|

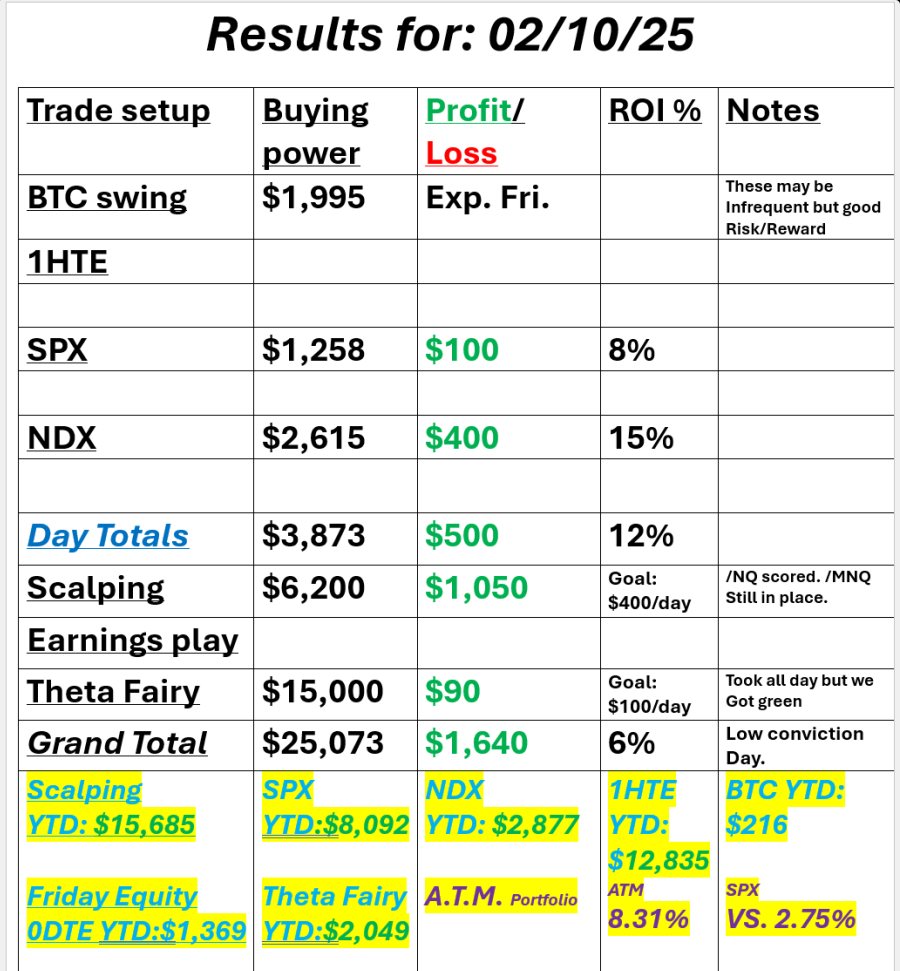

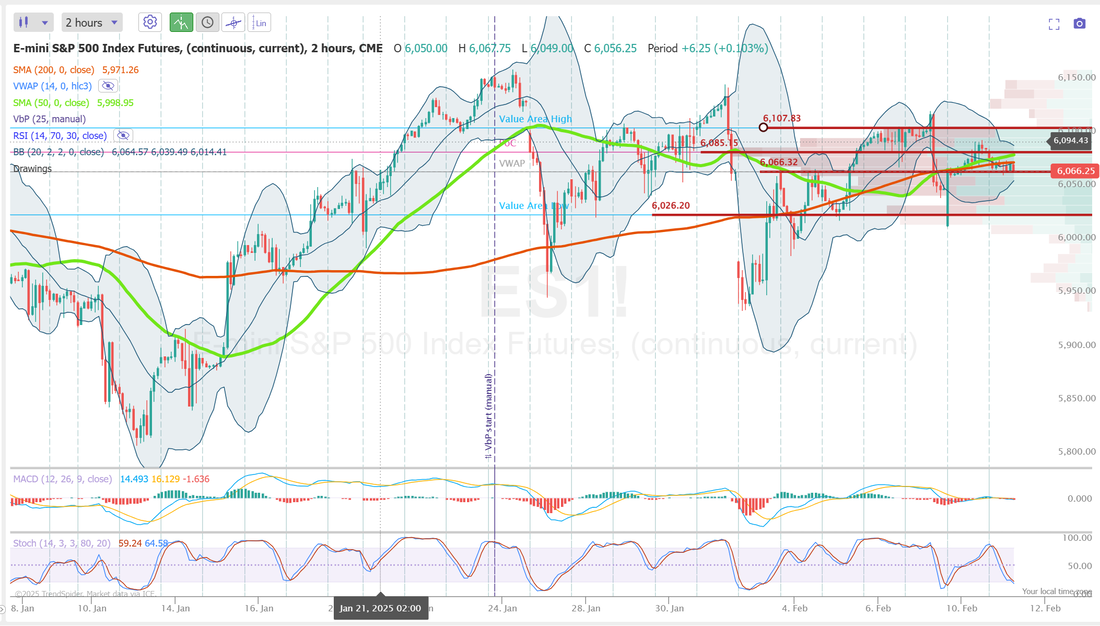

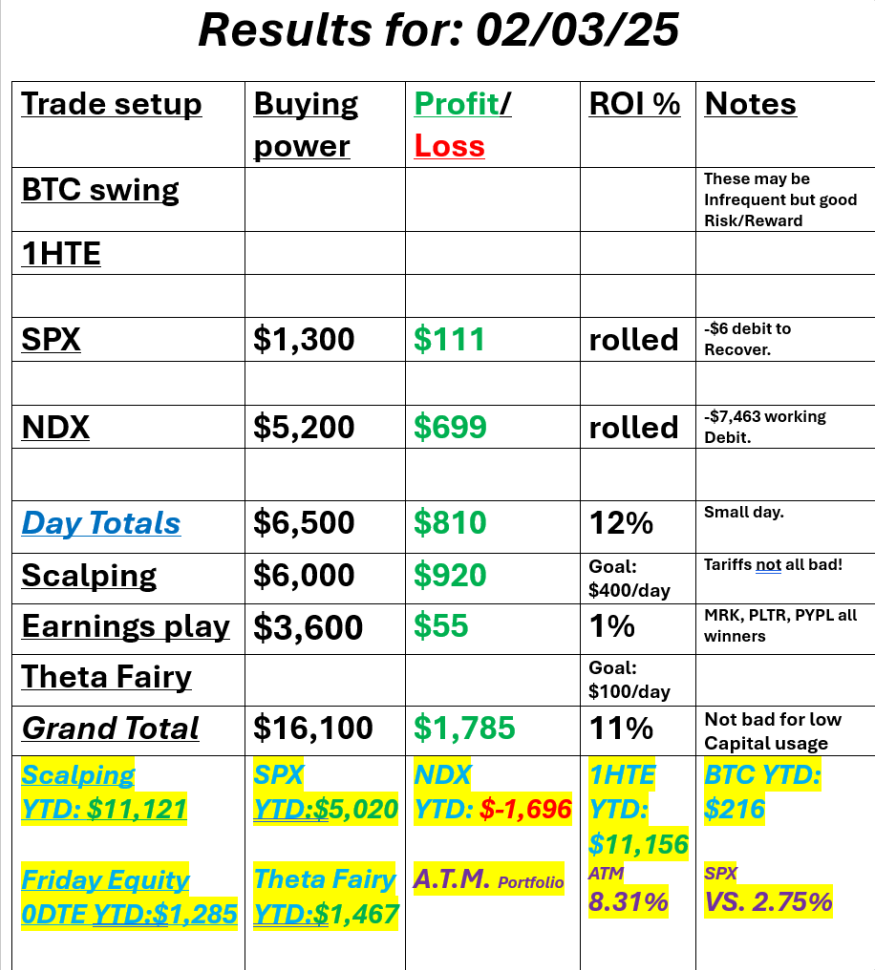

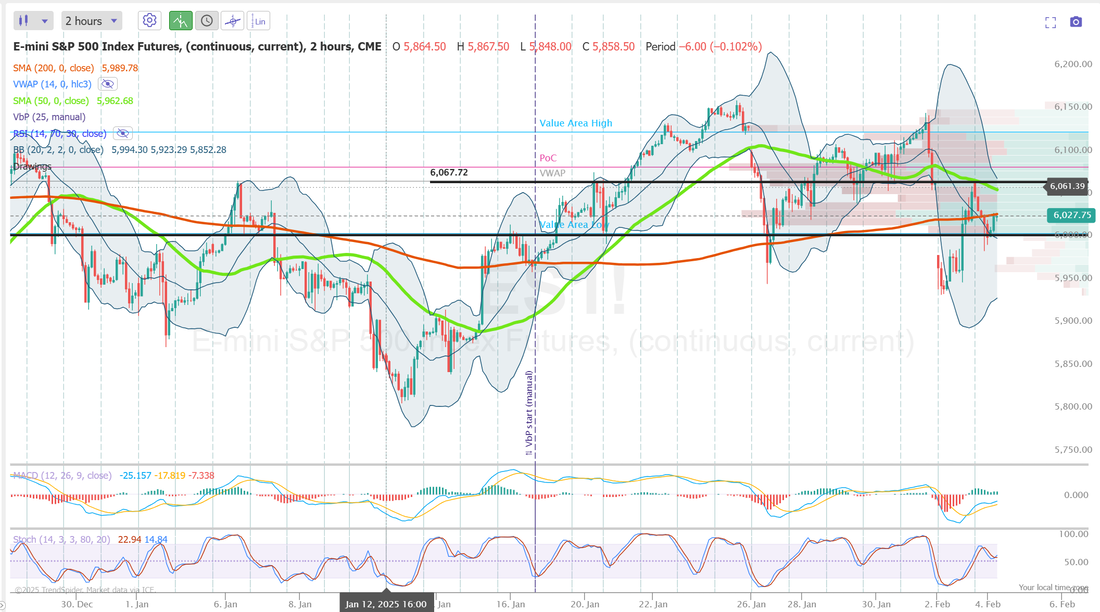

Welcome to CPI day! We've got PPI coming up tomorrow. Will these two days of data be enough to get us trending out of this chop zone? I'd love to see a down move to get some premium back in our trades. We had another solid day yesterday. Risk management was on point. It almost always costs us some potential when we are super risk focused. Pulling legs early or repositioning almost always costs money which comes out of the max potential profit but I made the statement Sunday night in our trading room that I wanted to pull $1,000 a day out of my account this week and still keep the value growing so we have no room for error and so far so good. Take a look at our results below. Also, our YTD numbers are looking pretty good.  I only update our ATM program once a month but that asset allocation model is up over 11% so far YTD. I continue to think we'll have a really good shot at a good result this year vs. the SP500, which I think is going to have some headwinds. March S&P 500 E-Mini futures (ESH25) are trending down -0.12% this morning as investors braced for the release of key U.S. inflation data while also awaiting further testimony from Federal Reserve Chair Jerome Powell. In yesterday’s trading session, Wall Street’s main stock indexes closed mixed. DuPont de Nemours (DD) climbed over +6% and was the top percentage gainer on the S&P 500 after the industrial materials maker reported better-than-expected Q4 results. Also, Coca-Cola (KO) advanced more than +4% and was the top percentage gainer on the Dow after the beverage maker posted upbeat Q4 results. In addition, Intel (INTC) rose over +6% after U.S. Vice President JD Vance said the Trump administration would ensure that advanced artificial intelligence chips are manufactured in the country. On the bearish side, Fidelity National Information Services (FIS) plunged more than -11% and was the top percentage loser on the S&P 500 after the payment technology company issued below-consensus Q1 guidance. Don't Miss: Own a piece of the world’s most iconic characters—invest now before this opportunity disappears! The Barchart Brief: Your FREE insider update on the biggest news stories and investing trends, delivered middayIn prepared remarks for a Senate hearing Tuesday, Fed Chair Jerome Powell reiterated that the central bank is not in a hurry to cut rates. “With our policy stance now significantly less restrictive than it had been and the economy remaining strong, we do not need to be in a hurry to adjust our policy stance,” he said. Also, Powell described the labor market as “not a source of significant inflationary pressures.” In addition, the Fed chief noted that speculating on tariff policy at this time would be unwise. “He’ll want to see the February jobs and inflation data, and align with other policymakers before saying much,” said David Russell at TradeStation. Cleveland Fed President Beth Hammack stated on Tuesday that keeping interest rates steady for “some time” is appropriate as policymakers wait for further progress on inflation and assess the economic impact of new government policies. Also, New York Fed President John Williams said that “the modestly restrictive stance of policy should support the return to 2% inflation while sustaining solid economic growth and labor market conditions,” but cautioned that policy-related uncertainty casts a shadow over the economic outlook. Meanwhile, U.S. rate futures have priced in a 95.5% probability of no rate change and a 4.5% chance of a 25 basis point rate cut at the March FOMC meeting. Today, all eyes are focused on the U.S. consumer inflation report, which is set to be released in a couple of hours. The report may indicate when U.S. interest rates are next likely to be cut, if at all. Economists, on average, forecast that the U.S. January CPI will come in at +0.3% m/m and +2.9% y/y, compared to the previous numbers of +0.4% m/m and +2.9% y/y. Also, the U.S. core CPI is expected to be +0.3% m/m and +3.1% y/y in January, compared to December’s figures of +0.2% m/m and +3.2% y/y. A survey conducted by 22V Research revealed that 41% of respondents anticipate a “risk-off” market reaction to the CPI report, 31% predict “risk-on,” and 28% expect it to be “mixed/negligible.” Investors will also focus on Fed Chair Jerome Powell’s semi-annual monetary policy testimony before the House Financial Services Committee, due later in the day. Atlanta Fed President Raphael Bostic and Fed Governor Christopher Waller are scheduled to speak today as well. On the earnings front, notable companies like Cisco (CSCO), AppLovin (APP), CVS Health Corp. (CVS), The Trade Desk (TTD), Robinhood Markets (HOOD), and Reddit (RDDT) are slated to release their quarterly results today. According to Bloomberg Intelligence, companies in the S&P 500 are expected to post an average +7.5% increase in quarterly earnings for Q4 compared to the previous year. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.549%, up +0.26%.  /ES, CRNX, DASH, LYFT, QTTB, SMCI, UPST, VALU, VRTX, CSCO, MGM, HOOD, RDDT, 0DTE's. With CPI today and PPI tomorrow I don't express a lean or bias and I don't look at levels until the day is a few hours in. These are days that the Algos will determine the moves and its important to be flexible. I'll see you all in the live trading room shortly. We'll be working our /ES trade quite a bit today. We've already got the anchor position in place.

0 Comments

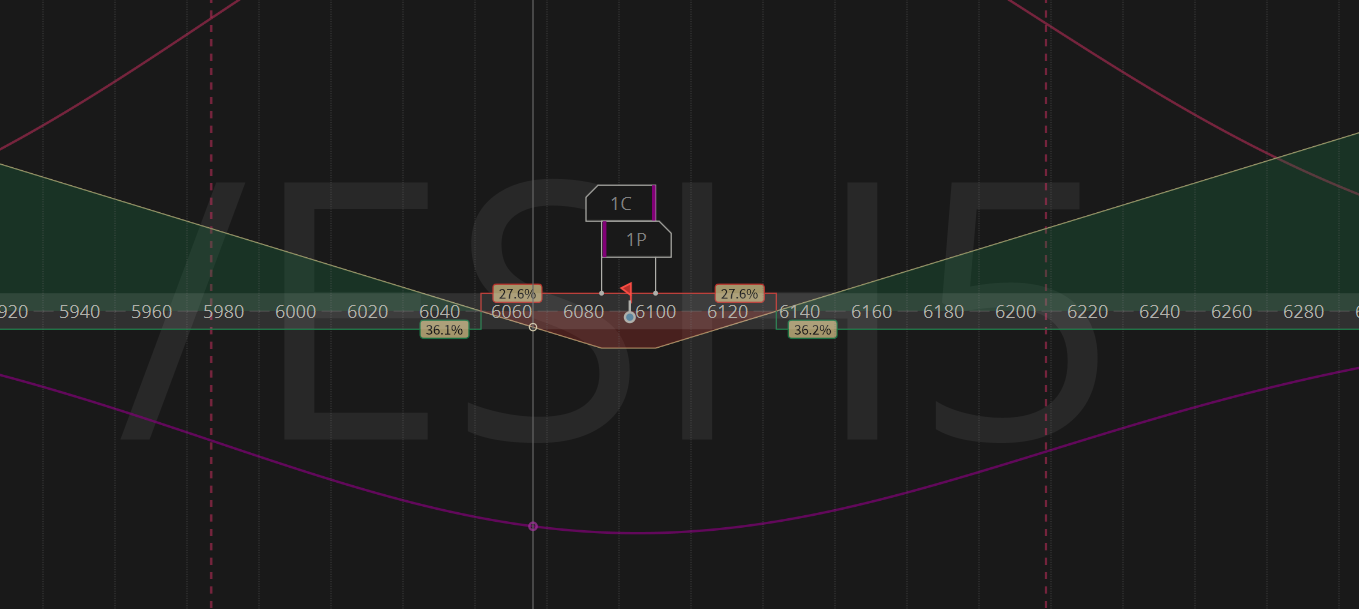

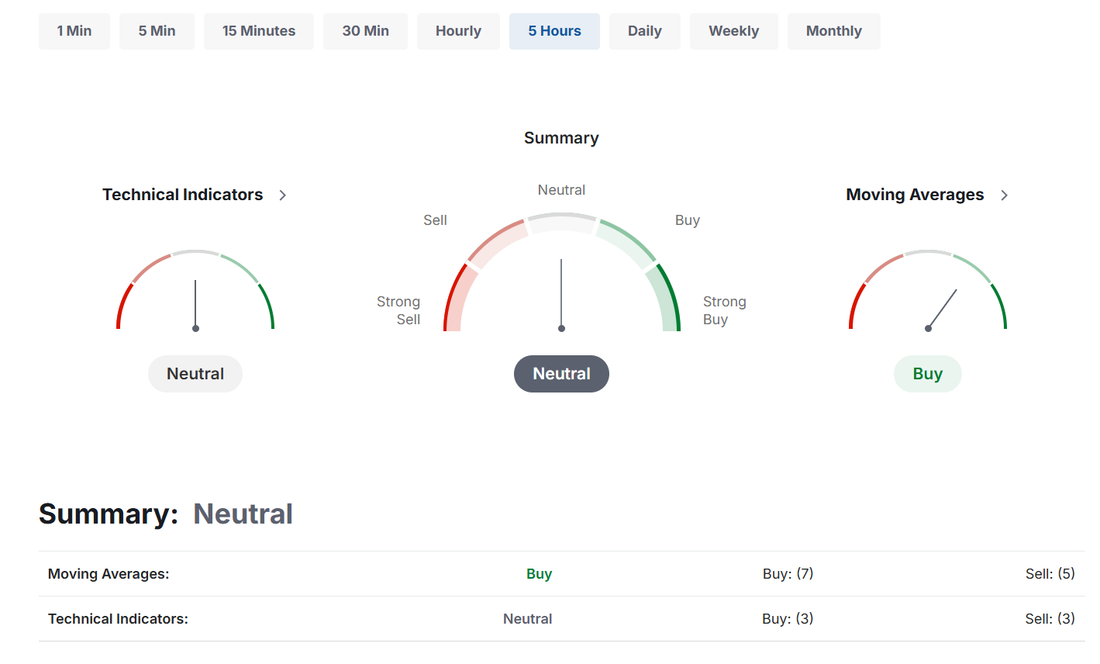

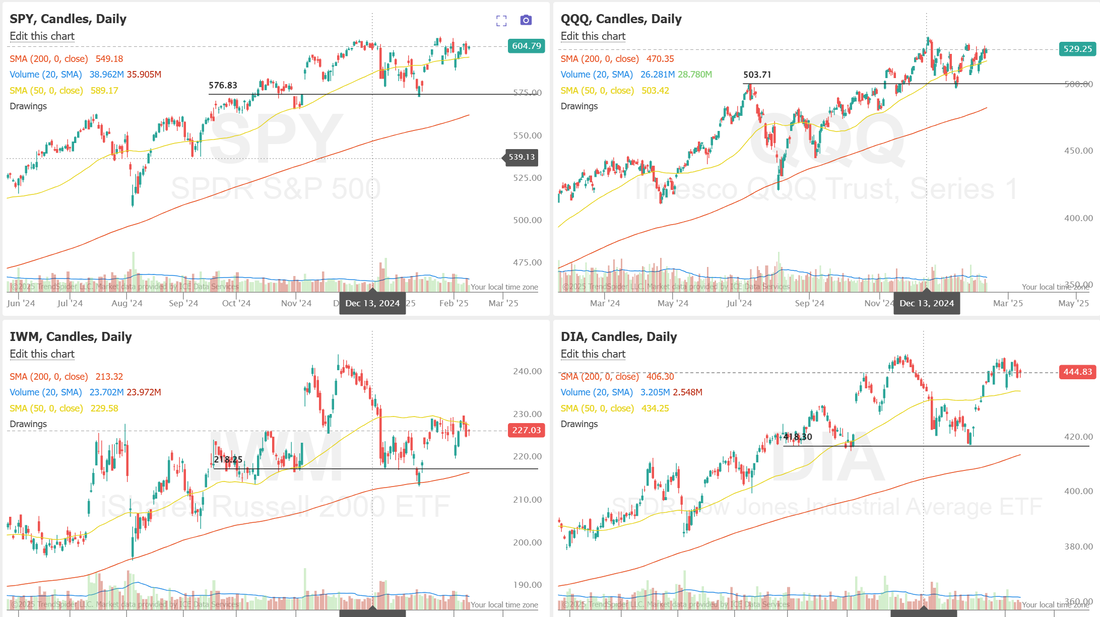

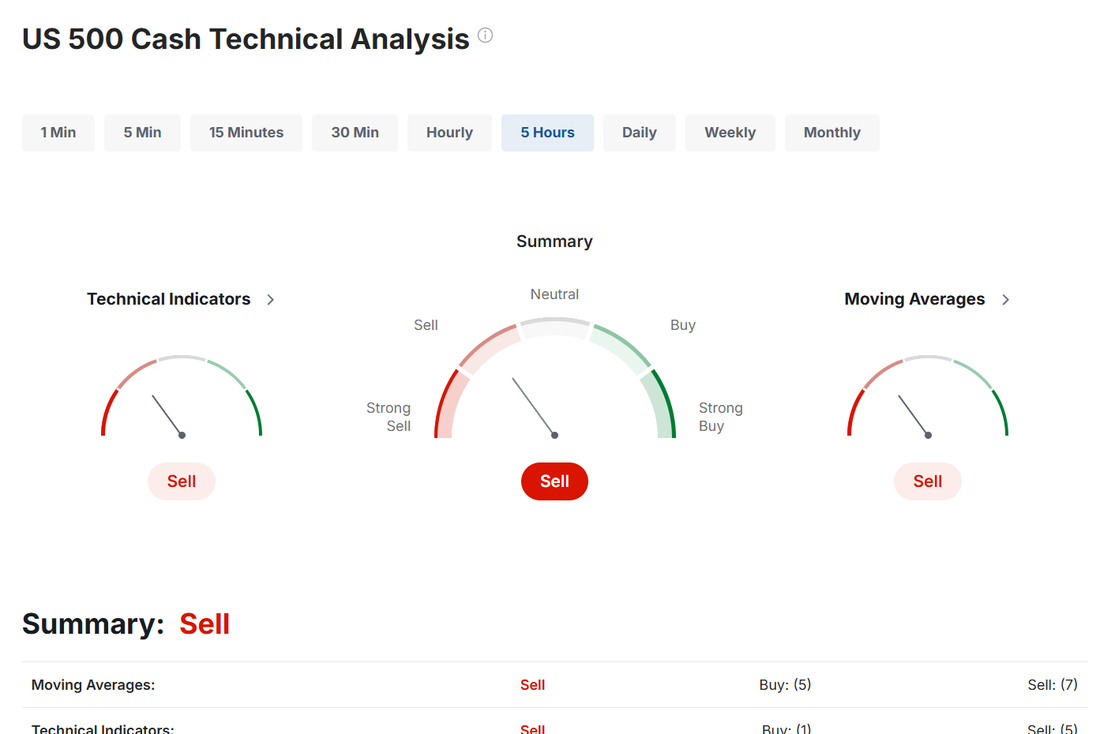

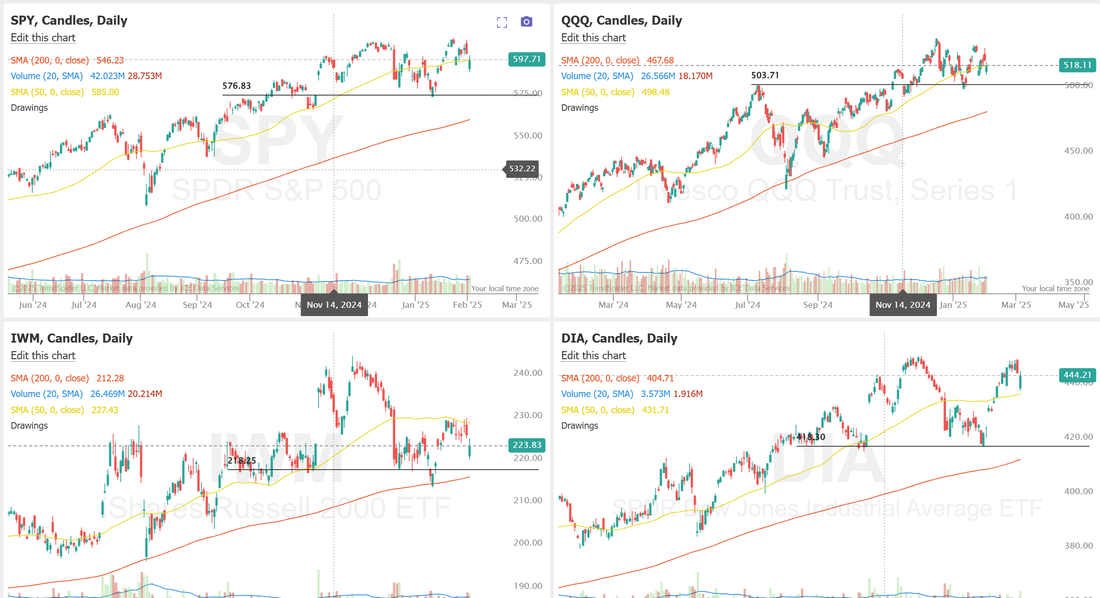

Yesterday day was a good day for us. It was a solid reminder that we don't always need to swing for the fences to have a $1,000+ profit day. I was trading with a bit of "tariff ptsd" yesterday. We've had three days where our trades looked amazing...until they didn't, as soon as tariff news dropped. I simply wasn't willing to trade the puts side yesterday and while that cost us some potential premium capture, I stand by it. It was the right thing to do from a risk management standpoint. It was also a great lesson in how important it is to have multiple, diversified strategies. We still had a solid day, even with the low capital outlay and conservative approach. See our results below.  Let's take a look at the market. We start today off with a neutral rating. That seems appropriate as we continue to churn in a tight chop zone.  One thing I feel pretty confident about predicting is that we won't stay stuck at this level forever. We have CPI and PPI coming up in the next couple of days. That may be enough to get us moving agian.  March S&P 500 E-Mini futures (ESH25) are down -0.33%, and March Nasdaq 100 E-Mini futures (NQH25) are down -0.44% this morning as investors digested another round of tariffs introduced by U.S. President Donald Trump and looked ahead to Federal Reserve Chair Jerome Powell’s congressional testimony as well as Wednesday’s release of a key U.S. inflation report. Late Monday, President Trump ordered a 25% tariff on steel and aluminum imports from all countries, including key suppliers Mexico and Canada, effective March 12th, but stated he would consider an exemption for Australia. Trump earlier said he would introduce reciprocal tariffs on countries that tax U.S. imports this week. In yesterday’s trading session, Wall Street’s three main equity benchmarks ended higher. Rockwell Automation (ROK) surged over +12% after the automation products maker reported better-than-expected FQ1 adjusted EPS. Also, aluminum and steel company stocks advanced after Trump announced plans to impose a 25% levy on all steel and aluminum imports into the U.S., with Cleveland-Cliffs (CLF) soaring more than +17% and Alcoa (AA) rising over +2%. In addition, McDonald’s (MCD) climbed more than +4% and was the top percentage gainer on the Dow after the burger chain posted an unexpected increase in Q4 comparable sales. On the bearish side, ON Semiconductor (ON) slumped over -8% and was the top percentage loser on the S&P 500 and Nasdaq 100 after the chipmaker posted downbeat Q4 results and issued below-consensus Q1 guidance. Today, market participants will closely monitor Fed Chair Jerome Powell’s semi-annual monetary policy testimony before the Senate Banking Committee for insights into the rate outlook. Powell will likely emphasize the resilient economy as a primary reason policymakers are not in a hurry to further reduce borrowing costs. Also, investors will likely focus on speeches from Cleveland Fed President Beth Hammack, Fed Governor Michelle Bowman, and New York Fed President John Williams, due later in the day. Aside from Powell’s testimony, the U.S. consumer inflation report for January, scheduled for release on Wednesday, will be a highlight, as it may indicate when U.S. interest rates are next likely to be cut, if at all. The CPI is expected to remain unchanged from December at +2.9% y/y, while the core CPI is projected to ease to +3.1% y/y from +3.2% y/y in December. “Inflation data, Powell’s congressional testimony, and tariffs are poised to drive the market story,” said Chris Larkin at E*Trade from Morgan Stanley. “If the S&P 500 is going to break out of its two-month consolidation, it may need a respite from the types of negative surprises - like DeepSeek, tariffs, and consumer sentiment - that have tripped it up over the past few weeks.” Meanwhile, U.S. rate futures have priced in a 93.5% probability of no rate change and a 6.5% chance of a 25 basis point rate cut at the next FOMC meeting in March. On the earnings front, notable companies like Coca-Cola (KO), Shopify (SHOP), Gilead (GILD), Marriott (MAR), and DoorDash (DASH) are set to report their quarterly figures today. According to Bloomberg Intelligence, companies in the S&P 500 are expected to post an average +7.5% increase in quarterly earnings for Q4 compared to the previous year. The U.S. economic data slate is largely empty on Tuesday. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.521%, up +0.58%. /HG, /MNQ,/NQ scalping, F, MRK, SHOP, TPB, TSLA, VRTX, DASH, SMCI, LYFT, UPST, 0DTE's. My bias or lean today is bearish, just like yesterday. Powell is speaking today but we don't really have any news catalysts today other than the tariff overhang. The market is focused on CPI, PPI coming up. We've carried over a bearish scalp from yesterday and will continue to work that today.  Let's take a look at our intra-day levels: /ES: There are some very critical levels today. 6084 is the first resistance with 6107 above that. 6066 is the absolute critical first support. We are sitting on that right now, as I type. If we can't hold that level we could see a move all the way down to 6024.  /NQ: 21,832 is resistance with 21,656 acting as support. If we lose that level we could see price action all the way down to 21,572.  BTC: Bitcoin continues to channel, making it hard to get a solid 1HTE working. They tend to be better risk/reward when we are trending vs. consolidating. The $100,000 level continues to be big resistance with $97,269 acting as near term support and $95,910 working as the next level down.  I look forward to seeing you all in the trading rooms today. We've got a good, bearish scalp on today that could yield us another solid profit day. Lots of earnings trades and of course, our 0DTE's.  Good morning traders! Welcome back to a new week. I hope everyone had a nice weekend. We spent some time with our neighbors watching the Superbowl. I'm not a stick and ball fan but it was nice to hang out with friends. We had an exceptional day Friday. It was a nice way to end the week. Take a look at our results below:  There's honestly not much to be unhappy about with our YTD performance. I've mentioned this before but Scalping cotinues to be a huge help for us as well as the 1HTE's. I'm also really happy with how many Theta fairies we've been able to get on. I'm entering today with a short /MNQ scalp and a Theta fairy that only has the call side working. I'm currently down on both of these but I think with regards to tariffs, "Fool me once, shame on you. Fool me four times? Come on!" I just think I'd rather be bearish here and need to roll up and out vs. bullish and need to roll out and down. Let's take a look at the technicals to start the week. Bullish bias and futures are up this morning but...I'm positioning for some bearish moves. CPI and PPI are out this week. "policy volatility" is coming into play and we'll take about systemic vs. unsystemic risk and how, regardless of technicals, I'd rather have some bearish exposure right now.  Overall, I don't seem much to be impressed about in this price action.  This week, the SPY closed marginally lower at $600.77 (-0.16%). After three weeks of tight price action paired with a squeeze, next week’s CPI and PPI data could be the catalyst for the next major move. This index will have to gain the top of the ascending triangle to push higher, while the rising trendline from the August 5th lows could act as a critical support level if sellers take control.  QQQ posted a modest gain this week, closing at $522.92 (+0.12%), as it continues to inch higher within a well-defined ascending triangle. Monday’s bounce off the lower trendline reaffirmed key support, keeping bullish momentum intact. Now in the third week of its squeeze, QQQ is nearing the triangle’s apex, potentially setting up for a decisive move on next week’s CPI announcement.  IWM lagged behind its index peers this week, closing lower at $226.00 (-0.21%) and testing the lower boundary of its ascending channel, a key level since October 2023. Now, in a prolonged squeeze that has turned negative for the first time since last summer, the stage is set for a decisive move. Will this extended squeeze lead to a breakdown, or will buyers dig in here at support?  Let's take a look at the expected moves for the week.. I.V. for the week isn't horrible and it's not amazing. We should be o.k. to get both debit and credit setups working this week.   The VIX1D at 16 is agian, middle of the road levels. Not great...not horrible.  My bias or lean is a little contrary today. We've got bullish technicals and bullish futures price action this morning We've also got the pinching wedge channels I detailed above which usually precede a big move. With "plicy volatility" in play, once again this week, I think I'd rather have some bearish positions on. I'm slightly bearish today. CSGS, /ZW, /HG, /ZN, TPB, HIMS, /es, /MCL, /MNQ scalping, CRNX, F, MRK, TSLA, VALU, VRTX, KO, SHOP, BITO Let's take a look at our intra-day levels for 0DTE setups. /ES: There are a couple interesting levels. 6116 is resistance with a close 6079 acting as support. This is a key support. It's close and it also aligns with the 50/200 period M.A. on the 2hr. chart. 6010 is also on my radar. This is the dip that futures opened up at Sunday night and bounced hard.  /NQ: 21,828 is resistance with 21,829 being the next interesting level higher up. 21,528 is support with 21,445 just down below that.  BTC: $160,100 is resistance with a key area of interest being $98,377. This is a big demarcation point. Above would be bullish and below would be bearish. $95,977 seems to be a solid support level.  I look forward to seeing you all in the live trading room shortly!  Welcome to Friday. The gateway to the weekend! We had an absolutely perfect day yesterday. Check it out below.  Busy day. We double dipped on the Theta fiary. /ES, /MCL, /NG (LRN), /SI, AFRM, AMZN, F, GE, MRK, MSTR (0DTE), NVDA (0DTE), PINS, QQQ/SPY, TSLA, VALU, 1HTE and 0DTE's. See you all in the live trading room shortly. Let's see if we can put another $1,000+ dollars in our pockets today to end an awesome week on the right foot.  Welcome back traders! We are finally to expiration day of our 15DTE "mistake" NDX trade. For a quick recap, I errantly placed a 0DTE as a 15DTE (I have a habit of doing that!) We've traded around it for the last two weeks and the mistake actually looks pretty profitable. Building more of these (on purpose) may not be a bad way to go in this current enviroment. Here's my results from yesterday. I took a flyer right before the close on NDX that lost but most of our traders skipped it. Otherwise is was a solid day. I'm loving our setups in scalping. I'm really interested to see how we finish out this year with scalping and our ATM program. I think both of these hold a lot of promise.  March S&P 500 E-Mini futures (ESH25) are up +0.05%, and March Nasdaq 100 E-Mini futures (NQH25) are down -0.08% this morning as investors awaited a new round of U.S. economic data, remarks from Federal Reserve officials, and an earnings report from “Magnificent Seven” member Amazon. In yesterday’s trading session, Wall Street’s main stock indexes ended in the green. Johnson Controls (JCI) surged over +11% and was the top percentage gainer on the S&P 500 after the company posted upbeat FQ1 results and raised its FY25 adjusted EPS guidance. Also, chip stocks gained ground after the benchmark 10-year Treasury yield fell to a 7-week low, with Marvell Technology (MRVL) climbing more than +6% and Nvidia (NVDA) rising over +5%. In addition, Amgen (AMGN) advanced more than +6% and was the top percentage gainer on the Dow after reporting better-than-expected Q4 results. On the bearish side, Alphabet (GOOGL) slumped over -7% and was the top percentage loser on the Nasdaq 100 after the Google parent reported weaker-than-expected Q4 revenue as growth in its cloud business slowed. Also, Advanced Micro Devices (AMD) fell more than -6% after the chipmaker posted weaker-than-expected Q4 data center revenue, and its full-year forecast for the data center business failed to impress investors. The ADP National Employment report released on Wednesday showed that U.S. private nonfarm payrolls rose by 183K in January, up from 176K in December (revised from 122K) and beating the consensus estimate of 148K. Also, the final estimate of the U.S. January S&P Global services PMI was revised higher to 52.9 from the 52.8 preliminary reading. At the same time, the U.S. ISM services index fell to 52.8 in January, weaker than expectations of 54.2. In addition, the U.S. December trade deficit was -$98.40B, wider than expectations of -$96.50B and the largest deficit in nearly three years. Richmond Fed President Thomas Barkin stated on Wednesday that policymakers require more time to assess the trajectory of the U.S. economy and inflation amid heightened uncertainty over President Donald Trump’s policies, reinforcing expectations for rates to remain unchanged. Also, Fed Vice Chair Philip Jefferson said he is comfortable keeping interest rates on hold until policymakers gain a clearer understanding of the overall impact of the Trump administration’s policies on tariffs, immigration, deregulation, and taxes. U.S. rate futures have priced in an 85.5% chance of no rate change and a 14.5% chance of a 25 basis point rate cut at the next central bank meeting in March. Meanwhile, U.S. Treasury Secretary Scott Bessent said on Wednesday that the Trump administration’s primary focus in lowering borrowing costs is on 10-year Treasury yields rather than the Fed’s benchmark short-term interest rate. He stated in an interview with Fox Business that regarding the Fed, “I will only talk about what they’ve done, not what I think they should do from now on.” Bessent reiterated his belief that increasing energy supply would aid in reducing inflation. Fourth-quarter corporate earnings season continues, with investors looking forward to fresh reports from notable companies today, including Amazon.com (AMZN), Eli Lilly (LLY), Philip Morris (PM), Honeywell (HON), Bristol-Myers Squibb (BMY), Fortinet (FTNT), and Take-Two Interactive (TTWO). According to Bloomberg Intelligence, companies in the S&P 500 are expected to post an average +7.5% increase in quarterly earnings for Q4 compared to the previous year. On the economic data front, investors will focus on U.S. Initial Jobless Claims data, which is set to be released in a couple of hours. Economists expect this figure to be 214K, compared to last week’s number of 207K. U.S. Unit Labor Costs and Nonfarm Productivity preliminary data will also be closely watched today. Economists forecast Q4 Unit Labor Costs to be +3.4% q/q and Nonfarm Productivity to be +1.5% q/q, compared to the third-quarter numbers of +0.8% q/q and +2.2% q/q, respectively. In addition, market participants will be anticipating speeches from Fed Governor Christopher Waller, San Francisco Fed President Mary Daly, and Dallas Fed President Lorie Logan. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.435%, up +0.34%. Yesterdays price action was what I had predicted and it was enough to get us a slightly bullish outlook going into todays session.  I'm not going into this session with any real lean or bias. I'll note the demarcation points below for a bullish or bearish trigger. Things for the most part look bullish. It's only the IWM that still can't get back up above it's 50DMA.  We had a busy docket yesterday and that should continue today. NVDA and MSTR as 1DTE's to work as 0DTE's tomorrow. AFRM, AMZN, AMAT, PINS, ARM, BMY, F, GOOG, MRK?, QCOM, RBLX earnings trades. Possible TSLA, VIX, 1HTE, 0DTE's and /ZN. Let's take a look at our intra-day levels. /ES: There are three levels I'm watching today. 6126 is resistance with 6069 acting as support but I'm most interested in 6085. It's PoC on the 2hr. chart and may offer a nice entry level for a butterfly.  /NQ: Resistance is close at 21,832 but if was firmly rejected yesterday. If we can break above and hold today that would be very bullish. 21,591 is support and also key. It's a convergence of both the 200 and 50 period moving averages. A break below this would be very bearish. We've been channeling for a while now. A big move could be incoming.  BTC: We had a nice clean, "one and done" 1HTE yesterday for a $499 profit but I'm less optimistic about todays potential. Resistance stays right at $100,756 with support at $98,491. I'd look to start a new long swing trade around the $96,997 level.  I'll see you all in the trading room shortly!  Welcome back traders! We had a great day yesterday. Not a perfect day. Our SPX debit didn't hit but our NDX did. I want to do a training review today on the nine main orderflow indicators we use and what is showing on our live scalping zoom feed. See below:  Supertrend, Parabolic SAR, Pivot point, Squeeze indicator, Audible order flow with Tickstrike, $TICK, $ADSPD, $VOLSPD are the ones we'll focus on today. As I mentioned, our results were solid.  I want to stress, once again, how important it is to have diversified strategies working each day. I can't remember the last time we've had a day where something wasn't losing money and yet, you'll see our YTD results are impressive. You never know what's going to work. Scalping is one example. We did scalp yesterday but no results were posted because the cover is set to expire this Friday but there's $2,500 potential profit sitting there. Our Theta fairys are another example. We hit a $170 profit last night in a couple hours.  Sometimes the cash is pouring in on scalping and Theta fairys and sometimes we go a whole week without a single entry. You just never know what opportunities the market will offer up each day. Let's look at the markets: Poor earnings results from GOOG and AMD as well as China issues with AAPL are dragging the futures down this morning. It's put us back to a neutral rating to start the day which means it will just be a crap shoot about direction (IMHO).  Heaven knows we've had plenty of volatility and movement this past week but in terms of actual ranges or directional bias there's absolutely nothing happening! At some point we will move from consolidation to trending. Neutral days can be the trigger days for that to happen. I don't see that taking place today but you never know.  March Nasdaq 100 E-Mini futures (NQH25) are trending down -0.91% this morning as disappointing results from Alphabet and Advanced Micro Devices weighed on sentiment. Alphabet (GOOGL) slid over -7% in pre-market trading after the Google parent reported weaker-than-expected Q4 revenue as growth in its cloud business slowed. Also, Advanced Micro Devices (AMD) slumped more than -8% in pre-market trading after the chipmaker posted weaker-than-expected Q4 data center revenue, and its full-year forecast for the data center business failed to impress investors. Market participants now look ahead to a fresh batch of U.S. economic data, comments from Federal Reserve officials, and corporate earnings reports, with a particular focus on results from entertainment giant Disney. In yesterday’s trading session, Wall Street’s three main equity benchmarks closed higher. Palantir Technologies (PLTR) jumped about +24% and was the top percentage gainer on the S&P 500 and Nasdaq 100 after the data analytics company posted upbeat Q4 results and issued above-consensus Q1 and FY25 revenue guidance. Also, megacap technology stocks advanced, with Apple (AAPL) and Tesla (TSLA) rising more than +2%. In addition, Super Micro Computer (SMCI) climbed over +8% after the artificial intelligence server maker announced that it would provide an FQ2 business update on February 11th. On the bearish side, Estee Lauder (EL) plunged more than -16% and was the top percentage loser on the S&P 500 after the cosmetics and skin care company provided a downbeat FQ3 outlook and announced job cuts. Also, Merck & Co. (MRK) slumped over -9% and was the top percentage loser on the Dow after halting shipments to China of its Gardasil vaccine and offering a weak FY25 forecast. A Labor Department report released on Tuesday showed that the U.S. JOLTs job openings fell to 7.600M in December, weaker than expectations of 8.010M. Also, U.S. December factory orders fell -0.9% m/m, weaker than expectations of -0.7% m/m and marking the largest decline in 6 months. “[The latest reading on U.S. job openings] eases upside risks into Friday’s employment report in a way that is helpful for the Federal Reserve and markets,” said Krishna Guha at Evercore. Fed Vice Chair Philip Jefferson said on Tuesday, “As long as the economy and the labor market remain strong, I see it as appropriate for the Committee to be cautious in making further adjustments... I do not think we need to be in a hurry to change our stance.” Meanwhile, U.S. rate futures have priced in an 83.5% chance of no rate change and a 16.5% chance of a 25 basis point rate cut at the conclusion of the Fed’s March meeting. Fourth-quarter corporate earnings season rolls on, and investors await new reports from notable companies today, including The Walt Disney Company (DIS), Qualcomm (QCOM), Arm Holdings (ARM), Uber Technologies (UBER), and Ford Motor (F). According to Bloomberg Intelligence, companies in the S&P 500 are expected to post an average +7.5% increase in quarterly earnings for Q4 compared to the previous year. On the economic data front, all eyes are focused on the U.S. ADP Nonfarm Employment Change data, which is set to be released in a couple of hours. Economists, on average, forecast that the January ADP Nonfarm Employment Change will stand at 148K, compared to the December figure of 122K. Investors will also focus on the U.S. ISM Non-Manufacturing PMI and the S&P Global Services PMI. Economists expect the January ISM Non-Manufacturing PMI to arrive at 54.2 and the S&P Global Services PMI to be 52.9, compared to the previous values of 54.1 and 56.8, respectively. U.S. Trade Balance data will come in today. Economists foresee this figure standing at -$96.50B in December, compared to -$78.20B in November. U.S. Crude Oil Inventories data will be released today as well. Economists estimate this figure to be 2.400M, compared to last week’s value of 3.463M. In addition, market participants will be looking toward speeches from Fed officials Barkin, Goolsbee, Bowman, and Jefferson. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.471%, down -0.93%. My lean or bias for today: We nailed our bullish call yesterday. The day played out exactly as I laid out in our pre-market plannning. With credit trades your directional bias doesn't neccessarily need to be right to make money but it certainly helps and makes the day easier. I'm looking for another slightly bullish today. We may not finish in the green but with /ES down -30 points as I type I think we come up from here.  Trade docket for today: ARM, QCOM, F?, UBER?, BMY, RBLX, AMD, AMGN, GOOG, MRK?, SPY/QQQ, /MCL, 1HTE, 0DTE's. Let's take a look at our intra-day levels: /ES: Levels for today are the same as yesterday. 6067 is resistance with 6005 support. 6042 is key! This is the convergence zone for both the 50 and 200DMA's on the 2hr. chart. If you are good at chart reading you could look at this pinch point and guess we are starting off the day with a neutral technical reading. This will not last. We'll move off of this level (maybe forcefully) soon.  /NQ: Nasdaq levels have moved up from yesterday. 21,625 is resistancewith 21,350 working as new support.  BTC: Bitcoin has been a bit tough to trade our 1HTE's lately. We were able to catch a partial profit yesterday. There are three levels I'm watching today. $100,801 is resistance with $97,006 acting as support. $98,130 seems to be the demarcation point. Above I'd look for bullish action. Below, bearish. If we dip to that $97,000 range I'll look to start a new swing trade.  We've got a lot of training and other items to talk about today is zoom. I look forward to seeing you all shortly.  Welcome to Tues. traders! Are we getting a little stability, post tariffs? I'm looking for a bullish day today. More on that in a minute. We had a good day yesterday considering we had no idea (no one did, no matter what they said) about the tariffs. Would they or wouldn't they be implemented. How would the market be effected? Yesterday was going to be a big unknown so we traded really small (in comparision to a normal day) and waited most of the day before entering our trades. We still netted an 11% gain on the day. It brings up the ever present question...what's more important, transparency or premium? You'll usually get the best premium on your credit trades if you establish them right at the open but you lack transparency and a lot can happen those next 6.5 hrs. before the market closes. If you wait, like we did yesterday where we only had 1-2 hours left in the day, you get much better transparency but much less premium. I think it tough to apply a universal rule that one is always better than the other. There was enough volatility yesterday that we picked transparency over premium. Every day this is one of our main questions we ask ourselves. Here's our results from yesterday. One last comment...on days that are "scary" or uncertain or volatile, scalping can yield great risk/reward setups. I'm a firm believer that you need as many tools as possible.  Let's take a look at the markets Technicals are still bearish after the weak last couple of days but I'm looking for that to change today.  Yesterday was incredibly bullish. Yes I know technicals are bearish. Yes I know we finished down on the day but...we spent most of the day climbing out of the hole that futures dug. Note the green candles.  March S&P 500 E-Mini futures (ESH25) are down -0.01%, and March Nasdaq 100 E-Mini futures (NQH25) are up +0.08% this morning as investors awaited the latest reading on U.S. job openings, comments from Federal Reserve officials, and corporate earnings reports from heavyweight names. Stock futures initially moved lower after China retaliated to new U.S. tariffs. China’s Customs Tariff Commission of the State Council announced on Tuesday that it will impose a 15% tariff on U.S. coal and liquefied natural gas, and 10% tariffs on crude oil, agricultural machinery, large-displacement vehicles, and pickup trucks. The measures are set to take effect on February 10th. China’s commerce ministry also announced that starting Tuesday, the country will implement export controls on tungsten, tellurium, bismuth, molybdenum, and indium products. In addition, China said it would launch an antitrust probe into Google. This marked the resumption of a trade war between the world’s two largest economies, though China’s response was seen as restrained. In yesterday’s trading session, Wall Street’s major indexes ended in the red. Moderna (MRNA) sank over -7% and was the top percentage loser on the S&P 500 as vaccine makers retreated amid expectations that vaccine skeptic Robert Kennedy Jr. would be appointed to lead the U.S. Department of Health and Human Services. Also, automobile stocks dropped after President Trump announced tariffs on U.S. imports from Canada, Mexico, and China, with Tesla (TSLA) sliding more than -5% and General Motors (GM) falling over -3%. In addition, FedEx (FDX) slumped more than -6% after Loop Capital downgraded the stock to Hold from Buy. On the bullish side, IDEXX Laboratories (IDXX) surged over +11% and was the top percentage gainer on the S&P 500 and Nasdaq 100 after the pet healthcare company posted upbeat Q4 results and issued solid 2025 EPS guidance. Economic data released on Monday showed that the U.S. ISM manufacturing PMI rose to 50.9 in January, stronger than expectations of 49.3 and marking the highest level in 2-1/3 years. Also, the U.S. January S&P Global manufacturing PMI was revised upward to 51.2, beating the consensus of 50.1. In addition, U.S. construction spending rose +0.5% m/m in December, stronger than expectations of +0.3% m/m. Chicago Fed President Austan Goolsbee stated on Monday that the central bank should be more cautious in reducing borrowing costs due to increasing uncertainty stemming from the Trump administration. “Now we’ve got to be a little more careful and more prudent of how fast rates can come down because there are risks that inflation is about to start kicking back up again,” Goolsbee said. Also, Atlanta Fed President Raphael Bostic stated that he wants to wait “a while” before lowering interest rates again following last year’s cuts, given the uncertainty surrounding the direction of the U.S. economy in 2025. In addition, Boston Fed President Susan Collins said, “There’s no urgency for making additional adjustments.” Meanwhile, U.S. rate futures have priced in an 86.5% probability of no rate change and a 13.5% chance of a 25 basis point rate cut at the next FOMC meeting in March. Fourth-quarter corporate earnings season continues in full flow, with investors anticipating fresh reports from major companies today, including Alphabet (GOOGL), Advanced Micro Devices (AMD), PepsiCo (PEP), Merck (MRK), Amgen (AMGN), Pfizer (PFE), and PayPal (PYPL). According to Bloomberg Intelligence, companies in the S&P 500 are expected to post an average +7.5% increase in quarterly earnings for Q4 compared to the previous year. On the economic data front, all eyes are focused on the U.S. JOLTs Job Openings figures, set to be released in a couple of hours. Economists, on average, forecast that the December JOLTs Job Openings will arrive at 8.010M, compared to the November figure of 8.098M. Investors will also focus on U.S. Factory Orders data. Economists expect this figure to be -0.7% m/m in December, compared to the previous number of -0.4% m/m. In addition, market participants will be anticipating speeches from Atlanta Fed President Raphael Bostic, San Francisco Fed President Mary Daly, and Fed Vice Chair Philip Jefferson. In the bond market, the yield on the benchmark 10-year U.S. Treasury note is at 4.579%, up +0.79%. My lean or bias today is firmly bullish. Yeah, China retaliated with their own tariffs. That knocked the futures a bit but I think the market fundamentals were clearly bullish before Friday's tariff news and I think the smoke is clearing today and we'll return to that same bullish bias. Trade docket for today: MRK, PLTR, PYPL, GOOG, AMGN, AMD, /ZN, 0DTE's Let's take a looks at our key levels for todays 0DTE's. One reason for my bullish bias today is the fact that we bumped up along our resistance level all day long yesterday and overnight we've now broke above it. Resistance is now 6058 with support at 6005.  /NQ: The Nasdaq came back as well but wasn't as strong. It's running into it's 200 period M.A. on the 2hr. chart right now. That may be a tough nut to crack. Resistance is at 21,587 with support at 21,280 but that key 21,483 200 period M.A. on the 2hr. chart is my main focus for today. Above could be bullish. Below is bearish. It's a key demarcation level.  BTC: I certainly missed the opportunity yesterday to catch the falling knife and initiate one of our Bitcoin swing trades. We could have picked it up $7,000 dollars lower than current levels but that's how hindsight works. New levels seem to be $102,658 resistance with $98,408 support. I look forward to our live zoom session today. See you all soon! Welcome to a new month of trading and a new set of market catalysts called "tariffs". The market got thrown into turmoil late Friday as the treat of tariffs turned into more of a reality. I say more of a reality vs. an actual reality because there is still a chance (slim?) that this goes away. The tariffs were implemented last Saturday but they are really "implemented" until tomorrow, Tuesday. The EU tariff threat seems like it will be worked out before implementation and Trump has mentioned he will be talking to Canada and Mexico today, one day before D-day. It's a massive game of chicken with huge potential for market swings. Futures certainly look ugly this morning but if PLTR reports the blow out numbers expected today and a resolution is found (possibly after the market closes) Tomorrow could be a big up day...could be. It's a big guessing game right now. Here's our results from Friday.  Let's take a look at the markets. Probably not a surprise that the technicals are bearish to start the day.  The SPY ETF closed the week in negative territory at $601.82 (-1.00%). Buyers stepped in early Monday morning, absorbing the DeepSeek dip and driving prices higher in a steady grind with Momentum holding a higher low. By Friday, the gap was finally filled—but just as SPY approached new all-time highs, the tariff news hit, triggering a sharp reversal into the weekend.  The QQQ ETF closed the week at $522.29 (-1.39%), maintaining a higher low on the daily despite early-week pressure on tech stocks. Notably, the Momentum indicator has regained positive territory after briefly dipping earlier in the week. With major earnings reports from GOOG and AMZN on the horizon, bulls will be watching closely to see if Monday’s low holds.  The IWM outperformed its peers this week but closed in the red at $226.48 (-0.96%). The momentum indicator is showing a hidden bullish divergence on the daily, with momentum making a higher high while price did not. This could signal that small caps are primed to take the lead, after proving to be the most resilient of the major indexes this week.  My lean or bias today is neutral. Futures are down 100 points on /ES. Depending on the outcome of the negotiations that are planned with Canada and Mexico we could get a big swing one way or the other. To guess right now would be just that, a guess.  Trade docket for today will be lighter than a usual Monday. QQQ scalps could provide good opportunities. VIX trade again. ALTR?, ASUR?, TSLA, VALU, /SI, /MCL, PLTR, MRK and PYPL earnings. Possibly some small 1HTE and 0DTE's today. Let's see if we can find some intra-day levels that we like for some small 0DTE's today. /ES: 6024 is resistance this morning with 5935 acting as support. The challenge with all the indices today is, we know there is the catalyst of pending negotiations on tariffs but no idea when today or what the result will be. Levels may not be helpful today.  /NQ: Same principal here. Wide range and hard to put much stock in it yet. 21,580 resistance with 20,890 support.  BTC: Bitcoin had over a $10,000 drop from Friday! Big move. It appears to have stabilized now with 98,537 working as resistance now and 93,193 acting as support.  I look forward to seeing you all in the trading room today. Today should be a light (hopefully easy) day for us as we sit back a bit and let the tariff situation play out. |

Archives

August 2025

AuthorScott Stewart likes trading, motocross and spending time with his family.

|