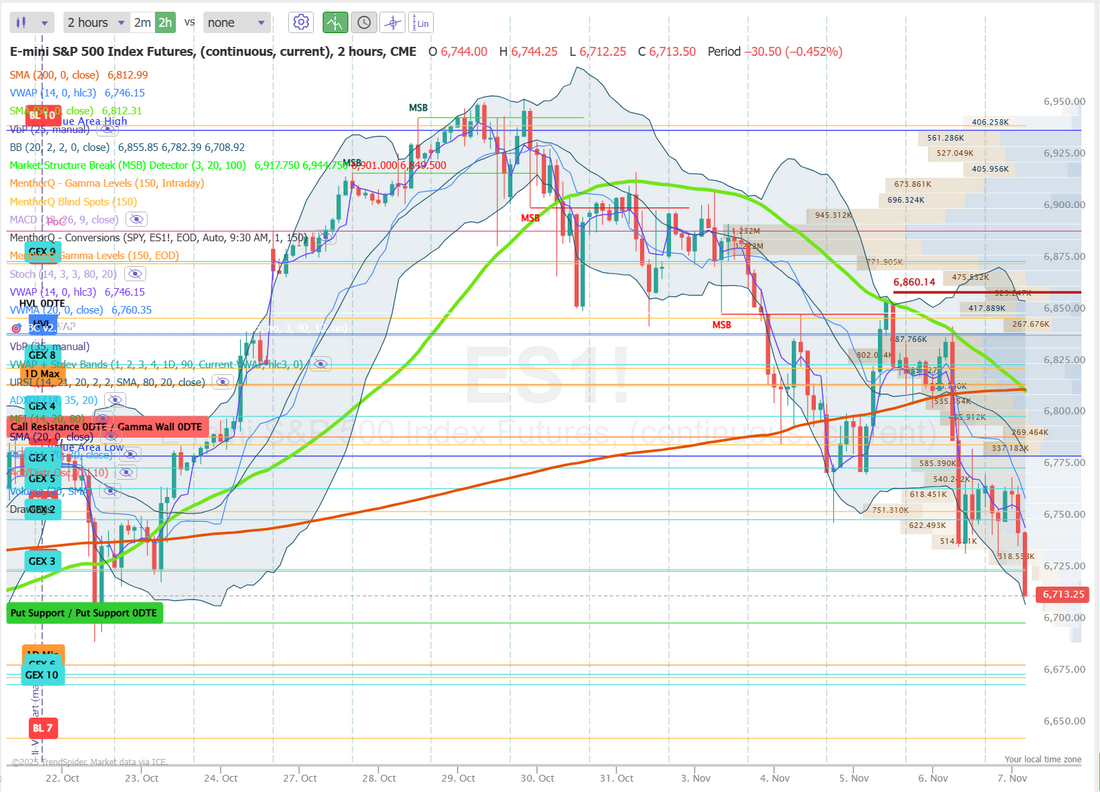

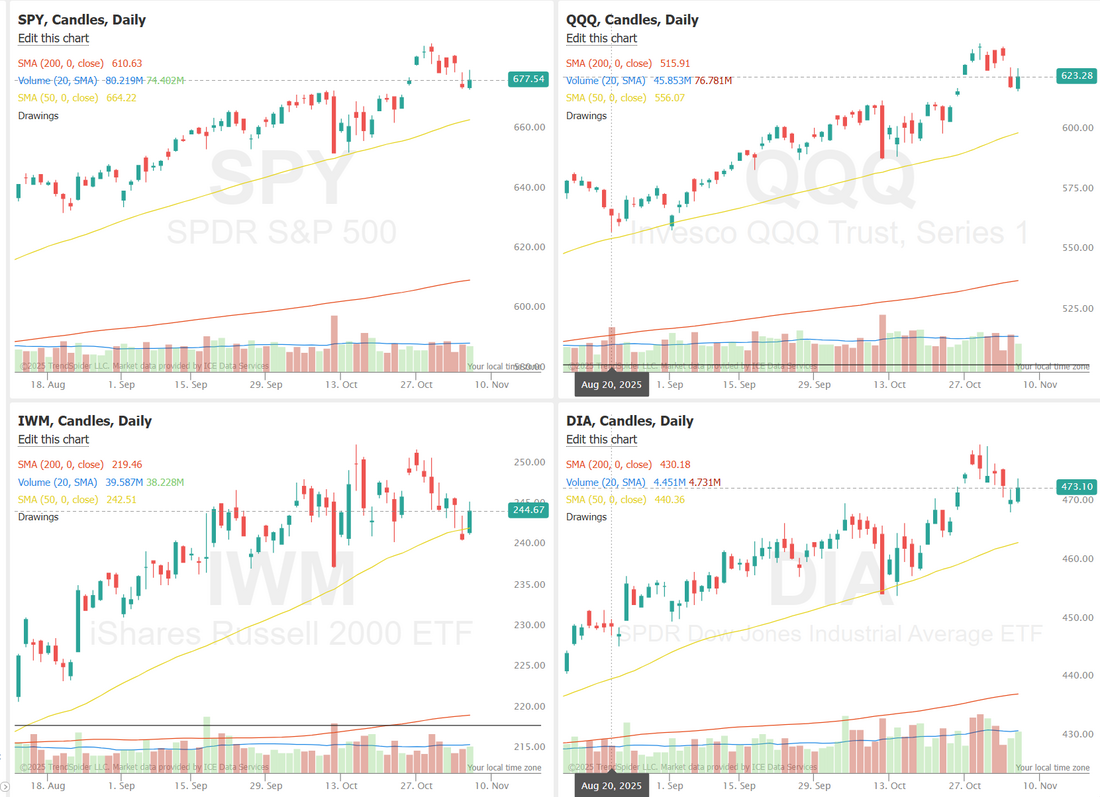

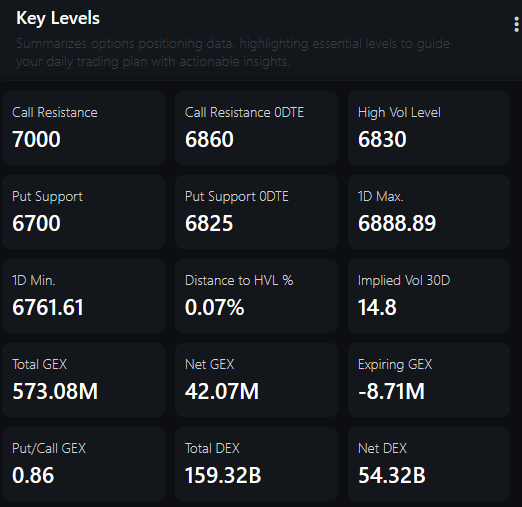

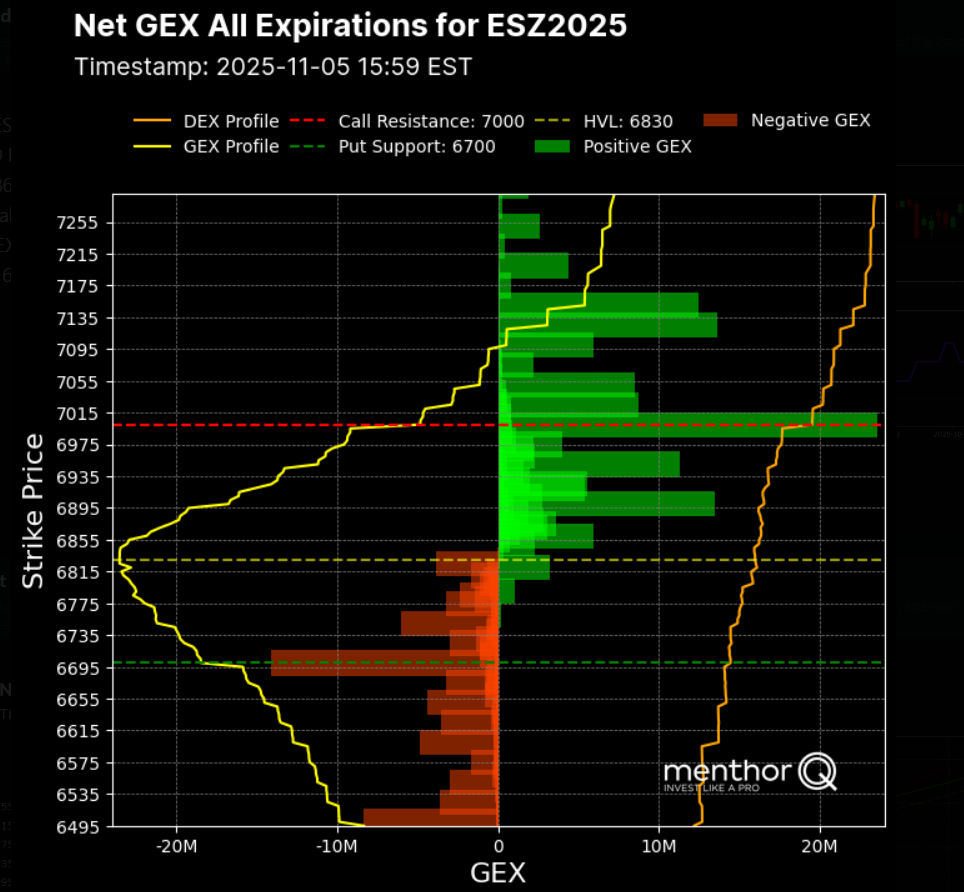

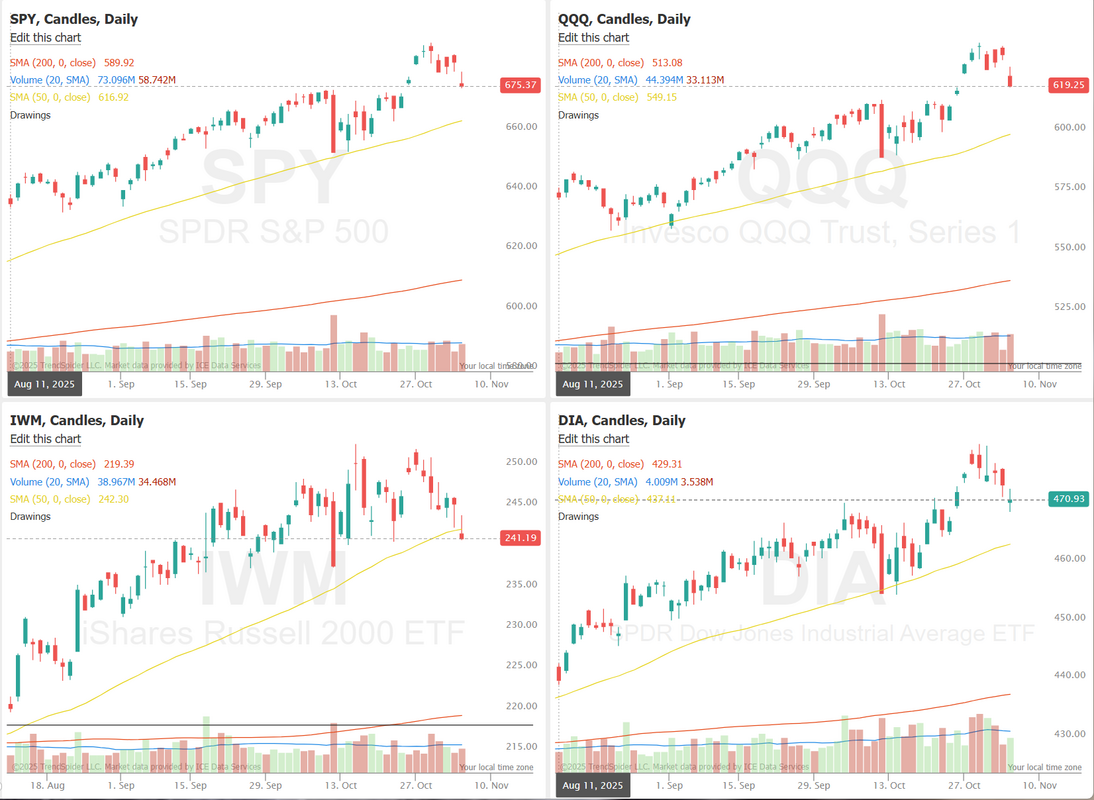

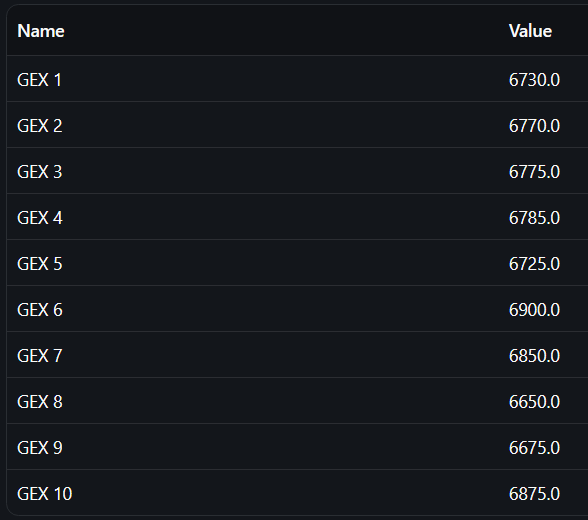

Ugly looking market=Beautiful profitsHow good was yesterday? Down markets are simply the best! It's everything we ask for, but it's more importantly, everything we are prepared for and set up to benefit from. Don't fear the reaper...be the reaper. Sorry, couldn't resist. Premium was just absolutely stellar. This is why we love down markets. It's been a long time since pure Theta trades made this much sense. We also had a solid day yesterday in our Asset allocation portfolio. It's built for days like this.  Here's a look at our day yesterday. ATM portfolio was great. It was a scalpers paradise and 0DTE premium was rich.  A 67% ROI on our used capital is extremely high without the help of debit trades. Let's take a look at the markets. It's not surprising, that the technicals are pointing bearish.  Something very big happened yesterday. We broke below the 50DMA on all the indices we track and trade. This hasn't happened in months and can be viewed as very bearish.  The SPX is pulling back from its recent highs, and the option score has slipped toward the lower end of its range, reflecting a cooling in short-term bullish appetite. Price action shows a series of lower highs forming over the past several sessions, hinting at a shift in momentum as sellers become more active on bounces. In the near term, the index appears to be consolidating between roughly 6,650 and 6,750, with repeated failures to reclaim the upper end of that zone. A continued low option score suggests hedging demand may be elevated, which can keep intraday swings choppy. Traders watching the short term may focus on whether SPX can stabilize above recent support or if another dip in the option score precedes a retest of last week’s lower levels.  Systematic flows in the Nasdaq appear to be rolling over, with the Q-CTA position trending lower just as the index itself shows signs of losing momentum after its recent peak. The sharp pullback in model-driven exposure suggests that trend-following programs are reducing risk as upside conviction softens. In the short term, this reduction in systematic demand could leave the index more sensitive to broader market volatility, especially if price continues to drift away from recent highs. Traders may watch whether Q-CTA positioning stabilizes or continues to unwind, as that shift often influences short-term liquidity and directional pressure.  December S&P 500 E-Mini futures (ESZ25) are trending down -0.31% this morning as investors continue to unload risk assets while awaiting Nvidia’s earnings and a pivotal U.S. jobs report. In yesterday’s trading session, Wall Street’s main stock indexes closed lower. Dell Technologies (DELL) plunged over -8% and was the top percentage loser on the S&P 500 after Morgan Stanley double-downgraded the stock to Underweight from Overweight with a price target of $110. Also, most chip stocks slumped, with Qualcomm (QCOM) sliding more than -4% and Marvell Technology (MRVL) falling over -3%. In addition, Hewlett Packard Enterprise (HPE) dropped more than -7% after Morgan Stanley downgraded the stock to Equal Weight from Overweight. On the bullish side, Alphabet (GOOGL) rose over +3% and was the top percentage gainer on the S&P 500 and Nasdaq 100 after Berkshire Hathaway disclosed a $4.9 billion stake in Google’s parent. Economic data released on Monday showed that the Empire State manufacturing index unexpectedly rose to a 1-year high of 18.70 in November, stronger than expectations of 6.10. Also, U.S. construction spending unexpectedly rose +0.2% m/m in August, stronger than expectations of -0.2% m/m. Fed Vice Chair Philip Jefferson said on Monday that risks to the labor market appear tilted to the downside, while reiterating that policymakers should move cautiously as interest rates approach neutral. At the same time, Fed Governor Christopher Waller reiterated his view that the central bank should lower interest rates again in December, pointing to a weak labor market. Meanwhile, initial jobless claims came in at 232K for the week ending October 18th, according to the Labor Department’s website. Data for the prior three weeks were not available. U.S. rate futures have priced in a 53.6% probability of no rate change and a 46.4% chance of a 25 basis point rate cut at the conclusion of the Fed’s December meeting. Today, investors will focus on U.S. Factory Orders data, which is set to be released in a couple of hours. The report was originally scheduled for release on October 2nd, but was delayed due to the government shutdown. Economists expect this figure to rise +1.4% m/m in August, following a -1.3% m/m drop in July. Market participants will also parse comments today from Fed Governor Michael Barr and Richmond Fed President Tom Barkin. On the earnings front, home improvement chain Home Depot (HD) is slated to release its Q3 results today. Earnings reports from big retailers throughout the week will provide additional insight into the health of the economy. Investor attention for the remainder of the week is squarely focused on Nvidia’s earnings report and the delayed September jobs report, with both events set to play a key role in shaping the outlook for markets throughout the rest of 2025. “The monthly jobs report would normally dominate this week’s economic calendar, but with the AI trade struggling the past couple of weeks, Nvidia’s earnings are once again looking like a key piece of the market’s momentum puzzle,” said Chris Larkin at E*Trade from Morgan Stanley. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.108%, down -0.56%.  The US federal debt surged +$620 billion during the 43-day government shutdown, to a record $38.151 trillion. This marks a +$14.4 billion increase per day.  The break in directional correlation between $SPX & $BTC quite profound. Happens rarely. Considering the depth of the sell off in crypto $SPX actually holding up quite well. So far. Risk is it spreads of course, flip side: Once $BTC bottoms markets could rip higher with it. TBD.  This is absolutely WILD: Retail investors have BOUGHT THE DIP every single week in 2025 whenever the S&P 500 fell over -1%, the 6th consecutive year their dip-buying rate stayed above 50. Meanwhile, institutional investors became dip buyers for the first time since 2019.  Guess what? Premium is back! Did I mention that? That means our vaunted Theta Fairy trade is back in play! We've got a modified version working for us today and likely will be able to get another one working this evening so keep your alerts on in discord for the working timestamp post. Yesterday we had a solid (and long) training session on part I of the top 12 books every trader should read. Tomorrow we start part II. Make sure to tune in. Implied I.V. is up in the 82% percentile. Should be another good day for premium collection.  My lean or bias today is bearish. It kind of has to be. We've had a lot of selling the past few days, so a rebound could be in the cards, but technicals are ugly, and we are below the 50DMA. Plus, who doesn't love a down market? Let's look at the intraday /ES levels for 0DTE setups today. 6675, 6691, 6700, 6725,6731 are resistance levels. 6650, 6633, 6625, 6618, 660, 6574 are support.  I look forward to seeing you all today in the live trading room. The market looks like it's shaping up to give us an ample opportunity to make a nice profit again today. Now it's up to us to capitalize on that opportunity. The data flow is back on.Finally, after more than a month without any economic data the spigot gets turned back on. It appears some of the data will be truncated but it's a step in the right direction. We've got NVDA earnings this week which may be even more important but it's looking less and less likely we get a rate cut next month. What a tricky day Friday. Bearish action in the morning with a big reversal later in the day. The market is in the throws of trying to divine a direction. We had to adjust our SPX which cut most of our profit potential there however it was a great day for scalping...again. Also, our ATM portfolio continues to hold up well to all this movement. We are not quite back to a new ATH there yet but we are close. Here's a look at our trades for Friday.  Today may be an interesting day for an NDX 0DTE. Premium is rich. Let's take a look at the markets. We start the day off with a sell signal technically.  Really interesting candles from Friday. They are green because futures started low and we finished higher by end of day but it was still a down day. The trend still continues to look bearish to me.  The latest SPX breadth readings across the 5-, 20-, and 50-day SMAs show a short-term improvement in participation, with the number of stocks trading above their respective moving averages stabilizing after a recent pullback. The 5-day breadth is especially choppy but has begun to turn higher, suggesting a pickup in very near-term buying pressure. The 20- and 50-day breadth measures remain in mid-range territory, indicating that while broader momentum hasn’t fully shifted, selling pressure has eased. In the short term, traders may watch whether these breadth lines continue pushing above their 10-day smoothers, continued follow-through would signal strengthening internal support for the index’s recent bounce, while a quick rollover would hint at fragility beneath the surface.  The QQQ volatility surface shows a clear skew toward elevated implied volatility at the very short-dated expirations, especially for deep out-of-the-money puts, where IV spikes above 70% and even over 100% in isolated strikes. This indicates strong demand for near-term downside protection, often a sign that traders are bracing for short-horizon catalysts or increased index movement. As expirations extend beyond two weeks, the surface flattens considerably, suggesting expectations for volatility to normalize over time. In the short term, the contrast between high front-end IV and relatively steady longer-dated levels highlights a market leaning defensive in the immediate window but not committing to a sustained volatility regime shift.  The SPX continues to hold near recent highs, but the Q-CTA positioning line has rolled over sharply, showing a clear reduction in systematic long exposure. This type of divergence price holding up while trend-following models begin to pare risk, often reflects fading momentum beneath the surface. In the short term, systematic flows may be less supportive than in previous weeks, which could leave the index more sensitive to volatility spikes or macro headlines. While not predictive on its own, the shift in Q-CTA positioning suggests a more cautious posture from rules-based strategies as the market navigates this elevated zone.  Monday news catalysts.  US tech CAPEX is EXPLODING: Tech capital expenditure has grown more over the last 5 years than during the 2000 dot-com bubble. Is this sustainable and will it pay off? Is this AI CapEx bubble and will burst?  This week we'll have a three part training on the top 12 books traders should read. We'll hit four each training session, Mon. Weds. Thurs. on our live zoom feed. Make sure to join in. These are always beneficial. Expected move for the SPX this week is 1.69%. That's some good premium. Credit trades may make more sense this week.  December S&P 500 E-Mini futures (ESZ25) are up +0.02%, and December Nasdaq 100 E-Mini futures (NQZ25) are up +0.09% this morning, pointing to a muted open on Wall Street as cautious sentiment prevailed at the start of a busy week. Investor focus this week is on an earnings report from AI bellwether Nvidia, the minutes of the Federal Reserve’s latest policy meeting, and the release of long-delayed U.S. jobs data. In Friday’s trading session, Wall Street’s major equity averages ended mixed. Most semiconductor stocks fell, with Lam Research (LRCX) sliding over -3% and ON Semiconductor (ON) dropping more than -2%. Also, Stubhub Holdings (STUB) tumbled about -21% after the company did not provide guidance for the current quarter. In addition, Bristol-Myers Squibb (BMY) slipped more than -4% after ending a trial of its experimental drug milvexian for stroke and blood-clot prevention due to disappointing data. On the bullish side, DoorDash (DASH) climbed over +6% and was the top percentage gainer on the S&P 500 and Nasdaq 100 after Needham called the stock’s recent pullback a buying opportunity and reiterated its Buy rating with a $275 price target. “The general trend has been to buy the dip, which could provide a respite. Retail investors may be spooked temporarily, but are likely to come back in if they believe the long-term story driving many of the names that have been gutted remains intact,” said Melissa Brown at SimCorp. Kansas City Fed President Jeff Schmid said on Friday that further interest rate cuts could do more to entrench higher inflation than to support the labor market. Also, Dallas Fed President Lorie Logan said, “I think it would be hard to support another rate cut unless we were to get convincing evidence that inflation is really coming down faster than my expectations or that we were seeing more than the gradual cooling that we’ve been seeing in the labor market.” In addition, Atlanta Fed President Raphael Bostic indicated that although he backed the most recent two rate cuts, he wasn’t yet persuaded about another move next month. Meanwhile, U.S. rate futures have priced in a 55.4% chance of no rate change and a 44.6% chance of a 25 basis point rate cut at the next FOMC meeting in December. In tariff news, the White House removed duties on imported coffee, bananas, and beef on Friday amid surging prices for some grocery staples. All eyes will be on Nvidia (NVDA) this week, dubbed “the most important stock on Earth” by Goldman Sachs, as the semiconductor giant reports its quarterly earnings on Wednesday. Nvidia’s earnings reports have been market-moving since May 2023, when the company delivered the revenue growth forecast that reverberated globally. Skepticism toward the AI trade is now at its highest level since before Nvidia’s 2023 forecast, putting pressure on the company to deliver with its upcoming report. Retailers such as Walmart (WMT), Home Depot (HD), TJX Companies (TJX), Lowe’s (LOW), and Target (TGT), along with notable companies like Palo Alto Networks (PANW), Intuit (INTU), and Copart (CPRT), are also set to release their quarterly results this week. Market participants continue to await further updates to economic data calendars from official statistics agencies. The Bureau of Labor Statistics said it will publish the September jobs report on Thursday, and the Census Bureau announced it will proceed with releasing reports on August construction spending, factory orders, and the trade balance. The data will gradually help clarify the state of the U.S. economy, though they’ll be more backward-looking than usual. Investors will also monitor private-sector data this week, including preliminary purchasing managers’ surveys on U.S. manufacturing and services sector activity, the National Association of Realtors’ existing home sales data, and the University of Michigan’s Consumer Sentiment Index. In addition, market watchers will parse the Fed’s minutes from the October 28-29 meeting, set for release on Wednesday, amid growing concerns over the central bank’s ability to cut interest rates next month. The FOMC lowered its benchmark rate last month for the second time this year, though Chair Jerome Powell cautioned that a December reduction is far from a “foregone conclusion.” Since then, a slew of Fed officials have voiced skepticism about the need for a rate cut next month, citing lingering uncertainty about inflation. Investors will hear perspectives from Fed officials Jefferson, Waller, Williams, Barr, Hammack, Cook, Goolsbee, Paulson, and Logan throughout the week. Today, investors will focus on the New York Fed-compiled Empire State Manufacturing Index, which is set to be released in a couple of hours. Economists expect the November figure to come in at 6.10, compared to 10.70 in October. The construction spending report for August will also be released today. Economists forecast this figure to be -0.2% m/m, compared to -0.1% m/m in July. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.127%, down -0.53%. My lean or bias today is bearish. I think the bulls are starting to take center stage here. Let's see if they can run with it. We can only hope! Let's take a look at the intraday /ES levels: Lots of tight levels this morning. 6752, 6759, 6765, 6770, 6777, 6781 are resistance levels. 6741, 6732, 6730, 6725, 6722, 6711 are support.  Let's make it happen today folks. I look forward to seeing you shortly in the live trading room. Hey 50DMA! Bye bye bye. We lost the 20DMA on the SPY and QQQ yesterday and we are losing the 50DMA this morning (as I type). We've been waiting for the bearish trend to really take hold.  To quantify how big the last two days rollover is, our delta on our ATM portfolio just turned positive! We generally try to always carry a negative delta. Might be time to add some more shorts! We had a STELLAR day yesterday. Low risk...high return... small trade size. Perfect for a day like yesterday. 6% ROI on the day and small buying power. Today may be the same. Keep risk low.  Let's take a look at the markets. No surprise. Bears are in full effect this morning.  As mentioned, yesterday we lost the 20DMA yesterday and it sure looks like we are set to lose the 50DMA this morning.  December S&P 500 E-Mini futures (ESZ25) are down -0.97%, and December Nasdaq 100 E-Mini futures (NQZ25) are down -1.29% this morning, pointing to further losses on Wall Street as worries over stretched tech valuations persisted and investors questioned whether the Federal Reserve was still on track to cut rates in December. In yesterday’s trading session, Wall Street’s three main equity benchmarks closed sharply lower. The Magnificent Seven stocks sank, with Tesla (TSLA) slumping over -6% and Nvidia (NVDA) falling more than -3%. Also, chip stocks slid, with Intel (INTC) and Lam Research (LRCX) dropping over -5%. In addition, Walt Disney (DIS) plunged more than -7% and was the top percentage loser on the Dow after the entertainment giant posted weaker-than-expected FQ4 revenue. On the bullish side, Cisco Systems (CSCO) rose over +4% and was the top percentage gainer on the Dow and Nasdaq 100 after the networking-equipment company reported better-than-expected FQ1 results and raised its full-year guidance. “The question now is whether the market’s recent exuberance has run its course. After a stellar rally since April, technology shares look increasingly overvalued and overstretched, with sentiment tempered by a lack of fresh catalysts and a lull in economic data,” according to Fawad Razaqzada at Forex.com. U.S. President Donald Trump signed legislation to end the longest shutdown in U.S. history late on Wednesday. The government reopening removes one source of investor uncertainty, paving the way for the release of delayed economic data, including the September jobs report, as early as next week. The Bureau of Labor Statistics is expected to issue a calendar in the coming days outlining new release dates for delayed data. President Trump’s top economic adviser, Kevin Hassett, told Fox News’ America’s Newsroom on Thursday that the October jobs report will be published without an unemployment rate reading. The data will be critical in shaping interest rate-cut expectations ahead of the Fed’s December meeting. Stubbornly high inflation and the weakening labor market are deepening the divide among Fed officials over the best path forward for interest rates. Cleveland Fed President Beth Hammack said on Thursday she remains focused on price stability even as the labor market weakens, emphasizing that reaching the central bank’s 2% inflation target is essential. Also, San Francisco Fed President Mary Daly said it is too early to determine whether policymakers should cut rates in December. In addition, St. Louis Fed President Alberto Musalem said policymakers should proceed cautiously with further rate cuts while inflation remains above the central bank’s target. Finally, Minneapolis Fed President Neel Kashkari said he did not support the last rate cut, though he remains undecided on the appropriate course of action for the December policy meeting. Meanwhile, U.S. rate futures have priced in a 49.6% chance of a 25 basis point rate cut and a 50.4% chance of no rate change at December’s policy meeting. On the trade front, a senior Trump administration official told reporters Thursday that the U.S. will eliminate tariffs on bananas, coffee, beef, and select apparel and textile goods under framework agreements with Argentina, Ecuador, Guatemala, and El Salvador, as part of efforts to address elevated food prices. Today, investors will focus on speeches from Kansas City Fed President Jeff Schmid, Dallas Fed President Lorie Logan, and Atlanta Fed President Raphael Bostic. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.114%, up +0.41%.  I want to take a moment to talk about (IMHO) the best way to approach the management of your hard earned capital. Three distinct approaches. #1. Scalping. #2. 0DTE's. #3. A unique asset allocation, passive portfolio. Scalping is what's kept me paying bills when I first started and had a minuscule amount of capital. It's a great way to have a good shot at generating daily income to live off, regardless of market conditions. 0DTE's keep you active and you only have to be right for a few hours a day. Our ATM portfolio takes 5 min. a day to manage. Has daily cash flow, carries shorts and well as longs. These all combine for a nice mix on days like yesterday. If you didn't make money yesterday or are worried about today it's not because you are a bad trader. You may just need a better strategy to manage your capital. This has NEVER happened: US stock market valuations have hit the highest level in modern history. Not even the periods before the 1930s Great Depression or the 2000 Dot-Com Bubble saw such expensive US stocks. US equities have never been more expensive.  Let's take a look at the intraday /ES levels. Should be another exciting day. 6690 first key resistance. 6702, 6750, 6766 are all resistance zones. 6679 is first support zone. 6660 is a big potential buy zone. 6651, 6625 are last big support zones for me today.  Let's finish strong today. It should be a great opportunity day. It's up to us now to capitalize! See you shortly in the live trading room. Everything's fixed!... for a few weeks.Well, the Government is back open. There's a lot of euphoria over it. Remember this isn't anything permanent. This budget fix will last a whopping 78 days before the next potential shutdown! Talk about just kicking the can down the road. That's fine for us traders. It just insures more uncertainty and volatility which is what we crave. I start my trading day early. Scanning charts, news and looking at the futures. Some mornings I just salivate and can't wait to get started. Some mornings are less exciting. Yesterday was the latter for me. If felt like a neutral technical day or even an FOMC morning where prices just float around with no inherent direction. I made a commitment to trade small and balance the cost of our SPX debit with what I thought could be a good day for scalping. It worked out o.k. I kept risk as small as I possibly could. 5-wide debit on SPX and only one contract on /MNQ scalping. The SPX didn't hit but risk was small all day. Today may be better with the potential for a "buy the rumor, sell the news" day. Do we sell back off today? It's certainly possible. Here's a look at my small day yesterday.  On the plus side, our ATM asset allocation model continues to perform well. Heading into the last part of the year. Let's take a look at the markets: Technicals are still holding to a buy mode to start the day.  The DIA continues to explode to the upside but everything else is a bit blah.  December S&P 500 E-Mini futures (ESZ25) are down -0.05%, and December Nasdaq 100 E-Mini futures (NQZ25) are down -0.08% this morning as investors weigh the outlook for the Federal Reserve’s interest rate path following the end of the longest government shutdown in U.S. history. U.S. President Donald Trump signed a spending bill to reopen the government late Wednesday, a measure passed by the Republican-controlled House after a record-long 43-day shutdown. The legislation cleared the House on a 222 to 209 vote, largely along party lines. The package extends federal government funding through January 30th and includes full-year funding for the Department of Agriculture, military construction, and the legislative branch. It will ensure that federal employees, including air-traffic controllers, receive their pay and return hundreds of thousands of furloughed government workers to their jobs. In yesterday’s trading session, Wall Street’s major indices ended mixed, with the Dow notching a new all-time high. Advanced Micro Devices (AMD) climbed +9% and was the top percentage gainer on the S&P 500 and Nasdaq 100 after forecasting faster sales growth over the next five years, fueled by strong demand for its data center products. Also, On Holding (ONON) jumped about +18% after the company posted upbeat Q3 results and raised its full-year guidance for revenue growth and adjusted EBITDA margin. In addition, BILL Holdings (BILL) surged over +11% after Bloomberg reported that the business-payments company was exploring options, including a potential sale. On the bearish side, most members of the Magnificent Seven stocks fell, with Meta Platforms (META) and Tesla (TSLA) sliding more than -2%. The government reopening removes one source of investor uncertainty, paving the way for the release of delayed economic data, including the September jobs report, as early as next week. The data will be critical in shaping rate-cut expectations ahead of the Fed’s December meeting. Still, White House Press Secretary Karoline Leavitt said on Wednesday that the October jobs and inflation reports are “likely never” to be published because of the shutdown. “All of that economic data released will be permanently impaired, leaving our policymakers at the Fed flying blind at a critical period,” Leavitt told reporters. Fed officials remain divided over which risk is more pressing—inflation or the weakening labor market. Boston Fed President Susan Collins said on Wednesday she favored keeping rates unchanged, given still-solid growth that could slow or hinder progress in bringing down inflation. Also, Atlanta Fed President Raphael Bostic stated that inflation remains the bigger risk to the economy and that he prefers keeping rates unchanged until it’s clear the central bank is on track to achieve its 2% target. “Despite shifts in the labor market, the clearer and urgent risk is still price stability,” Bostic said. At the same time, Fed Governor Stephen Miran reiterated that U.S. monetary policy is overly restrictive, arguing that easing housing inflation is helping to reduce overall price pressures. Meanwhile, U.S. rate futures have priced in a 53.9% probability of a 25 basis point rate cut and a 46.1% chance of no rate change at the next FOMC meeting in December. Today, market participants will hear perspectives from San Francisco Fed President Mary Daly, Minneapolis Fed President Neel Kashkari, St. Louis Fed President Alberto Musalem, and Cleveland Fed President Beth Hammack. On the economic front, investors will focus on the EIA’s weekly crude oil inventories report, set to be released in a couple of hours. Economists expect this figure to be 1.0 million barrels, compared to last week’s value of 5.2 million barrels. On the earnings front, prominent companies like Walt Disney (DIS) and Applied Materials (AMAT) are scheduled to report their quarterly figures today. According to Bloomberg Intelligence, S&P 500 companies are on track to post a +14.6% increase in Q3 profits from a year earlier, nearly twice the level analysts had projected. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.072%, up +0.17%. The S&P 500 breadth chart shows encouraging short-term improvement in market participation. The number of stocks trading above their 200-day moving average is starting to rise again, diverging positively from the 10-day moving average (SMA 10), which had been flattening out. This widening gap suggests that broader segments of the market are regaining strength, with more stocks participating in the recent index rebound. If this upward breadth momentum continues, it could reinforce short-term resilience in the S&P 500, as stronger participation often supports price stability and potential continuation of the prevailing trend.  Markets generally perform quite well after a Government shutdown.  Quantum stocks continue to retrace and we continue to short them in our ATM portfolio.  Let's take a look at the intraday levels on /ES. 6867, 6875, 6880, 6891, 6900 are resistance levels. 6860, 6850, 6843, 6839, 6827 are support.  No training session for today. My "off" day on Monday threw my schedule into a bit of flux. We'll be back next Monday with a whole new training module so make sure and tune in then on our live Zoom feed. I'll see you all shortly in the live trading room. I think today could be another good opportunity for scalping. Govt. back=Risk on?It looks like the Govt. shutdown could be over as soon as today. Futures are liking it and I'm going to assume that it will be risk on trading until we do get the eventual opening. Yesterday was spent digging out of holes. I started the scalping day down about $400 and down about $250 on SPX 0DTE. I was pretty happy to be able to turn those two around however a late day NDX failed...again. Two in a row there. Here's a look at my day. Not much to show for it.  Let's take a look at the markets. Technicals are popping to the upside. Futures are looking for the Govt. re-open.  Price action was impressive yesterday with the Dow which absolutely popped! Everything else was pretty flat.  December S&P 500 E-Mini futures (ESZ25) are trending up +0.35% this morning as optimism that the U.S. government shutdown is nearing an end boosted sentiment. A record 43-day U.S. government shutdown is poised to end as soon as today after the Senate passed a temporary funding bill. Reopening the government now depends on the House, which is set to return to Washington to consider the package. It would fund most parts of the government through January 30th and some agencies through September 30th. If approved, the bill will be sent to President Donald Trump, who has already voiced his support for the legislation. Investor focus is also on remarks from Federal Reserve officials. In yesterday’s trading session, Wall Street’s major indexes closed mixed. Paramount Skydance (PSKY) climbed over +9% and was among the top percentage gainers on the S&P 500 after the entertainment company issued above-consensus Q4 revenue guidance. Also, FedEx (FDX), often seen as a bellwether for the economy, rose more than +5% after the company projected that its profit this quarter would improve from a year ago. In addition, RealReal (REAL) jumped over +38% after the company posted better-than-expected Q3 results and raised its full-year revenue guidance. On the bearish side, Nvidia (NVDA) fell nearly -3% and was the top percentage loser on the Dow after Japan’s SoftBank Group disclosed it had sold its entire stake in the chipmaker for $5.83 billion. Once the government reopens, a wave of delayed economic reports is expected to be released, helping to clarify the outlook for interest rates. Jim Reid of Deutsche Bank stated that, based on historical precedent from the 2013 shutdown, September’s jobs report could be one of the first to be released, potentially within three business days of the government’s reopening. In the absence of official data, investors have turned to alternative indicators, including a report from ADP released on Tuesday. That report showed that the private sector lost an average of 11,250 jobs per week during the four weeks ending October 25th. The figures suggest that the labor market weakened in the latter half of October compared with the earlier part of the month. Separately, economists at Goldman Sachs estimated that U.S. payrolls fell by 50,000 in October after accounting for employees participating in the government’s deferred resignation program. Today, market participants will parse comments from a slew of Fed officials, including Williams, Paulson, Waller, Bostic, Miran, and Collins. Their remarks will be scrutinized closely amid the ongoing debate over whether another rate cut is needed at the December meeting. Meanwhile, U.S. rate futures have priced in a 63.4% chance of a 25 basis point rate cut and a 36.6% chance of no rate change at next month’s monetary policy meeting. On the earnings front, notable companies such as Cisco (CSCO), TransDigm Group (TDG), and GlobalFoundries (GFS) are slated to release their quarterly results today. According to Bloomberg Intelligence, S&P 500 companies are on track to post a +14.6% increase in Q3 profits from a year earlier, nearly twice the level analysts had projected. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.088%, up +0.44% The SPX Momentum Score shows signs of stabilization after recent short-term volatility, suggesting that bullish momentum may be regaining traction. The price has rebounded from last week’s dip and is now approaching prior resistance levels near the recent highs, supported by an improving momentum reading climbing back toward the upper range. This rebound indicates a potential shift in short-term sentiment as buyers regain control following a brief consolidation phase. However, given the choppy behavior over the past few sessions, traders appear focused on confirming sustained strength above these levels before committing to a broader directional move.  Todays training session we be another Jessie Livermore segment on "How to grow your wealth starting with zero". It should be another good session. Please tune in. My lean or bias today: It should be bullish. Technicals are all pointing up. Risk on seems to be back. The Govt. WILL open up at some point. Today? We're not sure but when it does it could provide an upward pop to the indices. Even if short term in nature. Today could be tricky It could be easy to get trapped in a bearish move when the news hits and markets pop. Be diligent today.  Let's take a look at the intraday levels on /ES. Several key levels. 6900* (key resistance), 6920, 6928* (key resistance) 6936, 6960* (key resistance). 6889, 6875, 6860, 6850, 6843* (key support)  I look forward to seeing you all back on zoom today. See you shortly! Does yesterday change the trend?We had a monster rebound yesterday after five very weak trading sessions. News that an end to the Govt. shutdown was near was enough to initiate a big relief rally. That makes sense. Some moves are harder to understand but this has generally been the pattern on re-openings. The real question is about its sustainability. Will this usher in another bull leg or is it only temporary? Futures are a tad weak this morning as we start the process of finding out. Word is it could be as early as tomorrow to get the Govt. back open. Let's see if it becomes a "buy the rumor, sell the news" event or not. I was out of commission most of the day yesterday with some low blood pressure issues. I did take one trade late in the day, looking for an NDX retrace going into the close but quickly got stopped out. Here's a look at it. Not much of a day for me.  Let's take a look at the market. Technicals are pointing bullish after yesterdays big push higher.  Yesterday's move higher was a solid gap up move. The question now is, will this gap get filled? Futures are suggesting it's a real possibility this morning.  The SPX option score is rebounding sharply after a brief pullback, aligning with a short-term bounce in spot prices following recent weakness. The score’s quick recovery to higher levels suggests renewed option market confidence and possibly a shift toward increased call positioning or reduced hedging activity. Price action shows the index stabilizing after testing support near recent lows, hinting that volatility compression could favor range-bound consolidation before the next directional move. In the near term, maintaining momentum above the mid-range levels will be key for sustaining bullish sentiment, while a drop in the option score could quickly reintroduce short-term downside pressure.  I wanted to take a moment and look at the bellwether A.I. stock (Nvidia). There seems to be a bit of a waning in A.I. stocks as more concerns of valuations and profitability come online. It seems to be at a crucial level. NVIDIA’s price action is consolidating near a key call resistance zone around $200, where significant gamma exposure (GEX) concentration suggests dealers may begin to hedge defensively if momentum stalls. The Gamma Wall at $195 marks a notable inflection level holding above it keeps the short-term tone stable, while a break below could open room toward support levels near $190 and $185. On the upside, if NVIDIA can sustain strength through $200, option positioning could fuel a gamma squeeze toward the next resistance clusters around $205–$210. The setup highlights a tightly balanced market where option flows may heavily influence short-term direction.  Of course, it goes without saying that as NVDA goes so goes most of the tech and A.I. marketplace. This is a key one to watch. December S&P 500 E-Mini futures (ESZ25) are down -0.22%, and December Nasdaq 100 E-Mini futures (NQZ25) are down -0.39% this morning, pointing to a lower open on Wall Street after yesterday’s rally amid renewed concerns over the valuations of some of the biggest beneficiaries of the AI boom. Sentiment weakened as Nvidia (NVDA) fell over -1% in pre-market trading after Japan’s SoftBank Group disclosed it had sold its entire $5.83 billion stake in the chipmaker, reigniting valuation concerns. Separately, CoreWeave (CRWV), which provides rental access to powerful AI chips, slumped more than -9% in pre-market trading after cutting its full-year revenue guidance. Also adding to the negative sentiment on Tuesday was a Wall Street Journal report stating that China will expedite rare earth export approvals for most firms while excluding those tied to the U.S. military. The move added fresh uncertainty about the durability of the trade truce between the world’s two largest economies. In yesterday’s trading session, Wall Street’s main stock indexes ended in the green. The Magnificent Seven stocks advanced, with Nvidia (NVDA) climbing over +5% to lead gainers in the Dow and Alphabet (GOOGL) rising more than +4%. Also, chip stocks rallied, with Micron Technology (MU) gaining over +6% and Advanced Micro Devices (AMD) rising more than +4%. In addition, TreeHouse Foods (THS) jumped over +22% after Investindustrial agreed to acquire the food processing company for about $2.9 billion. On the bearish side, health insurance stocks slumped after lawmakers moved closer to ending the shutdown without securing an extension of Affordable Care Act subsidies, with Oscar Health (OSCR) tumbling more than -17% and Centene (CNC) sliding over -8% to lead losers in the S&P 500. A record 42-day U.S. government shutdown is poised to end as soon as Wednesday after the Senate passed a temporary funding bill, with Democrats providing enough votes to push the measure through. The package now heads to the Republican-controlled House for a final vote before advancing to President Trump’s desk. Once the government reopens, a wave of delayed economic reports is expected to be released, helping to clarify the outlook for interest rates. “Reopening would not only boost sentiment, but also open the way for data releases, which could provide more insight into the health of the U.S. jobs market and, more broadly, the U.S. economy ahead of next month’s Federal Reserve interest-rate decision,” said Fiona Cincotta at City Index. Meanwhile, Vail Hartman, Delaney Choi, and Ian Lyngen at BMO Capital Markets noted that it would take several weeks for the market to receive all the data delayed since the start of the shutdown. Jim Reid of Deutsche Bank stated that, based on historical precedent from the 2013 shutdown, September’s jobs report could be one of the first to be released, potentially within three business days of the government’s reopening. Assuming the government reopens and data collection resumes, Fed officials will still face data compiled through retroactive surveys and other methods—if they are published at all. Analysts cautioned that the Bureau of Labor Statistics would likely be unable to gather and process data for both the October and November CPI reports ahead of the December FOMC meeting. And this comes at a time when the Fed is the most divided in recent memory. St. Louis Fed President Alberto Musalem said on Monday that he expects the U.S. economy to rebound sharply early next year, emphasizing that policymakers should exercise caution when considering further rate cuts. “It is very important that we tread with caution, because I believe there’s limited room for further reductions without monetary policy becoming overly accommodative,” Musalem said. At the same time, San Francisco Fed President Mary Daly said the economy is likely experiencing a slowdown in demand and cautioned against keeping rates too high for too long. Also, Fed Governor Stephen Miran said that better-than-expected inflation data and continued signs of labor market weakness support the case for a third consecutive rate cut in December. U.S. rate futures have priced in a 63.6% chance of a 25 basis point rate cut and a 36.4% chance of no rate change at the December FOMC meeting. The bond market is closed today for the Veterans Day holiday. Will they or won't they?One big question is will the FED lower rates again at its next meeting? A big part of that guessing game comes down to interpreting the data that had yet to be released, due to the shutdown. Several observers are noting that it will take quite a while to compile and release all that backlogged data. It's likely that some will still be pending when the FED needs to make a decision. Futures are almost down to a coin toss as to whether or not we get another cut this year. My lean or bias today: I'm going to lean or look for more bearishness. Yesterdays pop was understandable but I think the recent A.I. weakness and overall softness in the market, combined with weak futures offer the bears up another shot to refill the gap and continue the move lower. Let's take a look at some intraday levels. The daily chart on VTI doesn't offer up much guidance. Technicals and price action put us more neutral than anything.  On a tighter 2-hour. chart on /ES, we have a couple of big levels and lots of tiny levels. Pretty normal after a big move like we got yesterday. There is a big Gamma wall of resistance at 6884 and a big Gamma wall of support at 6700. That leaves a lot of levels in between. I'll work to point these out in Discord as the day progresses, so keep your chat room open as the day goes forward.  Warren Buffett is known for many, many wise quotes. One of my favorites is, "In the short term the market is a voting machine. In the long term it's a weighing machine." This simply means in the short term individual (or collective) opinion can move stocks is crazy ways but ultimately, at the end of the day, fundamentals come home to roost. There have been (and will continue to be) many Meme stocks that had spectacular runs in the short term, only to come back to reality over time, as fundamentals took focus.  It may be too early to call the A.I. stocks to this category of investments but it's something I'm certainly watching, and we are selectively building small, short positions in several of them in our ATM portfolio. I look forward to seeing you all in the live trading room today. Today may not offer up the opportunities of yesterday, but I think it will still be a good one. Goodbye 20DMA. Hello 50DMA!Well...as Phil Collins likes to say, it's another day in paradise.  Have our rain dance prayers finally been answered? All we've ever asked for is a down trending market. Is that so big an ask? LOL. I don't know. After two strong, back to back years of gains the market looked tired at the start of 2025 and I thought, if there was any year that looked poised to go down, this was the year. Instead its just held it's ground. I dare so however, this current rollover looks like it could be the real deal. The market seems to be getting tired of A.I. and Quantum computing stocks with no revenues or earnings to speak of. We love them, of course, from the short side. Our ATM portfolio is poised to profit again today if the market keeps dropping. We had a stellar day yesterday. Everything hit for us. Take a look below:  We had some excellent levels to work off yesterday. Today should be no different. There are some key support/resistance zones that have formed up. I'll touch on those in a moment. Let's look at the markets. Technicals are flashing sell.  As I mentioned above, We blew through the 20DMA yesterday on the SPY and QQQ. The 50DMA looks like it's incoming. A break below that would be glorious. IWM as already done so.  My lean or bias for today is bearish. Let's go bears! December S&P 500 E-Mini futures (ESZ25) are down -0.26%, and December Nasdaq 100 E-Mini futures (NQZ25) are down -0.30% this morning, extending yesterday’s losses as investors remain concerned about weak labor market data and lofty tech valuations. Investors are now awaiting the release of the University of Michigan’s preliminary reading on U.S. consumer sentiment and remarks from Federal Reserve officials. In yesterday’s trading session, Wall Street’s major indices ended sharply lower. Most members of the Magnificent Seven stocks retreated, with Tesla (TSLA) and Nvidia (NVDA) dropping over -3%. Also, chip stocks slumped, with Advanced Micro Devices (AMD) sliding over -7% and Qualcomm (QCOM) falling more than -3%. In addition, DoorDash (DASH) plunged over -17% and was the top percentage loser on the S&P 500 and Nasdaq 100 after the food-delivery company reported weaker-than-expected Q3 EPS and issued soft Q4 adjusted EBITDA guidance. On the bullish side, Datadog (DDOG) jumped more than +23% and was the top percentage gainer on the S&P 500 and Nasdaq 100 after the software maker posted upbeat Q3 results and raised its full-year guidance. Data from outplacement firm Challenger, Gray & Christmas released on Thursday showed that U.S. companies announced 153,074 job cuts in October, nearly three times higher than the same month last year and the highest for any October since 2003. Separately, Revelio Labs data showed that the U.S. shed 9,100 nonfarm jobs in October after adding 33,000 in the previous month. “We are sticking to our view that the Fed will deliver a follow-up 25 basis-point cut in December because restrictive Fed policy can worsen the already fragile employment backdrop,” said Elias Haddad at Brown Brothers Harriman & Co. Still, a slew of remarks from Fed officials on Thursday regarding inflation left traders uncertain about whether a December rate cut will materialize. Cleveland Fed President Beth Hammack said monetary policy needs to keep putting downward pressure on inflation, which she views as too high and a greater risk than labor market weakness. Also, Fed Governor Michael Barr said policymakers still have work to do in bringing down inflation to the central bank’s 2% target while ensuring the labor market is solid. In addition, Chicago Fed President Austan Goolsbee said a lack of official inflation data during the shutdown makes him cautious about cutting rates. Finally, St. Louis Fed President Alberto Musalem said the central bank needs to maintain downward pressure on inflation, warning that interest rates are nearing a level where that pressure could diminish. U.S. rate futures have priced in a 66.0% chance of a 25 basis point rate cut and a 34.0% chance of no rate change at the next FOMC meeting in December. Meanwhile, the longest government shutdown in U.S. history is now in its 38th day. U.S. officials have said they will reduce air traffic by 10% at 40 major airports starting today to ease pressure on air-traffic controllers who remain unpaid due to the shutdown. Economists noted that every week of the shutdown reduces quarterly annualized growth by 0.1 to 0.2 percentage points. Still, several lawmakers have expressed optimism that the shutdown could end this weekend. In light of the shutdown, the publication of October’s nonfarm payrolls report, average hourly earnings, and unemployment rate, originally set for today, will be delayed. Still, the University of Michigan’s U.S. Consumer Sentiment Index will be released today. Economists, on average, forecast that the preliminary November figure will stand at 53.0, compared to 53.6 in October. The Fed’s Consumer Credit report will also be released today. Economists expect the U.S. Consumer Credit to be $10.4 billion in September, compared to the previous figure of $0.4 billion. In addition, market participants will be looking toward speeches from Fed Vice Chair Philip Jefferson, New York Fed President John Williams, and Fed Governor Stephen Miran. On the earnings front, notable companies like Constellation Energy (CEG), KKR & Co. (KKR), Enbridge (ENB), and Duke Energy (DUK) are set to report their quarterly figures today. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.106%, up +0.32%. The last two days the SPX dropped about 30 handles in 30 mins. This is a nice sign of weak hands. Markets can't hold going into the close. Everyone wants to be risk-off overnight.  If you're worried about jobs numbers, you should be. Job cuts are skyrocketing.  The S&P 500 MACD Breadth chart highlights a moderate cooling in short-term momentum as the number of stocks with active MACD buy signals has eased from recent peaks. While the SPX index remains in an uptrend, breadth readings show fewer constituents participating in the rally, suggesting a potential pause or minor consolidation phase ahead. Historically, similar dips in MACD breadth have preceded short-term pullbacks or sideways movement before trend resumption. In the near term, traders may watch whether breadth stabilizes or rebounds, as a renewed rise in MACD buy signals could confirm fresh upside participation across sectors.  Gamma has flipped negative!  Quant score in plummeting.  Let's take a look at our intraday readings. We've got a textbook sell rating on the market right now. Rollover on Stoch, RSI, MACD. We just need a break below the 50DMA (green line) to really lock this bearish trend down.  6725, 6740, 6749, 6754, 6766 are resistance levels. 6711, 6700, 6680, 6674, 6660, 6644 are support.  We had another great training session yesterday on Attribution analysis. Join us Monday for a training session on the Options smile skew. It should be another good one! I'll see you all shortly in the live trading room. Remember...there ain't no market like a down market. Let's go bears! Big recovery=Big win?Lot's of lessons for me in yesterdays trading session. Both with our 0DTE SPX and Scalping the /MNQ futures. I got upside down on our SPX early in the day. Down about $1,000 dollars. I generally try to keep risk at no more than $500. We had an amazing reversal trade that almost brought us back to profits. It would have been almost $600 of profit IF, I would have abided by our level analysis and waited a bit longer to enter the retrace setup. I got a bit ahead of myself and our laid out gameplan. In scalping I went with 4 contracts which is a bit heavier than normal but the main issue was looking for the retrace a bit too early. It came. Again, I was just too anticipatory. I love the retrace trade. You can call me Scott "reversion to the mean" Stewart. The problem comes when it doesn't show up.. or shows up too late. A $45 dollar loss on SPX is hard to categorize as a win until you understand you were staring down a $1,000 loss. Today is a new day. Here's a look at my day.  Let's take a look at the markets. Technicals are in a bit of a flux. Neutral rating to start today. That's always a tough one to read so I'll be a bit more patient to get started today.  I would actually call yesterday a bearish day. Yes the IWM and DIA had a well deserved push higher after lots of negative days but the SPY and QQQ actually had a very bearish finish to the day, despite being up strong most of the day.  December S&P 500 E-Mini futures (ESZ25) are up +0.16%, and December Nasdaq 100 E-Mini futures (NQZ25) are up +0.20% this morning, pointing to a higher open on Wall Street as Treasury yields fell amid growing expectations for a Federal Reserve rate cut in December. Bond yields fell after data from outplacement firm Challenger, Gray & Christmas showed that U.S. companies announced the highest number of job cuts for any October in over two decades, prompting traders to increase wagers on a rate cut next month. Investors now await a slew of speeches from Federal Reserve officials for more clues on the interest rate outlook. Still, concerns over lofty tech valuations persisted, limiting gains in U.S. equity futures. Qualcomm (QCOM) fell over -2% in pre-market trading, becoming the latest chipmaker to issue upbeat guidance that nonetheless failed to impress investors. In yesterday’s trading session, Wall Street’s three main equity benchmarks closed in the green. Chip stocks rallied, with Micron Technology (MU) climbing over +8% and Marvell Technology (MRVL) rising more than +6%. Also, Amgen (AMGN) surged over +7% and was the top percentage gainer on the Dow after the biotech giant posted upbeat Q3 results and raised its full-year guidance. In addition, Lumentum Holdings (LITE) jumped more than +23% after the company reported better-than-expected FQ1 results and issued strong FQ2 guidance. On the bearish side, Zimmer Biomet Holdings (ZBH) plunged over -15% and was the top percentage loser on the S&P 500 after the maker of knee and hip replacements posted weaker-than-expected Q3 sales. The ADP National Employment report released on Wednesday showed that U.S. private nonfarm payrolls rose by 42K in October, stronger than expectations of 32K. Also, the U.S. ISM services index rose to 52.4 in October, stronger than expectations of 50.7. At the same time, the U.S. October S&P Global services PMI was revised lower to 54.8 from the preliminary reading of 55.2. Fed Governor Stephen Miran said on Wednesday that the ADP report showing an increase in employment at companies was “a welcome surprise,” though he reiterated that interest rates should be lower. U.S. rate futures have priced in a 67.3% probability of a 25 basis point rate cut and a 32.7% chance of no rate change at December’s monetary policy meeting. Third-quarter corporate earnings season rolls on, with notable companies like ConocoPhillips (COP), Airbnb (ABNB), Monster Beverage (MNST), Vistra Corp. (VST), Warner Bros Discovery (WBD), and Take-Two Interactive Software (TTWO) slated to release their quarterly results today. According to Bloomberg Intelligence, companies in the S&P 500 are expected to post an average +7.2% increase in quarterly earnings for Q3 compared to the previous year, marking the smallest rise in two years. Market participants will also hear perspectives from Fed Governors Christopher Waller and Michael Barr, along with New York Fed President John Williams, Cleveland Fed President Beth Hammack, and Philadelphia Fed President Anna Paulson, throughout the day. Meanwhile, the U.S. government shutdown has entered its 37th day. The shutdown has become the longest in U.S. history, surpassing the previous record on Tuesday night. In light of the shutdown, the publication of weekly jobless claims as well as preliminary third-quarter nonfarm productivity and unit labor costs data, originally set for today, will be delayed. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.139%, down -0.48%. The SPX Volatility Score chart indicates a cooling in short-term volatility after a brief spike in mid-October. While the index remains near its recent highs, the modest pullback in the volatility score suggests a more stable, range-bound environment as traders digest recent gains. Price action has shown resilience above the 6,700 zone, but fading volatility could mean tighter intraday swings and reduced momentum in the immediate term. If volatility picks up again, it may coincide with renewed market catalysts such as earnings or macro data releases, key short-term factors to watch as the SPX tests whether this consolidation becomes a pause before continuation or a shift toward rebalancing.  We were too occupied with our SPX trade yesterday to get into our Attribution training. We'll hit it today. Come join us. I try to with hold a lean or bias on neutral rated mornings. It's just too much of a coin toss. Futures are trending higher and looking to open strong. Let's look at the setups for today's 0DTE SPX trade based off /ES futures levels.  Quant score building momentum.  GEX levels across all expirations.  Intraday levels. 6842 (current level as I type) is key 50PMA on 2hr. chart. 6850 is also key (MSB- Market structure break level), 6860, 6875, 6890 are the remaining resistance levels for me today. Support starts at 6830, 6825, 6820, 6810, 6800.  I look forward to seeing you all in the live trading room shortly. Yesterday was a great save. Let's see if we can just skip the "save" part today and go straight to profit. Down market = Up profitsYesterday was everything we (I) ask for as traders. I've talked endlessly about how I love big down days. Let me expand on why I think they are the best trading environment. #1. Movement. As traders we just want movement. Nice clean (not erratic) moves. This is obviously the best situation for our scalping efforts. It also lends itself to the use of debit trades. Those give us a bit better leverage than credit setups. #2. Down trends. Markets usually have bigger moves down than up. It also pumps I.V. into the options premium, making credit trades better risk/reward. In short, downward trending days give us the best chance to use all our tools. Scalping, Debit and credit trades. Here's a look at our day yesterday.  Let's take a look at the markets. Sell mode it still engaged this morning although, futures are trying to fight back as I type.  Do I see an actual bearish trend? Maybe on the IWM and DIA but SPY and QQQ have really just made a round trip from where they broke out to the upside a couple weeks ago.  December Nasdaq 100 E-Mini futures (NQZ25) are trending down -0.57% this morning as investors digested weak earnings from notable tech players such as Advanced Micro Devices and Super Micro Computer, while concerns over lofty tech valuations continued to weigh on sentiment. Advanced Micro Devices (AMD) slid over -4% in pre-market trading after the chipmaker’s Q4 revenue guidance failed to impress investors. Also, Super Micro Computer (SMCI) plunged more than -9% in pre-market trading after the server maker posted weaker-than-expected FQ1 results and gave a disappointing FQ2 adjusted EPS forecast. Investors now await the U.S. ADP employment report and a new round of corporate earnings reports. In yesterday’s trading session, Wall Street’s major indexes closed sharply lower. The Magnificent Seven stocks retreated, with Tesla (TSLA) sliding over -5% and Nvidia (NVDA) falling nearly -4%. Also, chip stocks slumped, with Micron Technology (MU) dropping over -7% and Intel (INTC) falling more than -6%. In addition, Palantir Technologies (PLTR) sank over -7% amid valuation concerns, despite the data analytics company reporting upbeat Q3 results and raising its full-year revenue guidance. On the bullish side, Expeditors International of Washington (EXPD) climbed more than +10% and was the top percentage gainer on the S&P 500 after the company posted better-than-expected Q3 results. “This reinforces our thinking that the stock market is ripe for some sort of material pullback over the near-term, no matter where it’s going over the intermediate/longer-term,” said Matt Maley at Miller Tabak. On the trade front, China’s Customs Tariff Commission of the State Council announced on Wednesday that it will extend the suspension of a 24% tariff on some U.S. goods for another year while keeping a 10% duty in place, as part of the trade truce agreed at last month’s Trump-Xi summit. The commission also stated that it would lift tariffs of up to 15% on certain U.S. agricultural products. In addition, China will remove export controls against 15 U.S. entities and extend the suspension of such measures for another year for 16 others. The measures are set to take effect on November 10th. Third-quarter corporate earnings season continues, and investors await new reports from prominent companies today, including McDonald’s (MCD), Applovin (APP), Qualcomm (QCOM), Arm (ARM), Robinhood Markets (HOOD), McKesson (MCK), and DoorDash (DASH). According to Bloomberg Intelligence, companies in the S&P 500 are expected to post an average +7.2% increase in quarterly earnings for Q3 compared to the previous year, marking the smallest rise in two years. On the economic data front, all eyes are on the U.S. ADP private payrolls report, which is set to be released in a couple of hours. The report will provide fresh insights into the health of the labor market. Economists, on average, forecast that the October ADP Nonfarm Employment Change will stand at 32K, compared to the September figure of -32K. The U.S. ISM Non-Manufacturing PMI and S&P Global Services PMI will also be closely monitored today. Economists expect the October ISM services index to be 50.7 and the S&P Global services PMI to be 55.2, compared to the previous values of 50.0 and 54.2, respectively. U.S. Crude Oil Inventories data will be released today as well. Economists expect this figure to be -2.5 million barrels, compared to last week’s value of -6.9 million barrels. Meanwhile, the U.S. government shutdown has entered its 36th day, becoming the longest in history. On Tuesday, the Senate failed for the 14th time to pass a bill that would have reopened the government through November 21st. Still, lawmakers from both parties have hinted at the emerging outlines of a deal to end the shutdown, potentially as soon as this week. The Supreme Court is set to hear arguments later today in the case against President Trump’s use of the International Emergency Economic Powers Act to impose sweeping tariffs. The court will hear arguments from three lawyers, one representing the Trump administration and two representing the small businesses and states contesting the legality of the tariffs. U.S. rate futures have priced in a 69.9% chance of a 25 basis point rate cut and a 30.1% chance of no rate change at the December FOMC meeting. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.088%, down -0.05%. My lean or bias today: Not sure. Futures have been on a wild ride overnight. Absolutely tanking and then fighting back only to slip again and now fighting back...again. Every sell this year has been bought up. Technicals are bearish. Futures are red (although coming back) and yet I have a feeling today will be an up day.  Todays training will be on Attribution analysis. This should be another good one. Tune in live at 12:00 noon MT. The SPX option score chart shows a short-term softening in sentiment following the recent push to local highs near 6,900, as the option score dropped sharply from 5 to 1, hinting at a cooling of bullish positioning in the derivatives market. This pullback aligns with the minor retracement seen in spot prices after a strong multi-week rally. The data suggests that option flows have turned more cautious, possibly reflecting traders hedging recent gains or anticipating short-term consolidation. If the option score stabilizes and rebounds, it could indicate renewed demand for upside exposure, but for now, the momentum appears to favor a pause or mild correction as markets digest recent strength.  Intraday Gamma Levels 0DTE for SPX on 2025-11-05Spot Price used: Last Intraday Price (not provided explicitly, analysis based on levels) Date: 2025-11-05 Primary LevelsCall Resistance:

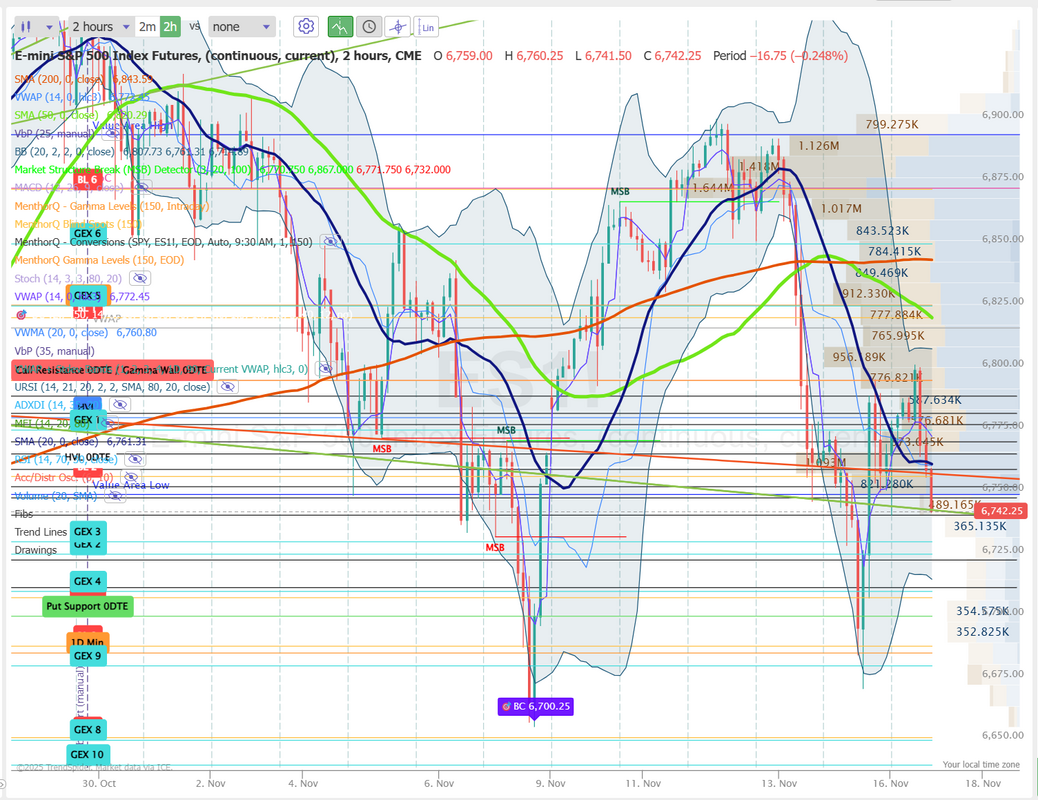

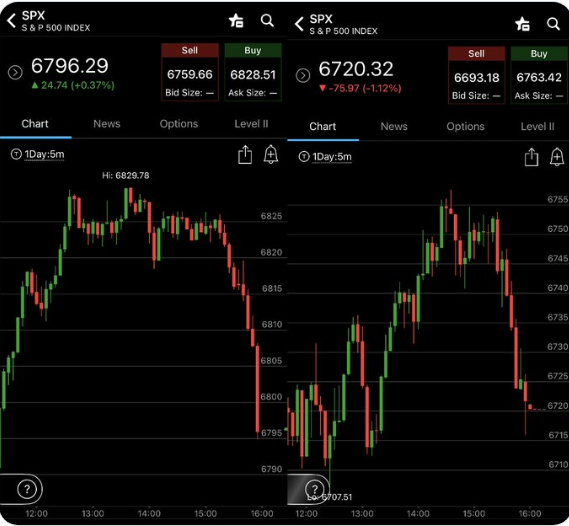

Let's take a look at the chart for intraday levels on /ES. 6800 is the first BIG resistance level. It's a big phycological level as well as the 200 period M.A. on the 2hr. chart 6821, 6825, 6839, 6850 (another big level). Support levels start at 6781. Bears need to get below this level to continue any downside bias. 6775, 6765, 6759 are the next levels.  I'll see you all in the live trading room shortly. Let's see if the bulls can take hold today. |

Archives

November 2025

AuthorScott Stewart likes trading, motocross and spending time with his family.

|