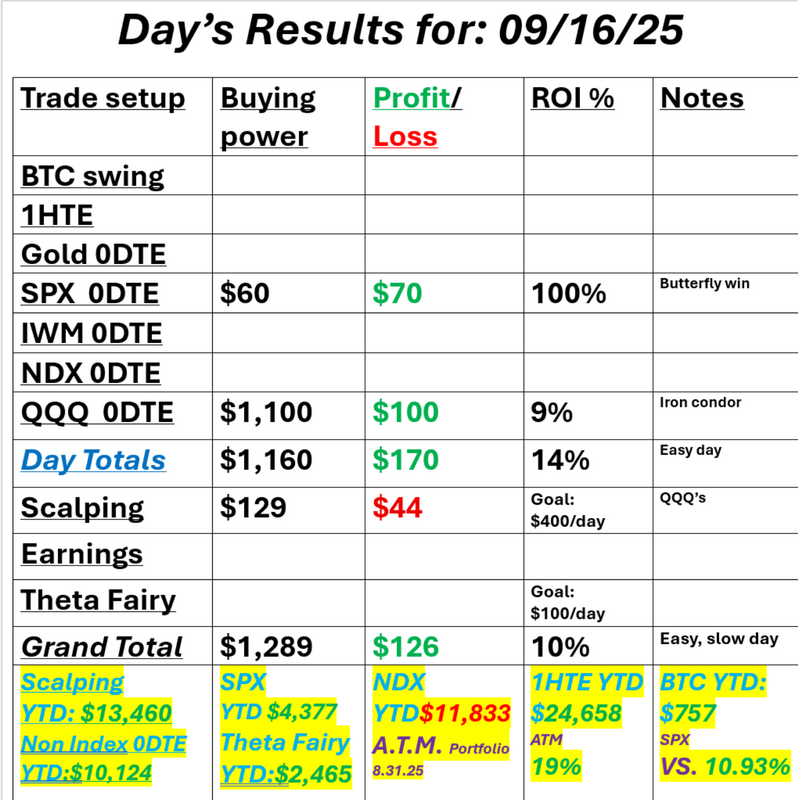

FOMC day is hereDo we get a rate cut as most believe? Is it the 25bp that's expected or a more aggressive 50bp? Most important (probably) will be what Powell says about the future. How hawkish or dovish he'll be. This will set the stage for the next two potential decisions for the rest of this year. Regardless of all this, it should be a good day for traders with ample movement to trade. The options market is implying a .07% move for the day. Come trade with us. These days are usually pretty good.  My lean or bias yesterday was for a neutral day will little movement and that's exactly what we got. We traded small and it was a successful and non eventful day. We placed a 0DTE on the QQQ's which expired fully profitable and a butterfly on the SPX which doubled in value. See our results below:  September S&P 500 E-Mini futures (ESU25) are up +0.01%, and September Nasdaq 100 E-Mini futures (NQU25) are down -0.04% this morning as investors refrain from making any big bets ahead of a highly anticipated Federal Reserve interest rate decision. Stock index futures’ subdued tone reflects investor caution over how the Fed will signal the interest-rate path, with a quarter-point cut at this meeting and three more by April already priced in. In yesterday’s trading session, Wall Street’s major indexes ended slightly lower. Warner Bros. Discovery (WBD) slumped over -6% and was the top percentage loser on the S&P 500 and Nasdaq 100 after TD Cowen downgraded the stock to Hold from Buy. Also, Rocket Lab (RKLB) tumbled more than -12% after the rocket launch company announced a $750 million at-the-market equity offering. In addition, Dave & Buster’s Entertainment (PLAY) plunged over -16% after the arcade-restaurant operator posted downbeat Q2 results. On the bullish side, chip stocks gained ground, with ON Semiconductor (ON) rising more than +3% to lead gainers in the Nasdaq 100 and Marvell Technology (MRVL) advancing over +2%. Economic data released on Tuesday showed that U.S. retail sales climbed +0.6% m/m in August, stronger than expectations of +0.2% m/m, and core retail sales, which exclude motor vehicles and parts, grew +0.7% m/m, stronger than expectations of +0.4% m/m. Also, U.S. August industrial production unexpectedly rose +0.1% m/m, stronger than expectations of -0.1% m/m, and manufacturing production unexpectedly rose +0.2% m/m, stronger than expectations of -0.2% m/m. In addition, the U.S. import price index unexpectedly rose +0.3% m/m in August, stronger than expectations of -0.2% m/m. “The American consumer appears to be in good spirits. That’s good news for the economy, but it may heighten debate over how aggressively the Fed needs to cut rates,” said Ellen Zentner at Morgan Stanley Wealth Management. Today, all eyes are focused on the Federal Reserve’s monetary policy decision. The Federal Open Market Committee is widely expected to cut the Fed funds rate by 25 basis points to a range of 4.00% to 4.25%. Market watchers will follow Chair Jerome Powell’s post-policy meeting press conference for any indications on how quickly rates may fall from here. Following recent data painting a picture of a slowing labor market, U.S. money markets have almost fully priced in follow-up rate cuts in October and December. Market participants will also closely parse the Fed’s quarterly “dot plot” in its Summary of Economic Projections, which will offer key guidance on how policymakers expect the interest-rate path to unfold over the next few years. The equity options market is predicting about a 0.7% move after the Fed meeting, matching the second-lowest expected swing in the past 18 months, according to data from Susquehanna International Group. A survey conducted by 22V Research revealed that 43% of respondents are leaning “risk-on” in reaction to the Fed meeting, 31% said “mixed/negligible,” and 26% said “risk-off.” On the economic data front, investors will focus on U.S. Building Permits (preliminary) and Housing Starts data, set to be released in a couple of hours. Economists expect August Building Permits to be 1.370 million and Housing Starts to be 1.370 million, compared to the prior figures of 1.362 million and 1.428 million, respectively. U.S. Crude Oil Inventories data will be released today as well. Economists expect this figure to be 1.400 million, compared to last week’s value of 3.939 million. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.014%, down -0.25%. With today being FOMC we don't try to map out levels or create bias. We'll sit on our hands until Powell speaks and try to ride the trend. I do think we have a decent shot at getting a retrace today. I'll see you all in the live trading room shortly.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Archives

November 2025

AuthorScott Stewart likes trading, motocross and spending time with his family.

|